Survival, recovery, and building resilience: Transformation of financial institutions in the times of COVID-19 – Part 1

by Anup Singh and Graham Wright

by Anup Singh and Graham Wright Aug 13, 2020

Aug 13, 2020 5 min

5 min

The COVID 19 global pandemic has affected the lives, health, and livelihoods of entrepreneurs, and they have been struggling to repay loans from financial institutions. This blog highlights recommendation from MSC for financial institutions to survive in the wake of COVID-19.

In the bustling City Park Market in Nairobi, Philip runs a fruit stall. The market has other fruit stalls but they are no match for his excellent service, which delights customers. His efforts have grown his business in the past 12 years since he began. Philip attributes his success to regular access to credit from a financial institution. His business has not always grown steadily though and came to the brink of collapse, twice.

The first time Philip almost had to quit his business was in 2016, immediately after the government imposed an interest rate cap when the market saw a squeeze in general credit. The second time Philip’s business hit a roadblock was in 2017. The election crisis in the country led to a lot of uncertainty and economic instability. In both cases, Philip was optimistic and indeed his business recovered in due course. Yet with COVID-19, he has lost all hope.

Philip is not unique. He represents over 300 million enterprises from emerging economies across the world. The global pandemic has affected the lives, health, and livelihoods of entrepreneurs, and they have been struggling to repay loans from financial institutions. These financial institutions face a vicious cycle, as poor asset quality continues to pressurize both liquidity and profitability. The financial crisis may erode a decade of gains in financial access if financial institutions cannot get timely support.

The global pandemic also amplifies the need and opportunity to initiate digital transformation. Such a transformation will be both a response to this crisis, which may well persist for years to come if no fully effective vaccine is found, and a response to an increasingly uncertain future. Viruses mutate, so this year’s vaccine may not be effective next year, as is the case with the flu. Moreover, as humanity’s destruction of the natural environment continues, similar future pandemics become more likely.

In this and the next in the series of blogs, we discuss how donors and investors should support financial institutions during this uncertain time.

The following are some recommendations from MSC for financial institutions to survive in the wake of COVID-19.

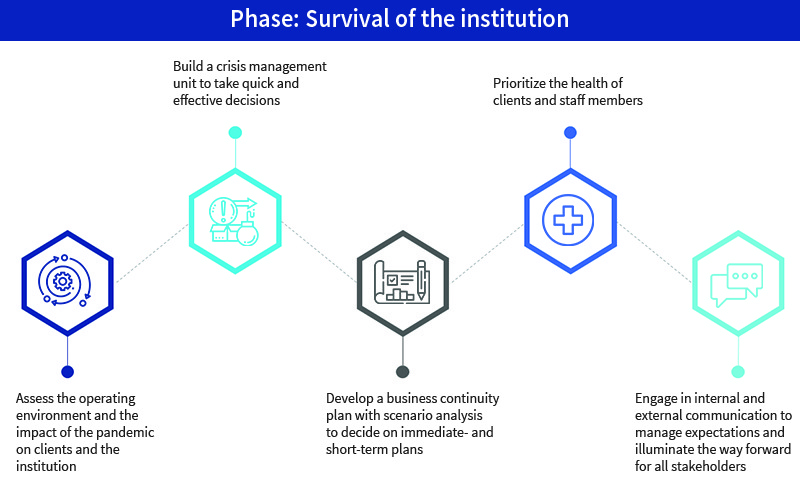

1. Assess the operating environment and the impact of the pandemic on clients and themselves

Financial institutions need to understand their new operating environment to build survival strategies. Governments have implemented several policies and measures for financial institutions. The institutions must assess these measures and see how best to use them to benefit from the policy, regulatory, and supervisory frameworks.

Financial institutions must assess the impact of the pandemic on the financial sector in the country. The institutions may also assess how COVID-19 has affected the clients. A dipstick assessment of the impact of their pandemic will help to understand the needs, attitudes, perceptions, and behaviour of customers. This will determine how best an institution can prioritize various strategic steps to support the recovery.

Financial institutions must assess the impact of the pandemic on the financial sector in the country. The institutions may also assess how COVID-19 has affected the clients. A dipstick assessment of the impact of their pandemic will help to understand the needs, attitudes, perceptions, and behaviour of customers. This will determine how best an institution can prioritize various strategic steps to support the recovery.

Financial institutions should assess the impact at an institutional level to determine steps to survive, recover, and build resilience. Some aspects the institutions may focus on include:

a) Financial aspects including capital adequacy and funding structure, funding mix, and use of financial instruments to mitigate various risks;

b) Portfolio aspects, such as asset quality, concentration, and diversity;

c) Risk management strategies;

d) Human resources aspects to focus on redundancies, the impact on staffing levels, and the need to repurpose staff members to other tasks.

We must note that not all individuals and enterprises are the same. Our research on enterprises shows that 20% of businesses—the “essential services” in particular—have not been affected badly. Such businesses may be encouraged to continue to repay.

The financial institutions can then develop survival strategies using these insights.

2. Build a crisis management unit to take quick and effective decisions

As the first step, the institutions may build a unit to manage the crisis during and after the pandemic. Ideally, the unit should have executive powers and should be willing and able to take decisions immediately and proactively. The unit should develop quick strategic and institutional responses to manage the immediate- and short-term risks. These responses should be developed and implemented with an unwavering eye on the future and the institutions’ digital transformation strategy.

3. Develop a business continuity plan with scenario analysis to decide on immediate- and short-term plans

The next step would be to develop a business continuity plan across various time frames. The institutions may conduct stress tests across several scenarios to include assumptions around when the pandemic is going to end, what funding resources are or will be available, and which expense items may be rationalized. As the institutions build their business continuity plans, they must revise business plans in light of the emerging situation and the impact, build scenarios, and refine budgeting for the various scenarios. The institutions may need to optimize expenses, reduce costs, and revise product pricing accordingly.

4. Prioritize the health of clients and staff members

As the high-touch model of financial institutions has the potential to expose the staff members to the risk of infection, the institutions may need to create awareness among the staff members on health precautions. Staff could minimize the risk of infection during meetings with clients, serving clients, and handling cash. The institutions may focus on explaining the concepts of disinfecting facilities, social distancing, and the use of protective equipment. Institutions should also repurpose the role of field staff members to that of community health advisors. As part of demonstrating corporate good citizenship and caring for clients, field staff members should educate customers on preventive measures and guide those suspected with the disease to visit the right place for screening or testing.

5. Engage in internal and external communication to manage expectations and illuminate the way forward for all stakeholders

In the immediate term, financial institutions need to communicate well with staff, clients, donors, investors, and other stakeholders. The institutions may focus on internal communications around restructuring roles, safety and wellness of the staff, strategies for portfolio and risk management, and revised structures and job responsibilities. Further, the institutions may amplify external communications around the impact of the pandemic on client, staff, and portfolio, business continuity measures, portfolio and risk management measures, and regular updates on institutional responses.

In the next blog, we discuss how institutions may formulate recovery and resilience strategies to manage revival during the pandemic and in its aftermath.

An abridged version of this blog was first published on Next Billion.

Written by

Anup Singh

Associate Director

Leave comments