UPI 123Pay: The four-leaf clover for feature phone-based payments in India?

by Pramiti Lonkar, Shweta Menon and Akshat Pathak

by Pramiti Lonkar, Shweta Menon and Akshat Pathak- Oct 10, 2023

- 6 min

by

by  Oct 10, 2023

Oct 10, 2023 6 min

6 minUPI broke all records in August 2023. It observed 10.586 billion transactions that amounted to INR 15 trillion (~USD 189.64 billion). It has become the preferred payment choice for digitally-savvy Indians. However, it cannot reach the feature phone users. Its penetration is limited to urban segments with high usage of smartphones and mobile Internet. India is home to 400 million feature phone users. These users have limited avenues for digital transactions. They largely depend on physical access points for financial transactions. This blog discusses an innovative offline payment solution, UPI 123Pay, and its immense potential to bring digital payment convenience to the underserved segment.

Nitesh is a 31-year-old autorickshaw driver who migrated from Katihar in Bihar state of eastern India, to Delhi for a better job. He earns ~INR 700 (~USD 8.55) per day. After covering his basic living expenses, Nitesh saves approximately INR 11,000 (~USD 133) monthly. He remits this money to support his family back home in Katihar. For a long time, Nitesh used informal channels for remittance, such as hawala and over-the-counter (OTC) agents.

Although Nitesh found it convenient to send his savings monthly through these channels, the commissions charged by the agents bothered him. He tried to use alternate modes, such as the USSD-based mobile banking service *99#. Yet he found the process cumbersome and time-consuming. Nitesh is comfortable using a feature phone and does not want to upgrade to a smartphone anytime soon. He is keen to try UPI 123Pay to transfer money to his family. However, he wonders if it is safe and if he can use it independently.

More than 400 million feature phone users in India like Nitesh have limited alternatives for digital payments on their feature phones. They continue to depend on physical access points for financial transactions. To cater to this segment of feature phone users, the National Payments Corporation of India (NPCI) integrated its USSD channel *99# into the Unified Payments Interface (UPI) ecosystem in 2016. *99# allows users to conduct financial and non-financial services using their mobile phones without using the internet. It aimed to make payments easier for users, especially those with feature phones. However, there has been limited uptake of the solution among the LMI segment for multiple reasons. One of the primary reasons for the limited uptake is the complicated payment process involved in *99# with a non-intuitive user interface. Subsequently, the transaction volume for *99# decreased significantly from 2.44 million in 2017 to 1.47 million in 2022, indicating a need to develop new and innovative solutions to facilitate payment for the feature phone user segment.

The launch of UPI 123Pay

With 10.586 billion transactions amounting to INR 15 trillion (~USD 189.64 billion) in August 2023, UPI has broken all records and has become the preferred choice of payment for digitally savvy Indians. Transactions conducted through UPI also create digital data trails for users. However, UPI’s penetration is limited mainly to the urban segments with high smartphone and mobile internet usage.

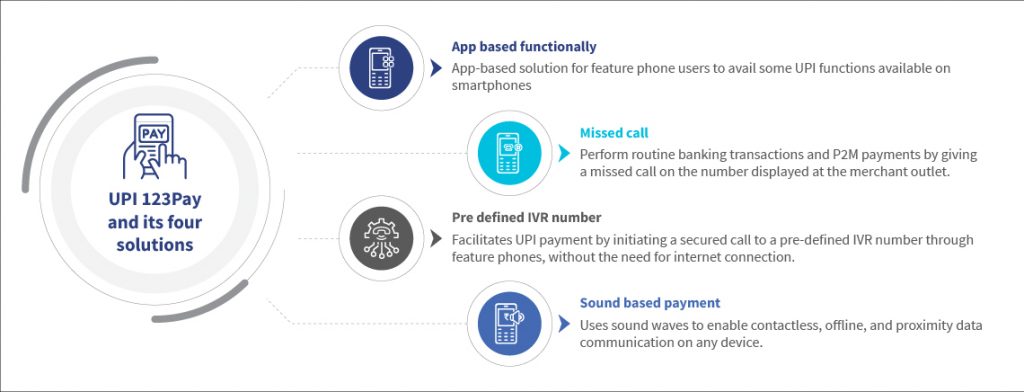

In March 2022, the Reserve Bank of India (RBI) and NPCI launched UPI 123Pay to offer digital payments to underserved segments of feature phone users. UPI 123Pay facilitates payments for feature phone users without needing internet connectivity. Through this, users can initiate payments to peers and merchants using UPI. The UPI-powered solution also supports smartphone users who prefer operating offline or with minimal internet connectivity. The current use cases of UPI 123Pay include utility bill payments, FASTag activation and recharge, mobile recharges, and fund transfers, among others. Users can undertake these transactions based on the following four technology alternatives that are currently live:

While smartphone users can also use UPI 123Pay, its primary target market comprises the underserved segment of feature phone users who are still dependent on the last mile access points or their friends/family for their financial transactions. Customers in remote locations often incur high costs, including travel costs, waiting at the business correspondent (BC) outlet, and the wages foregone when making periodic visits for their cash requirements. Wide-scale adoption of UPI 123Pay would significantly reduce these costs while improving ease of access for P2P and P2M payments for feature phone users.

Another challenge for people using digital payments, especially the feature phone segment and those in rural areas, is the lack of an active debit card. Most users of this segment struggle to keep their debit cards active due to low account balances, limited infrastructure for card acceptance, and limited knowledge of how to use the cards. Further, according to the latest data published by Global Findex, the debit card penetration in India is just 27%, and the majority of these users are based out of urban areas. The lack of active debit card limits a large chunk of the rural population to try and experience the digital payment convenience offered by UPI.

To solve for these issues, in September 2023, NPCI introduced the alternate onboarding process for UPI using Aadhaar + OTP. This is expected to simplify the process for feature phone users and help increase the uptake and usage of UPI further. The Aadhaar-based onboarding process is available to users in addition to the existing onboarding process using debit cards. UPI 123Pay is available in six vernacular languages: Hindi, Tamil, Telugu, Malayalam, Kannada, and Bengali. NPCI plans to introduce other languages as well. This would help resolve another significant barrier for feature phone users.

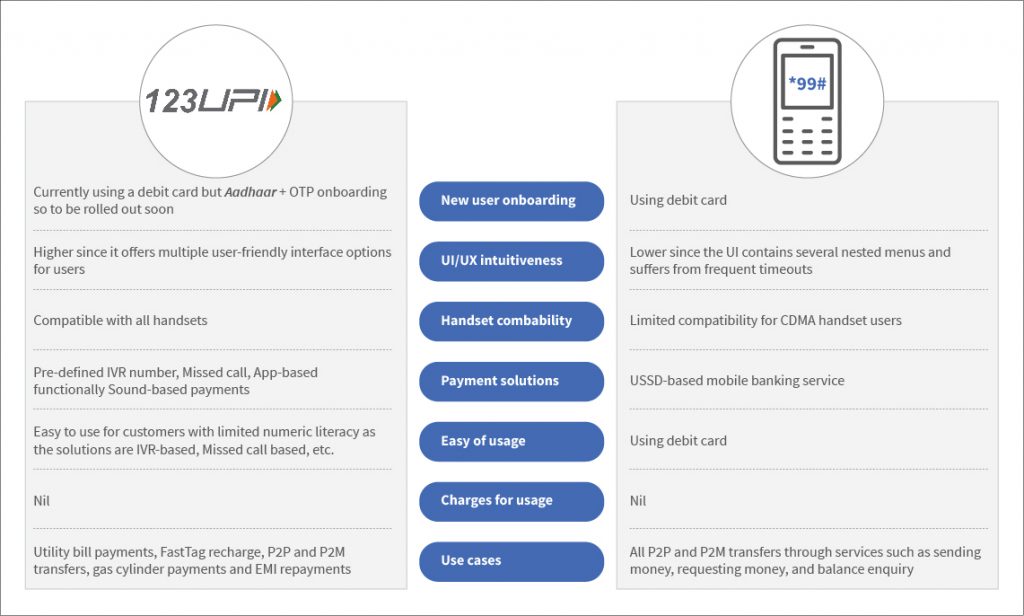

Furthermore, UPI 123Pay has also factored in the network and internet connectivity issues in remote and rural areas. All four solutions are built on technologies that work offline and do not require an internet connection. A look at the critical differences between *99# and UPI 123Pay highlights the different pain points that UPI 123Pay addresses for the feature phone users:

Barriers to the usage and scalability of UPI 123Pay

Barriers to the usage and scalability of UPI 123Pay

While these offline payment solutions offer massive growth opportunities in the feature phone users market, the uptake for UPI 123Pay has been slow since its launch in 2021. Major traction for the product is for use cases such as LPG gas cylinder payments, P2P payments, and mobile recharges. The solutions look promising and manage to overcome several barriers associated with *99#; however, a few concerns limit the uptake of UPI 123Pay among users. MSC’s analysis of the use of the IVR solution highlighted some critical insights into the process experience of UPI 123Pay for customers.

1) Limited comprehensibility of the users’ voice input

Users often have to pronounce their bank name multiple times while generating the UPI PIN, as the input gets disrupted due to differences in pronunciation or background noise. While users can also type the bank name as an alternative, the voice input provides more ease and convenience than the text input and is preferred.

2) Lack of a ‘favorites’ option

The solution currently does not have the provision to remember customer preferences such as frequent payee names’, frequently conducted transactions, or even the transaction history. This results in users undertaking these processes repeatedly, leading to a longer TAT that impedes the process experience.

3) Limitations in the current interface

First-time users, especially those with limited numeric literacy, require some assistance in onboarding while entering their debit card details and generating the UPI PIN. Hence it is not a completely independent process for the feature phone users in its current form. Users with limited digital readiness usually depend on others for transaction completion. MSC’s recent report “Decoding the extent and exposure of financial fraud among DFS customers” suggests that users’ dependency on others coupled with low digital readiness exposes them to financial fraud and risks. The risk increases even more for women users which is a major deterrent to the uptake of digital financial services among women.

Limited use cases in the IVR solution

Currently, the solution offers users limited use cases to transact. Recent MSC research for NPCI highlights the need to introduce use cases such as fee payments, postpaid bill payments, and rent payments, among others, to improve the uptake of the solution. While NPCI is working on adding new use cases, it will be critical to include use cases that cover the entire journey of a user’s financial needs lifecycle.

Conclusion

India’s ~400 million feature phone user base offers a massive opportunity to drive digital payments growth and unlock the USD 10 trillion opportunity by 2026. On the acceptance side, around 12 million Kiranas (hyperlocal neighborhood provision stores) account for 80% of the retail sector in India, with 90% being unorganized or self-organized and most digitally excluded. UPI 123Pay can help these merchants scale their operations through digital commerce. While UPI for smartphones continues to soar high, UPI for feature phones remains a new concept for many.

To further extend the usability and adoption of UPI across different segments, NPCI conceptualized Hello!UPI to make digital payments easy, accessible, and safe for users. The voice-activated payments solution is an extension to UPI 123Pay and allows users to use their voice for conducting transactions. Hello!UPI is available through two modes currently: on-call (through a voice call), and in-app (through any UPI app). MSC’s recent whitepaper on conversational payments (developed jointly with NPCI) suggests that the solution has immense potential to disrupt the payments space and bring millions of underserved users who are constrained by the lack of smartphones, Internet connectivity, and limited digital literacy into the folds of digital payments. All these are strong and positive steps to build pathways to a safe and inclusive payment ecosystem. Concerted efforts from NPCI and other stakeholders to develop inclusive payment solutions will benefit millions of underserved users like Nitesh and support them to kickstart their digital payments journey.

Leave comments