Financial stability is the key to financial resilience. Remittances in Senegal exceed USD 2.2 billion a year but neither do the beneficiaries have access to financial services nor are they digitally literate enough to plan for their future. In times of need, money transfers provide another means of reimbursement for the households.

Abdoulaye is a young entrepreneur who lives in the rural region of Louga, which lies in northeast Senegal. He lives in the family compound owned by his uncle, which comprises 8 adults and 15 children. Abdoulaye holds a Baccalauréat diploma and owns a business. He manages to bring home a monthly income of XOF 100 000 (USD 170) through diverse activities.

Every month, his brother, who lives in France, sends him XOF 150 000 (USD 250) through a money transfer company to contribute to the household expenses, such as food, utility bills, healthcare costs, and school fees, among others. His brother’s financial support has enabled Abdoulaye to launch his own business, as well as to start saving on an informal basis.

Abdoulaye owns a shop that sells a variety of products based on demand, which is often governed by religious celebrations that are a central part of Senegalese life. For instance, his business revolves around the sale of ceremony garments during local celebrations such as the Touba Magal or the Tabaski. In the lead up to Tabaski, he also breeds sheep and each sale brings in up to XOF 100 000 (USD 170). To increase his income, Abdoulaye also purchases sheep sometimes that he later sells at public markets. It is during this time of the year that his investment needs are the highest. When schools reopen, he focuses on the sale of school equipment. An entrepreneur at heart, Abdouldaye knows how to manage and grow his money.

Through his foresight and tenacity, Abdoulaye manages to bring home a stable income. However, as he remains in the informal sector, financial institutions are blind to his financial capabilities. He is an active member of two “tontines” ( savings groups ) and contributes up to XOF 30,000 (51 USD) per month. Simultaneously, Abdoulaye has managed to gather his own personal savings, which he keeps as working capital. It allows him to cover the costs associated with the operation of his business and the purchase of merchandise.

The nature of his business requires financial flexibility that banks and MFIs cannot provide with their high-interest rates and rigid reimbursement timelines. However, his primary and secondary incomes increase his credit rating and highlight his ability to reimburse.

Abdoulaye meets all the reliable and responsible customer characteristics set by financial institutions. However, he relies heavily on the remittances sent by his brother and on the informal borrowing and saving systems of his community.

Life would become much easier for people like Abdoulaye if financial institutions were to partner with money transfer companies to create digital profiles and develop an alternative credit history. This begs the question—how can financial institutions promote digital transactions to encourage entrepreneurs like Abdoulaye to reduce their use of cash?

Fertilizer subsidy is the linchpin of India’s support system for its farmers, who in turn help provide food security for the country’s 1.3 billion people. Thanks to its growing technological capabilities, India is primed to reform its fertilizer subsidy program, making it more efficient and economical. The key lies in connecting the subsidy directly to farmers, rather than giving it to fertilizer manufacturers based on the efficiency of the fertilizer manufacturing plant, as has been the case historically.

The government is already thinking about reaching farmers directly, and here we propose optimal models to do this.

The first step would be to draw up a list of all farmers who are eligible for the fertilizer subsidy, and to set a limit on how much they can obtain. Such a list and limits don’t exist today.

A well-targeted subsidy payment would benefit farmers, by ensuring that they get what they optimally require for agriculture. It would also benefit the environment, since a cap on the availability of subsidized fertilizers would likely stop the excessive use of fertilizers which, after all, end up in the food we eat.

By successfully rationalizing its subsidy program, India can also set an example for other developing countries, like Sri Lanka and Indonesia, which also subsidize fertilizers.

The Challenges of Subsidizing Fertilizer Use in India

India is the second-largest user of fertilizer in the world, after China, thanks to a vast geographic area being cultivated by more than 150 million farmers. Subsidies on fertilizers were introduced more than 40 years ago to make them affordable to farmers – and ultimately, to ensure food security for the country.

The subsidy bill has grown exponentially over the years. From just $700 million in 1990-91, it went to nearly $11 billion in 2017-18. Fertilizer is the country’s second-largest subsidy payment, after food. But this increase in expenditure hasn’t necessarily benefited farmers. An estimated 65% of the fertilizer produced does not reach the intended beneficiaries – that is, small and marginal farmers, according to government data.

A bulk of the subsidy is given in the form of urea, which makes up 70% of all fertilizer used in India. The government sets an artificially low price for each quintal (equal to 100 kilograms) of urea, which buyers (i.e.: farmers) pay to the retailer (i.e.: fertilizer shops). (These retailers are the last-mile touch-points that sell fertilizer to farmers on a commission basis. A retailer is given a license by the state government on the basis of a pre-defined selection criteria.) The gap between this sale price and the cost of producing the urea is paid by the government to the manufacturer.

Currently, there are no restrictions on who can buy the subsidized fertilizer, or on how much they can buy. This has led to the overuse of fertilizers in cultivation, and also to the diversion of urea to other industries (like dairy, textile, paint, fisheries, etc.) and to neighboring countries like Bangladesh and Nepal (through organized black market players who buy it in the guise of farmers and sell it for a profit).

Mindful of these leakages, the Indian government has been taking steps to reform the system, using technology. It implemented the Mobile Fertilizer Management System to digitize the fertilizer distribution supply chain. And in 2016 it took its most significant step, when it piloted a Direct Benefit Transfer (DBT) system to pay the subsidy. The pilot was followed by a pan-India rollout in March of 2018.

In the past, fertilizer manufacturers would get paid most of the subsidy amount shortly after the fertilizer left their warehouses, irrespective of sales. In the new DBT system, manufacturers get paid only after the retailer has sold the fertilizer to “authenticated” individuals. That means the buyer is required to prove his identity at the time of purchasing the fertilizer. The preferred identity card is Aadhaar — a nationwide unique identity card which includes the individual’s biometric information. The buyer also has to give his fingerprints on a Point of Sale machine possessed by the retailer. Once the Point of Sale machine verifies the buyer’s identity, the retailer sells them the fertilizer at the subsidized price, the sale is recorded in the fertilizer management system, and the proportionate subsidy is remitted to the manufacturer.

The biggest benefit of the DBT system is that, for the first time, it allows the government to know exactly who is buying the fertilizer. However, it’s important to note that the system doesn’t verify if the buyer is a farmer, since there is no database of farmers in India. In our research, we found that sometimes auto rickshaw drivers (to take one example) bought fertilizers which they said was on behalf of their farmer friends.

Still, despite these issues, the DBT system has made an impact – especially in increasing transparency. At the government’s request, MSC studied the program’s progress, and we found that retailers who were relying on pilferage (which had been more profitable than genuine commissions) might have left the system.

However, there is scope for more efficiency, and the government is already talking about switching to another system — one where it would credit the subsidy directly into the bank account of farmers. The government already provides such direct transfers for cooking fuel subsidies and pension payments. In these cases, a pre-defined amount of money is deposited directly into the beneficiary’s bank account. However, replicating this model for fertilizer subsidies is more complex, partly because the government doesn’t have a list of beneficiaries (i.e.: a database of farmers).

Solutions For Connecting Subsidies Directly with Farmers

For an optimal fertilizer subsidy transfer, the first order of business would be to create a list of beneficiary farmers, including tenant farmers (who farm land owned by others, paying rent with cash or with a portion of the produce). This won’t be easy, but existing databases like the PM Kisan list (which includes the registered farmers under the Indian government’s PM Kisan cash transfer scheme) can be a starting point. The next step would be to determine how much subsidy each beneficiary is entitled to, depending on the farmers’ land holdings, geo-climatic conditions, crop types, soil health status, etc.

On the question of how the subsidy would be transferred to the farmer, crediting their bank account is a popular idea. Farmers could then buy fertilizer at market price from the retailers.

The problem is, farmers don’t prefer this approach. According to our recent assessment, 65% of farmers in India don’t want to receive the subsidy via bank transfer. This is likely because they have faced many problems with similar programs in recent years, for instance, when they were supposed to receive bank transfers in lieu of a liquefied petroleum gas subsidy. They either never received the payment or it was delayed, and farmers fear the same would happen with the fertilizer subsidy.

Another concern is that if the subsidy amount is not available on time, it would increase their financial burden. They would have to buy the fertilizer at high, non-subsidized prices, and potentially be forced to borrow money to do so. Farmers today pay Rs 295 – 325 ($4 – $4.50) for a bag of urea, whereas its non-subsidized price would be between Rs 950 -1,100 ($13 to $15). To shell out Rs 1,100 per bag upfront would be too burdensome for many of India’s small farmers.

Then there is the hassle of banking. Farmers would have to make multiple trips to banking points to withdraw cash, and then another trip to the fertilizer retailer. These trips translate to lost opportunity costs for farmers.

So, until the government can fix all the hiccups in the bank transfer model, we propose an alternative model for the subsidy transfer: creating a virtual account for farmers. This wouldn’t be a bank account, but rather a digital record of how much fertilizer subsidy a farmer is entitled to, how much he has used, and what is remaining.

Here’s how it would work: A virtual account would be opened for all eligible beneficiaries on a government platform. At the beginning of India’s two major crop seasons, namely the kharif and rabi seasons, the government would credit the subsidy to the farmer’s virtual account. The farmer would get an SMS or a call on his registered mobile number, showing how much he is entitled to. (Most farmers in India now have access to a mobile phone.)

To buy the fertilizer, the farmer would authenticate himself with his Aadhaar card and the Point of Sale machine available at the retailer, then pay the subsidized amount. The gap between what he pays and the cost of manufacture would be deducted from the farmer’s virtual account. It would be transferred to the fertilizer manufacturer within a stated period of time.

This system would have two advantages. It wouldn’t create additional hassles for the farmer. He’d continue buying the fertilizer at the subsidized rate, without having to worry about whether the subsidy has reached his bank account or not. At the same time, the government would have better information about who is using the subsidy and by how much. In a way, it would further refine the Direct Benefit Transfer system that is in place now.

We recommend that the government commence a pilot for this model, since the infrastructure is ready. Once the banking and payment infrastructure is strengthened, the government can create a pilot for direct bank transfers.

Once farmers have had the opportunity to experience both models, the government will be able to determine the most suitable model for all stakeholders. We believe that both farmers and the Indian government will be quick to recognize the mutual benefits of this approach.

The blog was also published on Next Billion on 12th November, 2020

Remittances are about to become the largest source of external financing for West African countries, thanks to migrants who invest in their countries of origin. Yet the use of digital channels remains low among remitters and receivers. This report identifies barriers and opportunities in the use of formal remittances, and offers recommendations that address the needs and aspirations of both remitters and recipients.

The impacts of disasters and climate change events affect low-and moderate-income (LMI) individuals disproportionately. Disasters pose a greater risk to their lives and livelihoods. These events compromise the progress that the poor make to improve their living standards and emerge out of poverty. Inclusive financial services that transfer such risks and provide buffers for rehabilitation are the need of the hour. Financial service providers, including MFIs, cooperatives, and banks can play a pivotal role in offering risk transfer and management solutions.

In the first part of this two-part series, we discussed the macro landscape of disaster risk financing. In this part, we take a deeper look at microinsurance solutions that can and do enable LMI segments to manage and mitigate risks posed by climate change events. We draw from MSC’s experience with financial service providers and donor organizations in developing microinsurance solutions across emerging economies. We also examine nascent approaches that offer microinsurance solutions to address disasters and climate change and see how they can be delivered in a sustainable and scalable manner.

How does microinsurance address climate change risks and disasters?

Disaster risk microinsurance products are offered in two formats: pre-defined payout products and voluntary disaster risk insurance products. The latter offers a choice of coverage and premium bands for the insured. At present, such pre-defined cash benefit bundled products are the most common form of disaster risk (micro) insurance solutions. Standalone voluntary disaster risk insurance products on the other hand have gained importance only in recent years.

Below we see some examples of disaster risk microinsurance products:

VimoSEWA in India has offered a bundled disaster risk insurance product for more than a decade to members who suffer damages to their homes as a result of floods. This product offers a fixed payout of INR 10,000 (~USD 132) if damages occur as a result of the disaster event. Such predefined cash benefits are the most rudimentary form of offering disaster risk insurance to the LMI segment.

Pioneer in the Philippines provides disaster risk insurance bundled with credit products offered by CARD, its partner MFI. The beneficiaries receive a predefined payout for damages incurred or loss of life, or both, if a covered disaster, such as typhoons or floods occurs.

In partnership with GIZ Regulatory Framework for Pro-poor Insurance (RFPI) Asia and Department of Trade and Industry (DTI), Philippines, MSC developed business interruption disaster risk insurance for MSMEs in the Philippines. After math of disasters, the top priority is to get livelihoods back up, especially micro and small enterprises. We spoke to more than 100 MSMEs in the Philippines to understand how disaster risk (micro) insurance can help MSEs recover quickly. The efforts resulted in the design and pilot of a direct cash benefit product.

Pre-defined benefit microinsurance products and when do they make sense?

Microfinance institutions have long been offering credit-life insurance to their members bundled with their credit products. The credit-life insurance products cover death arising out of disasters in the loan tenure. We have also seen above, in the case of disaster risk insurance product in the Philippines, microinsurance products that cover damages caused by disasters being offered in a similar bundle. The benefits of such bundled products are predefined and capped at a certain amount. The payout is most often triggered when the covered disaster occurs.

For beneficiaries, a pre-determined payout makes sense because:

Immediately after a disaster strikes, what enterprises and individuals most require besides healthcare and rehabilitation infrastructure is cash infusion. This helps them cope with the effects of disasters that include loss of life and health and damage to business assets, and get back up. The availability of this infusion also provides the poor a buffer against falling back into poverty. A pre-defined payout is the simplest way to offer this support to beneficiaries when it matters the most.

For insurers, an insurance product based on a predefined payout is easy to roll out:

These products are designed and implemented simply, as they have a basic structure in terms of receiving benefit “X” if disaster “Y” occurs;

Such products generally do not require costly and time-consuming assessments of damage as the payouts are fixed and capped.

Payouts are triggered based on well-defined parameters, such as the breach of an index or a declaration by the government that a disaster has occurred; and

Such products are easy to bundle with existing credit and savings products that financial service providers offer.

Voluntary disaster risk products and challenges that insurers face in offering these solutions

MSC’s study of the climate change and disaster risk landscape in Asia and Asia-Pacific allowed us to see firsthand the dearth of disaster and climate change insurance products available for LMIs and MSMEs. This led us to ask, what are some of the obstacles that prevent more insurers from offering such solutions?

MSC’s engagements with insurers in the Philippines, Vietnam, and Bangladesh revealed that most property insurance solutions cover disaster risks through additional riders that provide additional risk covers against possible losses due to disasters and catastrophic events. These riders come at extra costs, over and above the property risk premiums. However, premium bands are largely driven by market competition, and not necessarily by technical risk assessments. (“fight to be the lowest bid”). This is a challenge for insurers, as a lack of diversity of their underlying portfolios and risk concentration drives them toward losses on the risk assumed.

Representatives from an insurer in the Philippines that offers bundled (with micro-credit) insurance against calamities like typhoons commented that its premium was established based on high-level assumptions and not on technical risk assessments. When Typhoon Haiyan struck, the portfolio incurred losses due to high risk concentration and large-scale payouts, leading the insurer to increase the premium by a steep 800%.

Events like super typhoons and their increasing frequency continue to upset such simplistic pricing models and draw attention to the need to improve the technical capacities of insurers to price the risks better based on reliable weather data and emergent climate change patterns.

Insurers in emerging Asian and African markets have limited technical capacity to develop accurate climate change and disaster risk models and have limited actuarial capacities to analyze such risks. This problem is aggravated by the limited availability of reliable and affordable weather data from weather stations and satellite imagery. A combination of these factors makes it difficult for insurers to serve the LMI and MSE segments. Poor infrastructure in rural areas also makes it costly to sell, administer, and service these products.

Making disaster risk insurance sustainable and scalable

Through our interactions with insurers in Asian markets (Vietnam, Bangladesh, and the Philippines, among other geographies), we elaborate on key support areas for micro-insurers to develop and offer disaster risk insurance for the LMI segments.

Source: MSC analysis

Access to technical capacity development

Product design and pricing create the foundation for the design of a sustainable disaster risk insurance portfolio. For LMI individuals, both pricing and access to the relevant product are significant constraints. Insurers need to better understand target segments that need disaster risk insurance products. Further, there is also a need to build actuarial capacities, given the enhanced risk of exposure in the face of disasters and other climate change events. The success of disaster risk microinsurance products would also depend on the insurer’s capacities in the following areas:

Marketing of disaster risk products;

Selling or pitching disaster risk insurance products to prospective clients;

Developing partnerships to expand distribution channels that LMI customers, including micro and small enterprises, can access with ease;

Accessing affordable re-insurance support for disaster risk microinsurance products.

Use of technology to overcome infrastructure challenges

Inadequate infrastructure for financial services in rural areas poses major challenges for insurers as it increases the cost of administering disaster risk insurance and compels more manual interventions at the time of onboarding as well as claims settlement. Technology could help ease this pain point for insurers by the use of:

Mobile phones and mobile applications for client onboarding, policy sales, and management;

Mobile money platforms for premium collection and benefit payments; and

Applications to monitor the product lifecycle, originate, and manage claims and declare benefits.

Policy-level support from governments

Disaster and climate risk insurance is a relatively new industry and its markets in developing countries are even more nascent. The industry will need policy support from governments to develop. This can be accomplished by:

Well-defined policy environment and regulations that offer tangible motivation to insurers to develop disaster risk coverage; examples of such incentives can be free access to reliable weather data and satellite imagery from state agencies, development of weather monitoring infrastructure like monitoring stations, and premium subsidies that target LMI segments, especially farmers

Making technical support accessible for insurers and financial institutions to build their capacities in disaster risk insurance planning and design and cover knowledge gaps in the industry; one great way of doing so is to allow for regulatory sandboxes that enable insurers to pilot new products and models

The way forward

Insurers in markets including the Philippines and Bangladesh tell us that they view disaster risk insurance as a commercial opportunity. As one insurer from the Philippines said: “We have a big population, the impact of disaster events ripples through all sections of the society, so there are risks and there is a market. All we need now are models, tools, and the technical capacity to offer commercially viable solutions that also provide customers value.”

To achieve this vision, insurers must build their technical capacities, engage better with clients to understand their needs, and design solutions accordingly. MSC’s proprietary HCD tool, MI4ID, for instance, is a tested mechanism through which insurers can address client needs as part of product design. Besides, insurers must adopt technology suited to reach even remote areas in rural villages to be successful in the long run. Governments also have a role to play through the provision of reliable data and technical capacity-building to the industry. Now is the time to create and provide scalable and sustainable disaster risk insurance solutions—to safeguard vulnerable populations from the uncertainties of changing climate.

Super Cyclonic Storm Amphan ripped through Bangladesh and the eastern Indian states of West Bengal and Orissa in May, 2020. It left behind more than a hundred dead and millions of lives disrupted. The financial damage is certain to be severe with West Bengal alone predicting losses amounting to USD 13.2 billion. Most of the damage was uninsured and had no disaster risk transfer mechanism in place.

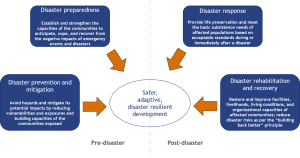

Responding to such disasters is a herculean effort. The top priority is always to save lives. MSC’s work on disaster risk financing projects has enabled our partners to understand the topic better and design need based solutions addressing the disaster recovery needs of the low- and moderate-income (LMI) segments, and MSMEs. Through a two-part blog, we summarize our experiences in the field of disaster risk financing and its application at regional, national, and consumer levels. In the first part of this blog, we provide an introductory, macro overview of layered disaster risk financing, while in the second part, we focus on disaster risk financing approaches from an inclusive finance perspective.

When Amphan struck, India and Bangladesh evacuated millions to safety well ahead.[1] Preparing for disasters and managing their impact has been standardized by most nations by now. The standard framework adopted to manage disaster response is summarized below:

Source: MSC analysis

The need for finance in disaster risk management

Disasters cause monetary losses by damaging physical infrastructure, assets, and lives. The absence of a risk transfer mechanism, therefore, makes rehabilitation even more expensive. Lending to rebuild is further complicated by the different types of disasters and their varied impact. Since the effects of climate change disproportionately affect poor communities around the world, disaster risk financing as a risk transfer mechanism therefore assumes critical relevance. Several stakeholders including policymakers, insurers, financial services providers, and entities are working to develop the resilience of LMI segments against climate change and disasters need,. They, therefore, need a well-grounded understanding of climate change and disaster risk financing mechanisms.

A layered approach to disaster risk financing

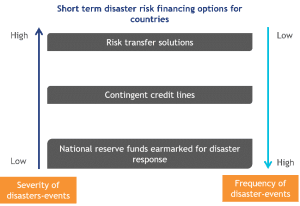

At the national level, a country can assess its risk financing options through a risk layering approach. The idea behind a risk layering approach is to identify the best-suited risk financing tools that are proportional to the severity of the risk and the fiscal capacity of the government. Simply put, disaster risk financing must be cost-effective, yet not compromise a country’s financing requirements at the time of a disaster. Layered disaster risk financing options are illustrated below:

Source: MSC analysis

In the following section, we briefly assess what each of these three layers of financing options entails.

The first layer is the national reserve funds, which generally refer to annual budgetary allocations, contingent budgets, and allocations made by a government in response to disasters. These funds are typically used to cope with localized, low-severity, but high-frequency events like floods, landslides, and earthquakes, etc. The economic capacity of a country would generally determine the amount of such funding. However, due to the implications of huge expenses, most developing countries find it difficult to fund large-scale anomalous disasters.

The second layer comprises contingent credit lines. These pre-arranged credit lines disburse loans to act as precautionary lines of defense in the event of disasters of medium to high severity and meet government expenditures over and above the disaster reserves.

An example of a contingent credit line is the Catastrophe Deferred Drawdown Options or CAT DDOs offered by the World Bank. This innovative contingent line of credit provides immediate liquidity to countries in the event of natural disaster. Funds become available for disbursement after the drawdown trigger—typically the member country’s declaration of a state of emergency. The full commitment amount is available for disbursement at any time within three years from the signing of the financing agreement.

The third layer is risk transfer solutions. The objective is to transfer the financial risks that arise from high-severity, low-frequency disasters from countries or individuals, or both, to a third party in place of a risk premium. Such solutions provide a contractual right to countries or individuals to receive pre-defined funds at the time of a disaster. These solutions can take the form of sovereign insurance or regional risk pools, CAT bonds, and consumer insurance solutions.

We discuss each of the risk transfer mechanisms in more detail below.

Sovereign risk pools

Through sovereign catastrophe risk pools, countries may pool risk in a diversified portfolio, retain some of the risks, and transfer excess risk to the reinsurance and capital markets. Since the likelihood of a major disaster afflicting several countries within the same year is low, diversification or “geographically spreading the risk” among participating countries creates a more stable and less capital-intensive portfolio. Sovereign risk pools are therefore, less expensive to reinsure. Examples of such risk pools are the Pacific Catastrophe Risk Assessment and Financing Initiative (PCRAFI)and South East Asia Disaster Risk Insurance Facility (SEADRIF).

CAT Bonds

A catastrophe (CAT) bond is a debt instrument that serves the dual purpose of raising debt and transferring financial risk in the books of the insurance companies. Countries that face disaster risks issues these bonds. Insurance companies and re-insurers are typically the sponsors who pitch the bonds to the potential investors. These instruments promise a higher yield to investors compared to traditional fixed income instruments. In normal circumstances, investors receive coupon payments along with PAR value at the end of maturity. In the event of a disaster, the sponsors suffer financial loss due to claims linked to prior indemnity, indexes, and parameters. In such a circumstance, the sponsors have the right to default on further payments to investors.

An emergent approach used by actors, such as the World Bank has been to combine a CAT bond with a Pandemic Emergency Fund (PEF). A PEF is a mechanism that provides additional financing as non-reimbursable grants in response to outbreaks with pandemic potential. The World Bank pioneered this approach in the Maldives.

Consumer-level risk transfer solutions

Consumer-level risk transfer solutions are insurance products or programs that provide coverage against disasters and natural calamities. Such solutions can be classified into agricultural and non-agricultural insurance solutions.

Agriculture insurance

Agriculture insurance solutions take one of two forms: state-supported or subsidized agriculture insurance and commercial agriculture insurance.

Agriculture insurance programs are an instrument of choice for farmers and rural communities to cope with the risk of disaster. The provision, administration, and oversight of agricultural insurance programs help a country manage the systemic risks of disasters, such as widespread drought or floods that affect a large number of farmers simultaneously. The cost of managing systemic risks that arise from catastrophic events and affect the agriculture sector is many times higher than the cost of premiums it would take to insure them. For example, the World Bank estimates that a widespread drought in India could generate crop-yield losses as high as three times the average annual crop loss experienced in a normal year. Traditionally, governments in India have mitigated crop failures or other natural disasters by providing post-disaster direct compensation as a relief measure, or through farmer loan waiver schemes—which while popular cannot be regarded as a sustainable mechanism to meet disaster-induced crop losses. The last major waiver in India in 2008 saw the government write off outstanding loans worth USD 7.8 billion for more than 30 million small and marginal farmers.

Insurance, on the other hand, not only reduces the cost of relief but allows governments to make fiscal plans for natural disasters and crop failures. It does so by well-defined premium subsidies for agriculture insurance taken by farmers, thereby allowing the government to gauge its proposed outlay and budget for it. In the event of a disaster, the insurance companies compensate the farmers from their own risk pools without government subsidies. Hence, insurance limits the government’s exposure when a disaster strikes while ensuring optimal risk coverage and compensating the losses of farmers. The biggest state-supported agriculture insurance program among emerging economies is the Pradhan Mantri Fasal Bima Yojana of India.

Non-agriculture disaster risk insurance

Non-agricultural disaster risk insurance solutions protect against damage to property and materials of value in the case of disasters such as floods, earthquakes, typhoons, and cyclones. While property insurance against risks like fire and theft is not new, coverage against disasters is nascent. Many micro and inclusive insurance companies have been experimenting with cash benefit products for low- and middle-income segments. These are typically pre-defined insurance products, where payout are triggered when the insured disaster occurs, irrespective of the damage incurred. We examine this in greater detail in part 2 of this blog.

Getting the disaster risk financing product mix right

Disaster risk financing tools and approaches to mitigate future losses should be a function of the types of disasters to which a country is most vulnerable, as well as potential future humanitarian and financial losses that could arise if such disasters occur. While incorporating the product design features of insurance, countries must also consider the requisite resources to rebuild the infrastructure that has been destroyed using better quality, disaster-resistant material.

Governments must strive for a portfolio mix of disaster risk financing instruments based on accurate risk assessments, desired coverage, available budgets, and cost efficiency. See the second part of this blog here.

COVID19 has affected women in many ways- financially, socially, physically, mentally. Response from policymakers and providers needs to be gender transformative so that fundamental gender issues like social norms, access to resources, etc are addressed. Can digital solutions help? What can be the design elements to develop truly gender centric programs, policies, and products to help women cope with the crisis brought by the pandemic?

Read our strategic insights to know more.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.Ok

Source: MSC analysis

Source: MSC analysis