The potential of merchant payments in Cote d’Ivoire: What is the situation in the informal sector?

by Nadine Zoro

by Nadine Zoro- Mar 19, 2019

- 4 min

by

by  Mar 19, 2019

Mar 19, 2019 4 min

4 minThis blog helps us to understand merchant behaviour and barriers while looking at opportunities that will help in the adoption and active usage of mobile money merchant payment solutions among businesses in Cote D’ Ivoire.

Merchant payments has been a top priority for digital financial service providers in 2018. However, the activity rates of acceptor merchants and customers remain low, according to GSMA’s report on the mobile money industry. The adoption of merchant payments in Côte d’Ivoire has been limited, where two mobile phone operators, MTN and Orange, dominate the market.

In November, 2017, MicroSave Consulting (MSC) conducted a diagnostic study on the success factors of merchant payments solutions using e-wallets. We conducted the study with 93 accepting merchants, which revealed that only 5% of payments are made via the merchant solution.

Our study surveyed 255 non-accepting merchants to assess the potential of merchant payments with the Ivorian business fabric. These merchants represent the economic diversity in Abidjan. According to a survey on the informal sector in Abidjan conducted by the National Institute of Statistics of Côte d’Ivoire, there are approximately 610,000 informal production units of non-agricultural market activities in Abidjan. Around 40% of the turnover is from informal trade.

The size of the informal sector in Côte d’Ivoire is considerable and its contribution to the overall Ivorian economy is significant. Hence, the integration and development of merchant payments in this sector could have a multiplier impact on the overall adoption of digital financial services. Our study points out some encouraging attributes of the informal sector.

Merchant payments: An alternative to cash?

Since its launch in 2016, the businesses that the merchant payments solution mainly targeted are the trade chains and large supermarkets that operate in the formal sector. Indeed, our diagnostic study of the Orange Money and MTN money merchant payments networks indicates that 75% of merchant acceptors of merchant payments are supermarkets, petrol stations, pharmacies, and large bookstores. This strategic choice is understandable given the large geographical scope of these businesses, which are generally part of national trade chains. However, the rate of use of the merchant payments solution in these businesses remains minimal, with only 5% of the total volume of transactions carried out via this payments solution compared to 80% in cash.

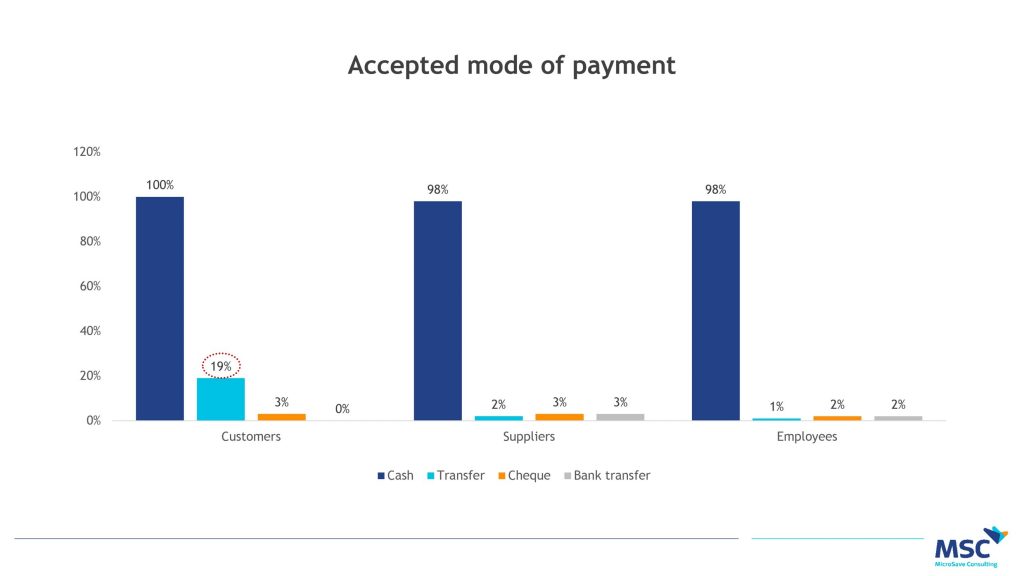

Informal sector businesses, which represent 95% of our non-merchant sample, are largely untapped in the expansion of merchant payments. They, however, face many challenges that merchant payments could try to solve. These businesses rely heavily on cash to manage their business (98%) and have limited access to money security and savings and credit options. These merchants are nevertheless aware of the problems generally associated with cash management, such as change, counterfeiting, as well as loss and theft of money, among others.

A majority of businesses identify the lack of loose change as the major problem of cash in the local market. Merchant payments come at the right time since it offers a solution to this problem through digital payments or provision of change. This trend points to the possibility of the proposed merchant payments solution being able to target informal sector businesses that existing suppliers hardly manage to serve.

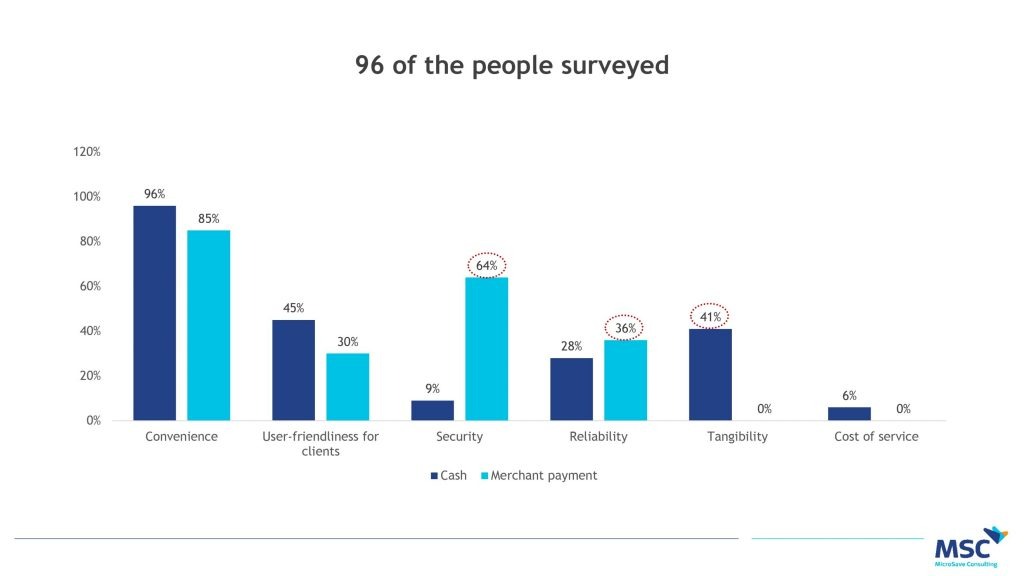

Moreover, merchants who currently use the merchant payments option find that it has attributes that could meet the needs of businesses in the informal sector. They consider merchant payments to be more secure and reliable than cash or any other means of payment. Businesses deplore the possibility of losing money or having it stolen, in addition to incurring unnecessary expenditure by having cash on hand. Since cash is too liquid and can be easily misused, there is a need for access to money security options and tools that promote financial discipline. Merchant payments, therefore, appears to be an appropriate solution to meet the needs: security and reliability.

Furthermore, most transactions in developing countries are still carried out in cash, as confirmed by the majority of the traders in our study sample.

Does technology have a place in the informal trade sector?

Our study shows that a small proportion of businesses (32%) use technology and the Internet to manage their activities. However, personal ownership of technological devices is high, with 90% of people owning a technological device and one-third owning a smartphone. This confirms GSMA’s report on the mobile economy, which notes that telephone penetration in Côte d’Ivoire is 53%. Secondly, in a local environment where the activity rate of mobile money accounts is below 35%, almost half of the traders surveyed (45%) have an active mobile money account. Therefore, we note that neither the ownership nor the use of a mobile money account—often cited as structural barriers as a previous MSC study suggests—constitute an obstacle to proposing a market solution for the informal sector traders interviewed in our study.

P2P transfers allows customers to send the purchase amount directly to the trader’s personal account. Indeed, traders who accept P2P transfer payments prefer mobile money transfers for large transactions and state security reasons associated with possessing physical cash as the main reason for this preference. Field observations from our study suggest that businesses accept P2P transfers for regular and trusted customers or for paying geographically remote suppliers.

The volumes of transactions and recognized business opportunities in this sector suggest that it is possible to develop a use-case specifically for micro and small informal sector companies that have already adopted the P2P mobile money transfer service for business purposes.

So what can suppliers do to seize opportunities in terms of adopting and using the service as well as making the offer profitable?

Lessons for merchant payments service provider

Suppliers could review their network segmentation strategy and target micro and small businesses. By using person-to-person transfers for commercial purposes, they could design a product for informal businesses. This product could focus on the problems of change, and the need for security and access to financial services.

However, given the specific nature of operations in this sector, we need to factor in aspects, such as convertibility of electronic money, the administrative documents required, and transaction costs.

Leave comments