What lies ahead for Bangladesh’s DFS market?

by Akhand Tiwari and Bhavana Srivastava

by Akhand Tiwari and Bhavana Srivastava Nov 21, 2016

Nov 21, 2016 5 min

5 min

The Helix Institute of Digital Finance recently concluded the second wave of Agent Network Accelerator (ANA) study in Bangladesh which found signs of growth in the digital financial services landscape in Bangladesh on all the key performance metrics*. Thsi this blog to understand why we feel that Bangladeshi market is poised for the next level of digital financial services. S

The Helix Institute of Digital Finance recently concluded the second wave of Agent Network Accelerator (ANA) study in Bangladesh which found signs of growth in the digital financial services landscape in Bangladesh on all the key performance metrics*. The number of providers, agents, and users –all have increased since the previous wave of the study was conducted in 2014 and the research indicates that the Bangladeshi market is poised for the next level of digital financial services. Service providers are likely to lead this wave of change, while the regulator – Bangladesh Bank, and agents will play their respective parts in contributing to it. You may call us victims of optimism bias, but study findings and interaction with various stakeholders clearly indicate that the market already has a good appetite for better digital financial services – or DFS 2.0, as we refer to it in this blog.

Providers will lead the change

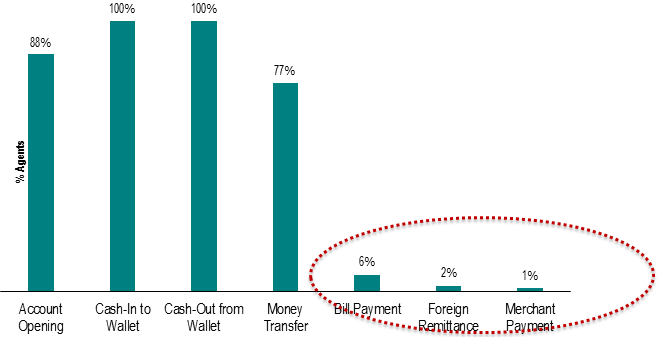

The current DFS product offering in Bangladesh is limited to the basics – account opening, cash-in/cash-out transactions, bill payments and money transfers, although bill payments and merchant payments have a negligible presence in the product suite (Figure 1). Compared to other factors that contribute to successful DFS ecosystems – players, agent networks, technology, customers, and products, the Bangladesh market is still nascent, in terms of the range of products and services. The country shows positive growth trends and is comparable to other ANA countries in terms of the training and liquidity management of its agent network.

More Bangladeshis are embracing DFS and it is likely that providers may want to offer them more than the basic wallet and P2P services. We predict that providers will begin to focus on diversifying and offering more sophisticated products.

Figure 1: Products offered by by Agent in Bangladesh

Agents also noted that “individual clients’ demand for (DFS) service is not regular”. This perception could be largely due to the P2P nature of the market which is not predictable as it is governed by a degree of migration in the market. The demand might become regular and/or predictable if there are more use-cases in the form of sophisticated products by providers that motivate more usage and uptake of DFS offerings.

As DFS market continues to evolve, acquiring a large customer base that understands and uses digital financial services is critical (Davidson and McCarty). We believe that the Bangladeshi market has reached this critical juncture and providers have attained a customer base ready to use more sophisticated financial services.

Bangladeshi providers have much to learn from the success of African markets where digital financial services have successfully offered savings and credit services – KCB-MPESA, M-Shwari, Equity Bank, are all shining examples. There are also examples of agents offering savings, credit, and insurance products. These experiences, irrespective of whether they were successes or failures, provide immense literature and learning on customer behaviour towards a credit product or role of agents in offering insurance products. This will be hugely beneficial to the providers in Bangladesh in designing both products and strategies.

Fortunately, all DFS providers in Bangladesh are banks or their subsidiaries. Unlike non-banking providers who lack expertise in the area, banks, in general, are far more proficient in designing banking products. The changing landscape of new product development that involves big data and Behaviour Economics principles will further help banks to design products that are tailored to meet the critical financial needs of customers. All these factors add weight to our optimism about DFS 2.0 in the country.

Agent optimism will support the launch of more complex financial products

The ANA study found that Bangladeshi agents are the most optimistic ones among all the ANA markets – almost all agents see themselves continuing as agents for another year. About one-third (31%) of agents in Bangladesh are high performing, that is, they conduct more than 1.5 times the country median level of transactions. Agents are critical to the development of digital financial services, and a happy army of agents is one of the most useful assets for a provider. There is, therefore, a good probability that agents in Bangladesh would be willing to promote and service complex financial products. The road to agent management, however, is not without its own challenges, as with more sophisticated products, agents will be more prone to fraud. The data shows that fraud has risen three percentage points – from 19% in 2014 to 22% in 2016.

Support from the Regulators will be key

It is worth noting that the regulator in Bangladesh supports both – mobile financial services (mostly wallet based payments offered by the banks) as well as agent banking (to promote bank-branch like experience for customers). We reckon that the competition for market share between these two models will catalyse the development of more sophisticated products. The objectives of both models are largely the same – increasing the penetration of financial services and achieving financial inclusion. Although there is a slight variation in the basic modus operandi of the two models, agents appointed by the bank play a key role in both of them during customer interaction. The best practices of agent management have already been established for the market, therefore, the next phase will be about providers competing to get the customer value proposition right. It is time to wait and watch how providers who offer either MFS (for example bKash) or agent banking (for example, Bank Asia), try to win customers over; and how provider(s) who offer both type of services (for example, Dutch-Bangla Bank) consolidate their value propositions. We believe that these two guidelines (agent banking and revised mobile financial services), will create opportunities for developing more complex financial products. The push for DFS 2.0 will, therefore, be greatly determined by how regulation facilitates this while ensuring customer protection at the same time.

Markets evolve in terms of the products they offer; Kenya evolved from ‘send money home’ to ‘payments’ to ‘get credit on the phone’ and beyond. India evolved from no-frills accounts to Basic Savings Bank Deposit Accounts to Jan Dhan Yojna accounts. In Bangladesh, the stage is now set for the evolution of the DFS ecosystem to take place.

*The data referred to in the blog is taken from ANA Bangladesh Report 2016, unless otherwise referenced

Written by

Akhand Tiwari

Partner

Leave comments