A weak client communication strategy leads to low customer awareness of the offerings of rural CICO agents. As a result, the product uptake at these agent points remains low and hurts their incomes. MSC developed a client communication message focused on behavioral communication around small savings. We piloted the message in a rural area where APB had planned to expand its operations. The pilot results show that women who heard the audio clip saved 54 times more than women from similar geographies whom the message did not reach. This deck charts the journey of this pilot.

A toolbox for business correspondent agents for better customer engagement

MSC and FIA Global developed and tested a toolbox of behavioral change communication tools with select business correspondent agents in India. The objective was to help agents build awareness and enhance uptake of select government-backed insurance products by low-and moderate-income (LMI) people in India. Our report charts how we could help agents bridge these barriers around said products and enhance customer engagement. Read the report here to learn more about the intervention and the results.

From a digital lender to a microfinance bank—what does this mean for MFIs in Africa?

The many aspects of Financial Inclusion

MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

From a digital lender to a microfinance bank—what does this mean for MFIs in Africa?

Our podcast featured DFS Consultant Wesley Otoso and DFS Specialist Edward Obiko of MSC. They discussed the landmark transition where Kenya’s first digital lender Branch International acquired Century Microfinance Bank in its latest expansion drive. Wesley and Edward delve deeper to unpack the motivation behind this acquisition and what it now means to traditional financial service providers and FinTechs.

Testing a behavioral design approach to deliver product information at agent outlets

“I believe the most important thing in my business is to provide good service to customers and build their trust in financial products and services. Customers are not aware of various financial products, so I try to inform them about new products when they come to withdraw government benefits in their accounts—mostly in the first week of the month. Yet they do not enroll in them at my outlet, even after knowing about the product.” —A business correspondent (BC) agent from Damoh district, Madhya Pradesh (M.P.).

Almost 1 billion Indians lack life insurance coverage – a vast proportion of the population remains untapped. The Government of India launched a slew of flagship life and accident microinsurance products in 2015, such as Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY), and Pradhan Mantri Suraksha Bima Yojana (PMSBY). The government’s initiative made these products accessible and affordable, yet their uptake remains low. The report on Financial Literacy and Inclusion in India by the National Centre for Financial Education in 2019, noted that awareness and holding of PMSBY policies in rural areas is 28% and 6%, respectively. A similar percentage holds for PMJJBY. The report mentions that the most important reasons for not opting for insurance include the lack of felt need and lack of knowledge. Moreover, customers have low awareness of BC agent services (46%) and a low proportion of people use BC outlets (28%). In fact, the use of BC agent outlets for DBT is much lower. Our study to understand the Effectiveness of India’s DBT system during COVID-19 indicates that between April to May, 2020, among the 67% of respondent households that visited a cash-out point during the lockdown, only 13% visited a BC agent or CSC point.

Customers have limited trust in agents – particularly with products that will only yield a return in the future such as insurance products. This low trust is amplified by limited awareness of the products and their features, nature of benefits, the perception that the products are expensive, and negative word-of-mouth about the products from those who have tried them, which further restricts uptake. Concerted efforts are needed to market long-term products, such as insurance products, to build awareness and understanding of their benefits among low- and moderate-income (LMI) people.

MSC and FIA Global[1] conducted an experiment to improve the awareness of the LMI segment around government-backed insurance products (PMJJBY, PMSBY) and enhance their uptake through agent outlets. We designed and tested a toolbox that included a set of behavioral change communication tools incorporating human-centered design principles[2] to help agents build awareness and sell PMJJBY and PMSBY to LMI people.

The communication toolbox supports product information delivery to overcome behavioral biases that limit customer interest in the product and thus product uptake. The tools support agents to nudge existing and potential customers to move to desired behavior. The toolbox equips agents with tools to interact with customers, influence behavior, engage more customers, and build a positive customer experience.

The toolbox was rolled out in June 2021. It enhanced the customer-agent engagement and increased enrolment of insurance products that were relatively difficult to sell. This helped diversify the products sold by agents and increased their revenue streams. In the assessment period of June- November, the total enrolment in PMJJBY (by both women and men) grew by 36% in 2021 compared to 2020. PMJJBY sales also increased in comparison to PMSBY, which is comparatively easier to sell as compared to PMJJBY. This could be because PMSBY costs INR 12 (USD 0.16) per annum and PMJJBY INR 330 (USD 4.44) per annum. The ratio of PMJJBY/PMSBY insurance enrolled increased by 38% from 2019 to 2020. This ratio almost doubled from 2020 to 2021.

The BC agents used a combination of physical and digital elements in the toolbox creatively to engage potential customers. BC agents found the audio and video links (1, 2, 3) beneficial and used them creatively on social media. They used them as their WhatsApp status, forwarded the videos to customers on WhatsApp, and displayed the videos on their mobiles and laptops. These helped establish trust among agents, influence customers, and save time by communicating key product benefits, features and terms. Collaterals designed in unique shapes, such as bell tags, proved to be a good reminder for customers and led them to ask agents about insurance products. Customers found the in-store promotional collaterals self-explanatory and informative, so that they generated the desire to learn more.

“One-to-one customer interaction is inevitable in my business. The communication media helps me create awareness about the product and enhance enrolments. Audio-visual aids are time-saving and they engage customers with less effort.” – Agent in Damoh, M.P

“One-to-one customer interaction is inevitable in my business. The communication media helps me create awareness about the product and enhance enrolments. Audio-visual aids are time-saving and they engage customers with less effort.” – Agent in Damoh, M.P

The communication toolbox empowered BC agents to promote the products requiring long-term financial commitments from customers. Agents could raise awareness, engage with, make the product and services more visible to, and serve customers. The increased engagement led to more enrolments and drove the adoption of insurance products among people from the LMI segments—a win-win for all.

At the time of writing, MSC and FIA Global have been scaling up the communication toolbox to support its 25,000 agents in their customer interactions and diversify their revenue streams. FIA Global also plans to integrate the communication toolbox in its existing digital communication system for BC agents.

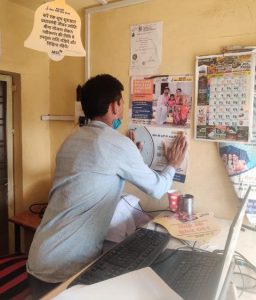

Figure 1: An agent using the collaterals at his outlet in Damoh

[1] A leading BCNM in India with a network of 25,000+ BC agents that serves rural areas

[2] Human-centred design principles are used in MI4ID (Market Insights for Innovation and Design), MSC’s flagship design thinking approach. It incorporates principles of behavioural economics and human-centred design.

Videos of women-led businesses’ program

Building agent trust among customers

In the podcast, Shelley and Graham discuss specific challenges of rural CICO agents that limit customer trust—identifying and recruiting suitable agents, branding practices followed by agents, liquidity support to agents, training to agents, and suitable agent monitoring. They also discuss the importance of fraud and risk management to sustain customer trust. Graham shares a few examples of how technology can build better transparency with agents while reducing the cost for providers. They also talk about a range of models being adopted in managing agent networks and the role of the government in expanding agent networks into rural areas. The podcast concludes with a discussion on the struggles oral customers face, which limits the uptake of DFS.