Lessons from the Financial Diaries research with women traders in Kenyan open-air markets and cross-border trades

by Rahul Chatterjee, Elizabeth Gathu, Pauline Katunyo, Grace Kathure and Kim Kariuki

by Rahul Chatterjee, Elizabeth Gathu, Pauline Katunyo, Grace Kathure and Kim Kariuki- Sep 27, 2023

- 6 min

by

by  Sep 27, 2023

Sep 27, 2023 6 min

6 minFrom our financial diaries research, we present the stories of Janet and Rebecca, two inspiring women entrepreneurs in Kenya. Please read our new blog as they shed light on women’s financial realities in the open-air market and cross-border trade sectors in Kenya.

Janet and Rebecca count among the 2.7 million women entrepreneurs who work across Kenya. Janet is an open-air market trader (OAT) who deals in secondhand clothes in Gikomba, one of the country’s largest open-air markets in Nairobi. Rebecca is a cross-border trader (CBT) who operates across the Kenya-Uganda border daily. She supplies agricultural products to customers in the border town of Busia. Both women share several commonalities—they have regular customers, prefer cash payments, rely on informal financial services, and experience severe income volatility. Rebecca and other CBTs contribute to 30-40% of Africa’s regional trade, which is informal and women-led.

The cost and complexity to obtain permits, licenses, and registration push traders like Janet and Rebecca to operate informally. This exposes them to harassment from local authorities. Moreover, CBTs also face risks related to exchange when they manage multiple currencies. The lack of secure options to make cross-border payments exposes them to fraud and theft. As a result, multiple constraints prevent these traders from being able to use a range of digital financial services effectively.

Despite their contribution to economic development, we know very little about the financial lives of women OATs and CBTs in Kenya. This blog unpacks the financial lives of women OATs and CBTs.

Findings from financial diaries

The financial diaries approach is a famous research method within the development community. It tracks people’s personal and financial behavior to provide deep insights into their lives. It unpacks their economic realities, income sources, savings preferences, consumption patterns, and usage of financial services. Financial diaries have improved financial record-keeping among women and unlocked insights into the barriers informal urban women entrepreneurs face in Uganda. Moreover, diaries have increased women’s financial literacy and well-being in Bangladesh. The diaries method has been used extensively in the US, Kenya, and multiple other regions after its introduction in the Portfolios of the Poor.

MSC conducted financial diaries research with 100 traders, both OATs and CBTs, between April 2022 and June 2023. The research sought to unlock the economic and financial realities of women OATs and CBTs in Kenya. During this period, traders kept daily written records of their total income, personal and business expenses, savings, and loans. Field researchers visited these diarists every two weeks, performed quality checks, and digitized the records for analysis. Three months after the research was completed, we found that 49% of the traders continued to keep such records. This finding reinforces the idea that diaries can improve financial habits in low-income settings.

Our analysis led to several interesting insights. We have highlighted some below:

Business volatility

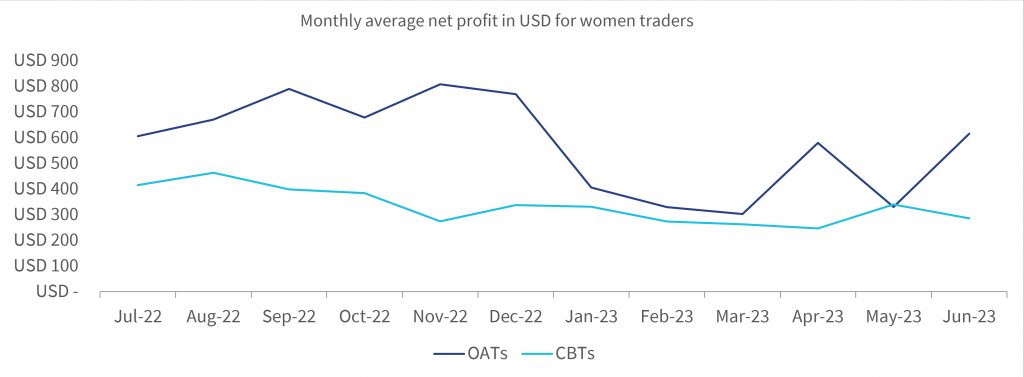

On average, women OATs, such as Janet, generated 31% more revenue than their CBT counterparts. However, their expenses are similar. OATs gained huge revenues in December due to the festive period, but CBTs did not. In contrast, CBTs experienced a slump in business activity, aggravated by the country’s worsening economic conditions. Other factors that explain the income and expense variation include geography, seasonality, business size, type of business, and captive customer base.

Variations in business income and expenses lead to higher net income for women OATs than women CBTs. Moreover, the decreasing trend in the net income for Janet and other OATs is significant based on the Mann-Kendall Test but not for women CBTs.

Janet and other OATs also cite various challenges that limit their business expansion, which are linked to the worsening economic conditions. These challenges include price volatility due to inflation, insufficient credit, and low customer volumes.

Rebecca and other CBTs struggle due to competition from men who are more established, supply-side shortages, price instability due to exchange rate volatility, income seasonality, insufficient credit, and inflation. They also face strict border restrictions, requests for bribes, and harassment by public officials at the border checkpoints.

The Kenyan Shilling has depreciated by 15% to the US dollar in the past six months. This is an example of exchange rate volatility, which makes it difficult for Rebecca and other CBTs to set suitable prices for their goods. Given their small size, CBTs cannot hold sufficient foreign currency to cushion themselves against exchange rate loss. CBTs rely on customs offices, informal money changers, and forex bureaus, which are unlikely to offer competitive rates due to the exchange of low amounts.

Savings behavior

Janet, Rebecca, and other traders heavily rely on informal savings mechanisms, such as chamas, to meet financing gaps. Chamas are informal savings groups where the members collectively pool their resources and rotate funds among the group. They must hold liquid assets, mostly cash and mobile money, to meet their personal and business needs. This discourages long-term savings or investments in other asset classes, such as fixed savings accounts, money market accounts, and treasury bills. This limits their growth potential.

Women OATs and CBTs face a high temptation to spend cash. So, they adopt various self-imposed measures to ensure financial discipline. They lock their savings with mobile money operators to prevent premature withdrawal, save via their chamas, and repay loans whenever they have extra cash.

Access to credit

Liquidity is a major challenge. Janet, Rebecca, and others access credit from formal and informal sources. Most prefer informal sources for their accessibility, convenience, and affordability.

For example, women OATs and CBTs borrow between USD 14-28 from friends and family. They repay these short-term advances on the same day at zero interest. Beyond friends and family, other sources of informal loans include women’s groups that charge interest rates of 10-15% per month (10% being the mode) and moneylenders who charge as much as 15-20% per week.

While women OATs rarely sell items on credit, some women CBTs extend credit to trusted customers. However, they face additional liquidity challenges when customers fail to repay on time.

Use of digital channels

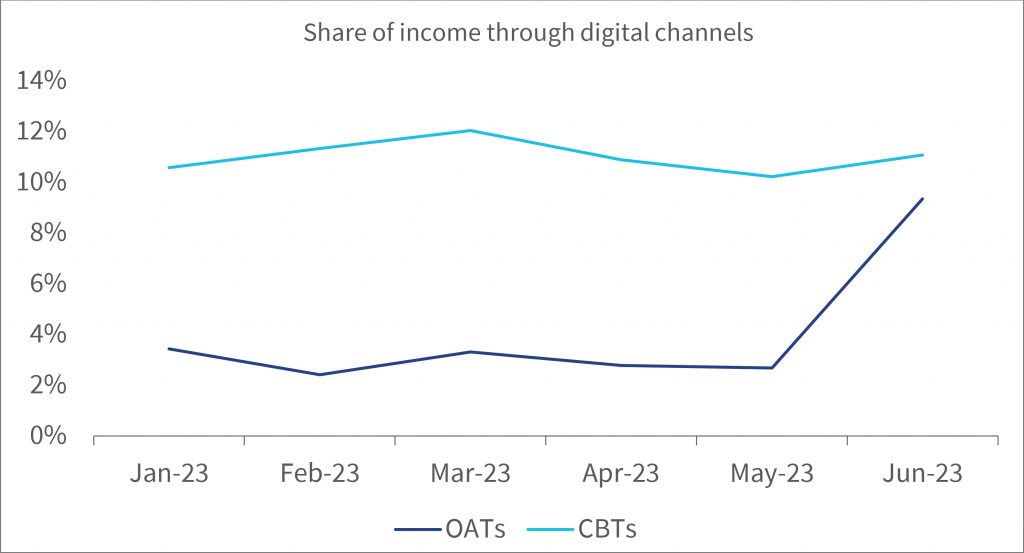

The use of digital channels has observed slow growth, driven mainly by mobile money. In the first six months of this year, Janet and other women OATs received payments for goods and services, primarily in cash. The income received via digital channels stood between 2%-9% (average 4%).

Between May and June 2023, the share of income from digital channels tripled from 3% to 9% for OATs. The growing trend in which financial service providers (mainly banks and mobile network operators) actively onboarded them onto merchant payment codes supported this growth. Alongside their simplicity, merchant payment codes offer speed, security, and convenience. This permits OATs more time to serve customers than they have to spend when they count money and refund change.

Women CBTs, such as Janet’s share of income through digital channels, are higher than that of women OATs—these range between 10% and 12% (average 11%). CBTs rely on digital channels for cross-border receipts and payments, mostly via mobile money.

Market segmentation

Women OATs and CBTs are not a homogenous group. We observed at least three personas that fall within the agile segment. They learn quickly, transact across multiple channels, have bank accounts, and earn more than USD 84 monthly. Following is a brief description of these three personas:

- Hustlers (28% of our diarists), such as Janet and Rebecca, earn USD 251 monthly net profit on average and are relatively new to business. They struggle to meet ends and need credit to balance their household and business finances. They use the credit mostly for consumption smoothing.

- Strivers (33% of our diarists) earn an average of USD 380 monthly net profit. They are experienced entrepreneurs. They borrow to grow their businesses and smooth personal consumption.

- Thrivers (39% of our diarists) earn an average of USD 669 monthly net profit. They are experienced entrepreneurs. Their businesses are stable, and they generate sufficient revenues to meet their personal and business goals. They borrow to expand their businesses.

Recommendations to financial service providers

Financial services providers struggle to develop cheaper, long-term credit to unlock productive credit for these entrepreneurs. Despite the challenges, they can still attract traders, such as Janet and Rebecca, if they:

- Design products that allow savings automation and entice customers toward goal-based savings (For example, through lock-in features and higher interest rates, among others);

- Offer affordable, accessible, and convenient credit alongside non-financial services, such as business advisory and financial literacy training;

- Build solutions that allow customers to track their finances and provide linkages to formal borrowing;

- Generate data trails based on repayment activity and empower borrowers to graduate from Hustlers to Thrivers;

- Build platforms that provide access to financial products, exchange rate information, and support timely settlement of cross-border transactions.

We cannot understate how critical informal traders, such as Janet, Rebecca, and others, are to drive Africa’s trade. However, financing their businesses at scale requires that providers offer viable financial solutions. These solutions should address liquidity challenges, encourage long-term savings, support customer graduation, and facilitate cross-border payments.

Leave comments