This report studies the effect of the COVID-19 pandemic on key elements of the health system framework across the Indian states of Uttar Pradesh, Bihar, and Odisha. These elements include community demand—health-seeking behavior and access to healthcare; provision of health services—human resource, infrastructure, and logistics; and community health workers—ASHAs. The report highlights insights from the supply and demand sides and provides key recommendations to better prepare the healthcare system of India to tackle shocks like the COVID-19 pandemic.

MSC (MicroSave Consulting), with support from the Swiss Capacity Building Facility (SCBF), conducted a workshop, “Assessment of the impact of COVID-19 on MSMEs in Asia and Africa” through a webinar on 28th January, 2021.

In this webinar, panelists discussed the impact of the pandemic on financial health, especially of the MSME sector and low- and moderate-income populations across Asia and Africa. Other topics of discussion included key opportunities that continue to emerge from this pandemic and how donors and governments can help these sectors recover. The key themes for discussion were as follows:

The impact of COVID-19 and coping strategies

The response of the government and donors to help low- and moderate-income populations and MSMEs mitigate the impact of the pandemic

The impact of the pandemic on MSMEs, especially on women entrepreneurs

*3:39: – 25: 46 Anup Singh, Regional Head—Anglophone Africa, MSC gives a presentation on the impact of COVID-19 on low- and moderate-income (LMI) populations and micro, small, and medium enterprises (MSMEs) in Asia and Africa

*26:44 – 27:31 Graham Wright, Group Managing Director, MSC welcomes the panelists and introduces the topic for the first round of discussions, “The impact of COVID-19 and coping strategies”

*27: 32 – 29:40 Evelyn Stark, Financial Health Strategy Lead, MetLife Foundation talks about the effect of the pandemic on people’s financial health and their attitudes toward formal financial services

*30:35 – 35:22 Mike McCaffrey, Regional Manager—East and Southern Africa, United Nations Capital Development Fund (UNCDF) responds to Question 2: “What have been the key highlights of the response of the government and donors to COVID-19 in Africa? How adequate have these measures been in addressing the financial crisis of the low- and moderate-income populations?”

*36:17 – 45:44 Mark Napier, CEO, FSD Africa responds to Question 3: “As a key market facilitator in Africa, how do you see COVID-19 impacting the inclusive finance sector?”

*46:42 – 52:53 Payal Dalal, Senior Vice President, Social Impact, International Markets, Mastercard Center for Inclusive Growth responds to Question 4: “What is the impact of the pandemic on MSMEs, especially on women entrepreneurs? What key challenges do you see in the growth of the MSME sector post-COVID-19?”

*53:52 – 1:10:23 The panelists respond to round one of the questions from the audience

Question 1) Would the loan demand be different across the poverty levels of households and MSMEs?

Question 2) Digital payments are in place but in the absence of an ecosystem, cash is the final destination. Any thoughts on this?

Question 3) Please see if this makes more sense—Lower income people have been borrowing extensively during the pandemic through mobile loans. We have heard that banks and microfinance institutions have been re-scheduling the loans as most people are unable to repay them due to the ongoing pandemic. How will this affect the economy?

Question 4) Does the MSC Foundation offer programs in SSA that tackle for instance, pre-investment TAs in the form of training sessions and grants?

*1:10:29 – 1:11:41 Graham Wright introduces the second topic on building resilience and the way forward. He gives a data point from the Kenya study on farmers. Graham notes that farmers’ margins have contracted by 38% and this could reflect across different sectors.

Second topic: Building resilience and a way forward

*1:11:44 – 1:17:29 Evelyn Stark responds to Question 1: “How has the current crisis been shaping the strategies of the MetLife Foundation to support the financial inclusion of the poor? How has it helped build a coordinated response to support recovery? Is there a need to re-focus financial inclusion, considering COVID-19 has undone years of inclusive finance initiatives?”

*1:18:40 – 1:26:31 Mark Napier responds to Question 2: How can financial markets effectively address the financial constraints of low- and moderate-income populations and MSMEs and help these segments survive and recover from the pandemic?

*1:27:18 – 1:32:21 Payal Dalal responds to Question 3: What key opportunities have been emerging from this pandemic that can further the financial inclusion agenda amid the current health crisis? How is Mastercard Center for Inclusive Growth working to realize these opportunities?

*1:34:10 – 1:42:39 Mike McCaffrey responds to Question 4: What are the innovations that financial services providers can use to assist recovery from the pandemic?

*1:42:57 – 1:50:32 The panelists respond to round two of questions from the audience

Question 1) Has the enterprise finance gap increased in recent years? Can there be a dynamic measure of this gap that can be regularly updated to measure the interventions focused on reducing the gap?

Question 3) Why can we not have situations, such as in most sensible nations, where long-term leases are signed but the rent is paid monthly or quarterly. Why do private landlords have to further cripple businesses through this unfair practice?

1:50:49 – 1:55:04 Sitara Merchant, CEO, Swiss Capacity building Facility, presents the concluding remarks

MSC with support from our generous donors Bill and Melinda Gates Foundation, Metlife Foundation, Swiss Capacity Building Facility, and Mastercard Foundation conducted a research exercise to assess the impact of the COVID-19 pandemic. We examined the needs, attitudes, perceptions, and behaviors of micro and small enterprises, farmers, and CICO agents in several countries including Kenya, Uganda, India, Indonesia, Bangladesh, Senegal, and the Philippines.

MSC and Swiss Capacity Building Facility(SCBF) launched the new reports on the impact of the COVID-19 on the low- and moderate-income populations as well as micro, small, and medium enterprises (MSMEs) in Asia and Africa, through an interactive webinar on 28th of January, 2021.

In Bangladesh, general holidays, falling consumer demand, and massive layoffs have affected all sectors of the economy. For the 2 million MSMEs that operate in the country, this has caused severe disruptions in the supply chain and a drastic reduction in revenues. 69% of businesses, mostly engaged in retail trade of essential commodities, remained operational while the remaining 31% were shut.

Our report highlights the impact of COVID-19 on the MSME sector in Bangladesh, particularly on micro-enterprises. It also provides policy recommendations to support the recovery of this sector.

Indonesia’s booming digital economy has also provided a favorable landscape for FinTech to flourish in the country. The country has a vibrant FinTech ecosystem, with more than 300 FinTechs innovating across different product and service categories. The digital-lending FinTechs operate using person-to-person (P2P) lending methodology and are by far the biggest segment of Fintechs. The P2P lending sector is one of the few that operates under a defined regulatory framework.

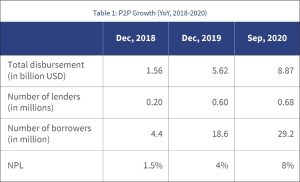

P2P platforms grew significantly from only six companies in 2016 to 156 companies in September 2020. The growth was spurred by a combination of investors willing to back their business models and a massive need for financing, especially for 64 million-plus MSMEs. These P2P players serve a wide range of segments, including individual consumers and MSMEs. Their loan ticket sizes can start as low as USD 7 for the consumer segment and go up to USD 675,000 for MSMEs.

Growth of P2P lending platforms in Indonesia

The following table shows a seven-fold increase in the number of P2P borrowers with a corresponding six-fold increase in loan disbursement in the past three years.

Despite the growth, P2P lending is mired in consumer protection concerns

Though the P2P lending sector has seen exponential growth, it has always been on the regulator’s radar due to the growing number of unregistered or illegal P2P lenders. Such lenders have often flouted the consumer protection guidelines laid down under the regulations. From 2018 until October 2020, OJK had blocked 2,923 illegal FinTech lending platforms.

P2P lenders have also drawn a lot of flak due to their unethical collection practices and abuse of personal data of their clients. Furthermore, P2P lending is mostly centered in urban locations and does not necessarily target underserved segments. For example, the distribution of FinTech lending outside Java Island is only around 14% out of the industry’s total loan portfolio of IDR 128.7 trillion (USD 8.9 billion). While this may put the willingness and ability of P2P lenders to accelerate financial inclusion under question, the reason behind the varying levels of financial inclusion across the nation is also geographical. Notably, infrastructure levels across major island groups in Indonesia vary widely, which affects the ability of service providers to offer their solutions.

Pandemic has puts pressure on the P2P lender’s growth and repayments

Indonesia is reeling under the economic pressures posed by the pandemic and has fallen into its first recession in 22 years. The large-scale social restrictions (PSBB), falling consumer demand, and massive layoffs have affected Indonesia’s MSMEs during the COVID-19 pandemic. Our study shows that revenues for MSMEs have almost halved since the pre-COVID levels and the supply chains at large have been disrupted.

The pandemic has seriously impacted the FinTech sector as well, particularly the P2P lenders that rely heavily on the growth of the MSME sector and consumer spending. As can be seen in figure 1 below, the average monthly growth rate for the new portfolio has fallen while repayment rates have started to fall since the onset of the pandemic in March.

In a bid to support the ailing economy, the Government of Indonesia (GoI) launched the National Economic Recovery Program (Program Pemulihan Ekonomi Nasional or PEN) under Government Regulation Number 23/2020. The regulation authorizes the top 15 licensed banks (in terms of asset base) to channel the PEN funds to designated sectors. A critical intervention of the program is financial support for MSMEs, for which it has allocated a budget of IDR 123 trillion (USD 8.4 billion).

Critical support measures for MSMEs include interest rate subsidies, a moratorium on principal repayments, and extension of loan tenures. These measures apply to all the three major MSME loan programs of the Government of Indonesia: KUR (people business credit), UMi (ultra-micro loans), and Mekaar . For interest rate subsidies alone, the government has allocated a budget of IDR 6.4 trillion (~USD 451 million) to target 8.33 million MSMEs.

Despite the scale of these programs, the GoI has relied heavily on the more traditional channels for distribution. These include state-owned banks, such as BRI, Mandiri, and BNI. In the past few years, the incumbent providers have struggled to meet their mandates for credit disbursement. Therefore, relying solely on these channels to deliver credit during such uncertain time may impede GoI’s efforts to stimulate economic recovery, especially for the MSME sector that will rely heavily on subsidized credit to restart operations in the post-pandemic period.

Opportunity for P2P lenders to support the government’s economic recovery efforts

Given the restrictions in movement, FinTechs have an important role to play in the efforts toward national recovery, especially for the delivery of social assistance. Countries like Singapore and the Philippines have utilized FinTechs to aid in COVID-19 relief initiatives. P2P lenders in Indonesia can significantly complement GoI’s programs, given their ability to implement agile digital delivery processes, especially for loan origination, KYC, credit assessments, and disbursements.

The government and state-owned banks have contracted established P2P lenders to channel loans under PEN mandates, as shown below.

During the pandemic, members of AFPI (the industry association of P2P lenders) compiled and collected data on 25 million MSMEs across different sectors and segments to support the government’s efforts. Besides these initiatives, FinTechs are also most capable of boosting the digital capabilities of MSMEs, a key priority area for the Indonesian government in its path toward economic recovery.

While all these are positive developments and a testimony of the sector’s latent potential, the pandemic may also encourage a revamp of the existing policy framework on the delivery of KUR and UMi loans. The GoI may consider including P2P lenders in the list of eligible service providers for the distribution of KUR and UMi loans.

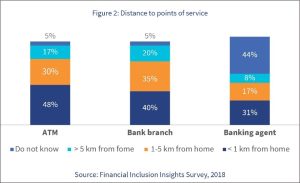

However, collaboration with incumbent financial institutions, which have some physical presence in remote areas, may soon become the most suitable operating model for P2P lenders. With the digital payment ecosystem still evolving, especially in rural areas, MSMEs may still need to cash out the disbursed funds through a financial access point such as agents, ATMs, or bank branches. The chart shows the presence of financial points near residential communities in Indonesia.

An effective mechanism of incentives and risk sharing will be essential to encourage the participation of P2P lenders in the delivery of government loan programs. The business model of P2P lenders depends on platform fees that range between 3%-5% and varies depending on the risk profile and customer segments. Given that the owners of many unserved and underserved MSMEs are not tech-savvy and lack digital trails for credit assessment, the P2P lenders may also need to modify their existing delivery processes— which are completely digital.

Such an adjustment may mean additional costs as service providers may incorporate delivery processes that would require physical touchpoints. The GoI need to recognize the existing infrastructure levels in the mandated locations to ensure providers are willing to go deeper and deliver in underserved segments—often in collaboration with existing, traditional financial services providers.

Another key consideration for GoI is taking care of the data protection, to ensure beneficiary data is being collected, stored, and processed in a secured and responsible manner as per the regulatory framework highlighted in the Personal Data Protection Bill. This is critical, given the target segment of KUR and UMi loans, typically underserved micro-enterprises, that might be even more vulnerable to data misuse and digital frauds than the current P2P borrowers, which include SMEs and young millennials.

Despite all the challenges, Indonesia’s FinTechs have matured in the past few years. Their digital products and delivery processes have gone through multiple rounds of iteration as they have tried to serve a more diverse range of customer segments. Now is the time for policymakers to utilize its potential to extend the delivery of the government’s social assistance program and accelerate the efforts to achieve meaningful financial inclusion, especially for 63 million strong MSME sector in Indonesia.

Note:

This blog assumes an exchange rate of USD 1 = IDR 14,500

For the past seven years, Neelam Devi has provided banking services to her fellow villagers in the remote villages of Sonepat in Haryana. She began her journey as a banking agent or business correspondent (BC) when there were only a handful of BCs across the country. Now, Neelam is one of the top-performing BCs in the state. Her simple manta for success? “Hard work and dedication”.

“It has been a memorable journey with challenges, solutions, and lessons along the way,” says Neelam when asked about her experience as a BC. Since the onset of the COVID-19 pandemic in India, Neelam has served her village relentlessly, providing essential banking services to her customers, including women and senior citizens.

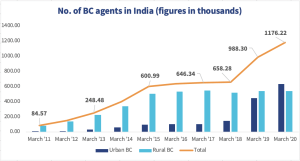

For more than a decade, BCs like Neelam have played a pivotal role in achieving financial inclusion in India. With vast geography to cover and a huge population to cater to, BCs remain the backbone of last-mile banking and payment service delivery across India. As highlighted in figure 1, as of March 2020, more than 1.17 million BCs were providing banking services to the people in the country. These BCs act as an important channel for the delivery of direct government benefits to nearly 800 million poor people and were instrumental in delivery of social assistance benefits during the COVID-19 pandemic.

BCs take center stage during COVID-19

On 24th March, 2020, the Government of India announced a nationwide lockdown to curb the spread of COVID-19. The government also announced a relief package worth INR 1.7 trillion (USD 23.17 billion) for the poor and vulnerable under the PM Garib Kalyan Yojana. As part of the package, an amount of INR 500 (USD 6.82) was transferred to more than 200 million PMJDY women’s accounts each month for April, May, and June. The government also front-loaded the first installment of INR 2,000 (USD 27.26) to all PM Kisan beneficiaries in April, covering around 87 million farmers. Senior citizens, widows, and physically handicapped individuals received financial assistance of INR 1,000 (USD 13.63) under the National Social Assistance Programme (NSAP).

“With most beneficiaries of the relief package residing in rural geographies, BCs acted as a bridge between them and the government,” says Neelam, who disbursed these cash benefits to numerous customers during the pandemic.

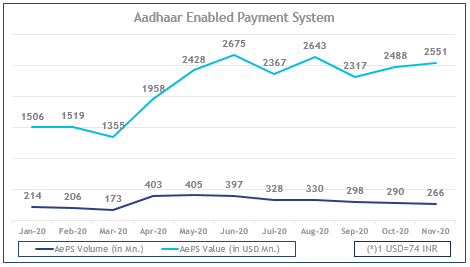

April 2020 saw a month-on-month growth of 133% in overall Aadhaar-Enabled Payment System (AePS) transactions, as captured in figure 2. Around USD 4.17 billion cash benefits had been transferred to the beneficiaries by May 5, 2020. A large part of these payments was withdrawn using AePS, which registered USD 2 billion worth of transactions in April, 2020. Interestingly, this trend continues even after stimulus package is over. While the number of transactions are gradually moving towards the pre-COVID levels, value of those transactions continues at above USD 2 billion. Payments banks, such as IPPB and Fino Payments Bank, used AePS and thus provided a significant stimulus to the number and value of transactions processed through this channel. With Paytm Payments Bank also starting to provide Aadhaar based transactions, AePS transaction values sustained. Reports indicate that BCs disbursed huge amounts of money every day when lockdown restrictions were at the peak, which provided relief to many needy people. India Post alone disbursed USD 56.16 million in a month. It

BCs faced numerous challenges during COVID-19

Nonetheless, BCs continued to face challenges, which were further aggravated during the pandemic. These issues prevent the BC model in India from performing to its full potential in response to such emergencies. The top three key issues and some potential solutions are:

Liquidity management: Cash management is important for a BC, especially during the times of monthly remittances and transfer of government benefits, such as payments under the PM Garib Kalyan Yojana as well as pension and other benefits. Traditional BCs located in remote areas find it difficult to replenish cash. Providers can look at distributor-based liquidity management practices that new-age BCs have adopted in urban locations. For remote or rural locations, providers should allow preferential access to agents for rebalancing, if a distributor-based option is not feasible. According to Neelam, support with cash management would help her perform better, especially in times of high use, particularly emergencies, such as natural calamities or pandemics.

Authentication failures with AePS: Transaction failure in any payment system can hinder seamless service delivery. According to a report, the average percentage of failed AePS transactions was 39% in April 2020. The numbers ranged from 10% to 62% across different providers. According to another report, a huge surge in cash-out transactions during the lockdown was one of the reasons behind transaction failures. Taking cognizance of the capacity of intermediaries, the regulators have advised banks and other service providers to follow best practices and reduce technical They have also revised the AePS architecture to balance the load on various servers. This raises concerns about the infrastructure capacity of intermediary providers. In addition, some issues continue to persist, such as the improper capture of fingerprints despite multiple attempts.

Our discussions with providers reveal that the measures taken have helped, and significantly reduced the technical decline of non-financial transactions. Nonetheless, some of the issues around business decline due to biometric mismatch limit breach, insufficient balances, and so on for financial transactions continue. Supply-side players can provide an additional biometric authentication option like an IRIS scanner to resolve one of the major issue. BCNMs like Stree Nidhi in Telangana have successfully integrated the IRIS feature with their Andhra Bank BCs. “While failure rates have improved significantly, transaction failures in AePS remain an issue,” says Neelam. After the announcement of the government’s relief packages, Neelam noticed a surge in non-financial AePS transactions at her outlet. “There were many occasions where transactions were declined because of authentication failure. So we started dissuading people from conducting non-financial transactions like balance enquiry – that seemed to take the pressure off the system,” says Neelam.

Insurance cover for BCs: Unforeseen circumstances like COVID-19 and natural calamities leave front-line professionals vulnerable to the situation. BCs provide essential services to the people during these trying times, but face risks associated with their health and possibility of accidents as they visit bank branches and sometimes provide doorstep services. Supply-side players can consider provisions for both health and accidental insurance for BCs. Some BCNMs, such as Basix Sub-K provide the Hospicash (a small value medical insurance to cover hospitalization and related expenses, otherwise not covered) facility to their BCs, but many are yet to take concrete steps in this regard. Neelam believes an insurance cover for BCs will be a welcome move and suggests the possibility of sharing the insurance premium amount among the BCs and banks.

Concluding thoughts

The BC channel in India is one of the most effective ways to provide the underserved segment with low-cost banking and payment services. However, the model struggles with many prevailing issues, including its agility to cope with emergency scenarios like COVID-19. BC agents are essential for the last-mile delivery of financial services across the country, as has been made clear by their role in DBT transfers during the pandemic. Acknowledging their importance, the government, regulators, and other supply-side players need to find feasible solutions for the key issues mentioned above. This will help not only committed agents like Neelam to prosper but also enable the underserved segments in remote locations to access better services.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.Ok

For the past seven years, Neelam Devi has provided banking services to her fellow villagers in the remote villages of Sonepat in Haryana. She began her journey as a banking agent or business correspondent (BC) when there were only a handful of BCs across the country. Now, Neelam is one of the top-performing BCs in the state. Her simple manta for success? “Hard work and dedication”.

For the past seven years, Neelam Devi has provided banking services to her fellow villagers in the remote villages of Sonepat in Haryana. She began her journey as a banking agent or business correspondent (BC) when there were only a handful of BCs across the country. Now, Neelam is one of the top-performing BCs in the state. Her simple manta for success? “Hard work and dedication”. For more than a decade, BCs like Neelam have played a pivotal role in achieving financial inclusion in India. With vast geography to cover and a huge population to cater to, BCs remain the

For more than a decade, BCs like Neelam have played a pivotal role in achieving financial inclusion in India. With vast geography to cover and a huge population to cater to, BCs remain the  April 2020 saw a month-on-month

April 2020 saw a month-on-month