The session included discussions around how catalytic financing can drive the supply of climate adaptation finance for the agriculture sector, especially for smallholder farmers who remain most vulnerable to climate change’s impacts.

The discussion intended to address the following questions:

Why do we need to mainstream climate adaptation finance for the agriculture sector?

How can catalytic finance help with the issue?

How is the impact investing community responding to this need?

Click on the timestamps from the webinar stream to hear specific segments.

Prasun Das elaborates on the need to finance climate adaptation finance for the agriculture sector. He highlights the necessity of knowledge collaboration, coherent policies, innovative financial instruments, and effective networks to overcome the barriers to green finance for smallholder farmers, who comprise most of the global agriculture sector.

Sandeep Bhattacharya, Advisor, Climate Change at GIZ, speaks about the initiative by Sustain Plus Energy Foundation and CINI to create farmer collectives called Production Hubs. He explains that these hubs use various technologies and practices to boost their income sustainably while facing challenges around maintenance, cost, scalability, and refinancing.

Krati Garg, Manager, Innovative Finance, KOIS, suggests that impact investors can help climate businesses attract commercial finance that balances impact and returns by using catalytic finance, standard impact measurement frameworks, and impact monetization.

Click on the timestamps below to watch the specific segments.

Chapters

04:29 – What is Lending SAAS? 08:30 – What was the trigger to start Roopya Money? 11:41 – Explain the business to a 5-year-old kid. 13:05 – How did you approach the building of the SAAS platform for the Indian lending industry? Given that the lending process is varied with such broad requirements, what were the underlying principles for you to design and build the product? 24:45 – Let’s talk business – what’s your model to earn? What is your cash cow? Other avenues that will open up. 29:19 – Are Indian lenders willing to open up for a lending SAAS? What are the underlying challenges you have faced? 36:10 – What’s your take on AI, especially with new-age generative AI impacting the financial technology industry? 39:06 – The RBI has recently given more clarity on the partnership between fintech and REs. FLDG has also received in-principle approval. Do you think REs may prefer to go with fintechs instead of investing to build their own stream of borrowers? 45:07 – India Stack is evolving – AA and OCEN and ONDC have become the buzzwords. How do you think Roopya can add value or gain from this ecosystem? 49:59 – How do you think India’s SAAS industry will shape up? What are the blind spots and opportunities? 52:11 – How does the acceleration by FI Lab help Roopya? How it can help scale the solutions. Any pearls of wisdom for both budding entrepreneurs and accelerators?

In developing nations, underserved people rely on agriculture, livestock, forestry, and allied activities for livelihoods. However, these sectors still struggle with technological advancements, particularly in digitalization. Innovations like AI/ML, blockchain, IoT, and large language model-based applications have emerged, but they face challenges like fragmented solutions, inadequate collaboration, and lack demand-driven reach. Initiatives like the AgriStack program and Integrated Digital Farmer Services Platform in India can help overcome these barriers.

Various digital solutions have emerged as potential game-changers in how the agri-food market functions and productivity-enhancing solutions are delivered. What constrains the potential of these innovations? If we take a systems perspective on the agri-food sector, we must consider three broad inter-related aspects:

Integration and coordination in value chains

Diffusion of innovation across value chain participants

Financing innovation end-to-end

If these solutions are to be effective, actors in the development sector need to mobilize a strong collective effort. They should determine how to harness digital technology to address the practical problem of change—many of which fall within the locus of these three areas. Finding viable routes to financing potential transformation pathways to resilience will be decisive.

The support is divided into four workstreams: (i) an active, efficient, and capable CICO network; (ii) a suitable product for underserved segments; (iii) streamlined G2P and bulk payment processes; and (iv) a comprehensive ecosystem of merchants to drive digital transactions.

MSC’s support has helped IPPB grow and increase its revenue by 140% in the past three years, from FY 2020 to FY 2023. Such impressive growth and significant contribution to financial inclusion (47% of all accounts are women’s accounts) have attracted attention from across the globe.

The IPPB model offers many lessons postal banks can replicate in other developing countries. Delegates, including the Bill & Melinda Gates Foundation Co Chairs and visitors from 25 countries, such as Africa and South Asia, have recently visited IPPB financial camps. They showed a keen interest in IPPB’s low-cost distribution strategy supported by robust technological solutions.

IPPB was launched in 2018 to provide accessible and affordable banking services to every household in the country. Since then, IPPB has used India Post’s extensive and trusted network of155,000+ post offices and129,000+ postal agents (GDS) to deliver banking and payment services. Thanks to its extensive network, the IPPB now reaches underserved and unbanked customer segments at their doorstep.

In a world striving for a brighter future, where no one is left behind, access to social protection becomes a crucial lifeline. It serves as the key that unlocks the doors to ending poverty, achieving universal health coverage, and reducing inequality by 2030, as outlined in the Sustainable Development Goals (SDGs).

Governments and regulators worldwide have recognized the power of social protection programs (SPPs) as instruments to uplift impoverished populations and combat the effects of inequality. Governments worldwide have planned or implemented more than 1,100 social protection programs, which cumulatively benefit more than 1.8 billion people who have been ravaged by COVID-19.

However, even with these efforts, the most vulnerable groups still remain overlooked. Homeless individuals, differently-abled people, transgender communities, indigenous populations, and migrants often find themselves excluded from the safety net these programs should provide. Shockingly, only one in three people with severe disabilities worldwide receive disability benefits, and a mere 23% of migrants possess any form of social security documentation. Clearly, these vulnerable groups, especially women, are in dire need of social protection payments.

This blog is an attempt to shed light on the major challenges these marginalized populations face when accessing social protection programs in developing countries, such as India, Indonesia, and Bangladesh. Read on to explore recommendations to address these obstacles and design targeted interventions that ensure social protection becomes a reality for those who need it most, and in the process, create a fairer, more equitable world for all.

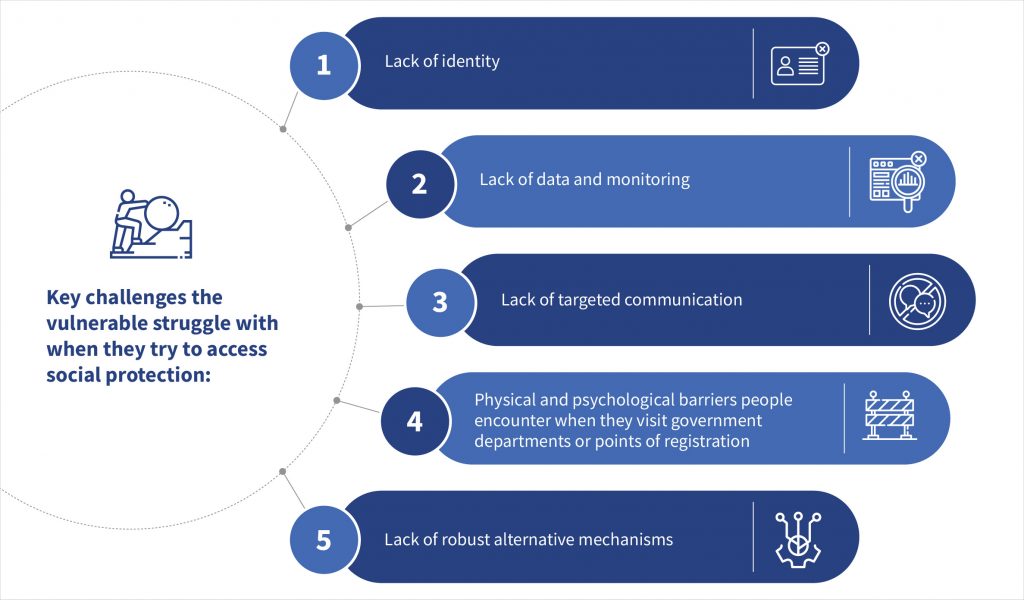

Key challenges the vulnerable struggle with when they try to access social protection:

1. Lack of identity

A substantial hurdle vulnerable populations face is the lack of proper citizenship documents to establish their identity. These groups cannot apply for social protection benefits without formal identity proof. For instance, the 2019 State of Aadhaar report found that 27% of transgender people in India lack an Aadhaar (digital identity). This is problematic for a country that otherwise succeeded in expandingAadhaar, as around 99.9% of residents have an Aadhaar card. Similarly, discrimination against transgender people is prevalent in Indonesia, as they are often excluded[1] from government safety net programs due to a lack of national identity (KTP).[2]

Other vulnerable groups, such as homeless people, have the most acute need for food security, health, and shelter assistance. Yet they are excluded from their entitlement as they lack identity documents. When subsidized or free services, such as basic education, health, and food security are offered only after the identity verification of individuals, it is a worrying aspect that the majority of the most excluded and marginalized still face bottlenecks in establishing their identity.

2. Lack of data and monitoring

Without identity documents, any credible data on vulnerable groups and monitoring their inclusion in social protection programs proves challenging. Many governments in developing countries, including India, Indonesia, and Bangladesh, have created social registries to automatically include the targeted population groups in the social protection programs. However, the most excluded groups remain outside these databases and must visit the government offices several times to register for a new program.

3. Lack of targeted communication

Communication on various programs and policies available for vulnerable groups is weak and poorly targeted. Most governments do not direct or customize awareness-building efforts for vulnerable communities, which leads to exclusion and reduced opportunities for direct engagements with the government. In particular, indigenous groups, differently-abled people, migrants, and homeless people are more susceptible to missing out on critical information on the social assistance they are eligible to receive.

People from these vulnerable groups often lack access to communication mediums, such as television, radio, internet, and phones, which further deprives them of information from the government. For instance, despite a robust social assistance package announced by the Indian government during the COVID-19 outbreak, the 1.7 million homeless people in India faced significant challenges in receiving them. Ironically, states with 60% of India’s homeless population did not even announcing the relief measures.

4. Physical and psychological barriers people encounter when they visit government departments or points of registration

Vulnerable communities, such as transgender people, often face exclusion and harassment from society, which compels them to shy from government offices. The last-mile workers at public offices and financial institutions are not sensitized to deal with such vulnerable groups, which often leads to their mistreatment.

A study conducted by the Indonesian Puzzle Community with transgender people in 2020 revealed 84.2% of respondents had a poor experience accessing public services as they lacked ID cards. People from such groups also struggle with barriers related to culture, norms, fear, and geographical location that further restrict their access to SPPs.

5. Lack of robust alternative mechanisms

Governments have created alternative solutions for vulnerable people to ensure they do not miss their entitlements even when they fail to meet the documentation-related conditions. However, the design of such alternative mechanisms often fails to address fundamental issues.

For instance, as part of their thrust on digitization, most governments in developing countries extend social protection by transferring cash into bank accounts or mobile money wallets. However, homeless people and tribal groups are excluded as they largely lack accounts or wallets. During the COVID-19 outbreak, the Indian and Bangladeshi governments announced cash assistance. Yet these did not reach homeless people because they lacked bank accounts.

Policy changes and interventions that need consideration to reduce the exclusion of the most marginalized and vulnerable in social protection programs

Developing countries have distinct national experiences regarding vulnerable populations and related laws and guidelines. They could consider developing customized interventions based on the following strategies and approaches.

1. Inclusion through identity

First, governments should ensure a foundational identity for the most vulnerable to roll out specific measures to bridge the last-mile gap in social protection for them. Micro-surveys, proofing through community workers, the local police, NGOs, and alternative mechanisms that permit registrations without birth certificates would open access to public services for vulnerable populations.

Further, vulnerable populations, such as homeless people and migrants, risk losing their documents as they lack a permanent place of residence. Governments should explore new technology approaches, such as decentralized identity systems, for easier recording and authentication of vulnerable groups.

2. Extend and expand alternative mechanisms for registration and assistance delivery

Vulnerable populations need flexibility in how they submit their documents and receive assistance. For such people, governments should allow flexibility to permit expanded, alternative options for them to prove their identity and eligibility. For instance, many states in India now provide doorstep assistance to differently-abled people, while Bangladesh has eased certain rules on providing identity to orphans.

3. Sensitization of last-mile workers

Last-mile workers include government officials and bank agents. They need to be sensitized to treat all applicants without bias against their gender, identity, income, or residential status. This can reduce the social stigma, fear, and resistance of vulnerable communities when they visit public offices. Such sensitization measures will further increase the interaction of such communities with the government, leading to better data collection and monitoring to expand social protection entitlements to the vulnerable communities

4. Targeted communication and awareness building for vulnerable people

Governments should adopt a bottom-up, community-based approach to deliver messages to vulnerable communities. Frontline workers, NGOs, community leaders, and labor associations should work to build awareness of the available assistance, entitlements, and rights of vulnerable and marginalized groups.

5. Develop a vulnerability index to customize social protection programs and policies

SPPs cannot be designed using a “one-size-fits-all” approach. Some population groups are more vulnerable than others. For instance, communities in Indonesia are prone to tsunamis, earthquakes, and volcanic eruptions that destroy homes and communities. The governments should develop a vulnerability index based on demographical, occupational, and climatic patterns to identify the most vulnerable people. For instance, governments should prioritize and include in the safety net ecosystem populations with disabilities, displaced people or those on the brink of losing shelter, people from highly remote areas, or people who live in disaster-prone areas.

Developing countries must take specific measures to build and strengthen their existing institutional structures to develop targeted policies for vulnerable populations. A focused approach will plug current gaps in accessing inclusive social protection and extend coverage of the vulnerable in the social protection system substantially by 2030.