From launch to lift-off: Lessons from the Beninese market

by Melissa Rousset

by Melissa Rousset- Nov 1, 2016

- 6 min

by

by  Nov 1, 2016

Nov 1, 2016 6 min

6 minDFS providers in Benin entered the market quickly and focused primarily on scale—i.e. reaching high volumes of low-value transactions and therefore some fundamental building blocks were not cemented. This blog gives recommendations to the current providers in the market as well as for those who are considering (or planning) to launch their deployment so that they can experience high customer registration and usage

Click here to read the blog in French

Six years into the launch of digital finance in Benin, the market is expanding. The two main mobile network operators (MNOs), MTN and Moov, have paved the way by leveraging their large GSM customer base and airtime distribution channel to scale up quickly. They have capitalized on their positive brand image and reputation amongst customers to communicate about their digital financial services (DFS) use cases. In fact, over half of Beninese adults (54%) are aware of a mobile money provider. However, the relatively high levels of awareness have not translated into high customer registration and usage – only 9% of Beninese have a registered mobile money account (Intermedia, 2016).

The Helix Institute of Digital Finance recently conducted qualitative research in Benin in partnership with the UNCDF Mobile Money for the Poor (MM4P) programme. The study findings indicate that because DFS providers entered the market quickly and focused primarily on scale—i.e. reaching high volumes of low-value transactions – some fundamental building blocks have not been cemented. It would be judicious that Beninese providers take a step back and ensure that they have put in place a solid foundation to support their efforts to grow.

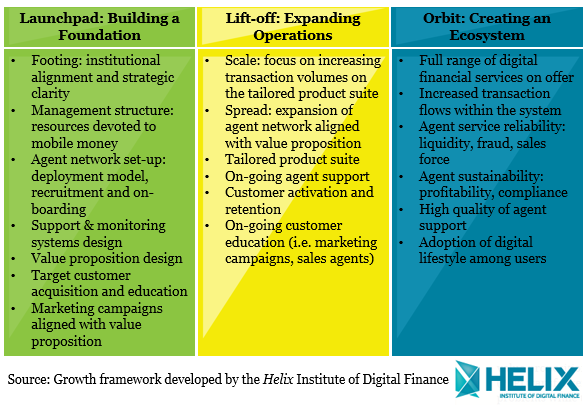

Defining the Three Stages of Success for DFS Deployment

There is no universal definition of what a ‘successful’ digital finance deployment is – for there are various players with different objectives who often offer diverse value propositions to different customer segments. However, there are some fundamentals that will ensure that providers can deliver optimally on their respective objectives and value propositions. Providers should ideally undergo three growth stages in order to reach their full potential (Figure 1).

The ‘Launchpad Stage’ is the developmental phase which concentrates on getting strategic foundations right, such as defining clear strategic objectives and management structure, before rolling out a DFS deployment. Once these tasks have been completed, the focus then shifts to expanding operations. The ‘Lift-off Stage’ involves increasing transaction volumes on the tailored product suite to target customers and expanding delivery touchpoints at strategically chosen places. Years into deployment, when the market reaches maturity, providers must concentrate on building a digital ecosystem. It is worth noting that no provider has reached the ‘Orbit Stage’ yet; even the most advanced East African markets are still struggling to overcome operational challenges.

Figure 1. The Three Growth Stages of DFS Deployment

The Beninese Market is Propelling towards Lift-Off

In Nigeria, Benin’s neighbour, providers seem to have skipped the ‘Launchpad Stage’, whereas in the Beninese market, providers have attempted to put most of its foundations in place. The two major providers have carefully thought through their value proposition to customers: domestic and cross-border person-to-person transfer (P2P) services, to address Beninese demand for safe, affordable and convenient payment solutions. By targeting key remittance corridors – particularly Ivory Coast and Togo, Beninese providers participate in boasting a pioneering cross-border remittance model in the West African Economic and Monetary Union (WAEMU).

To successfully deliver their value proposition to target customers, MTN and Moov have designed an extensive agent network spread across the country (over 8,300 active agents as of October 2016), creating customer touch points in both sending and receiving corridors. On the technology front, MNOs have an advantage because they control the network bandwidth; thus both providers have managed to maintain service downtime at low levels. MTN has recently upgraded its technological platform, demonstrating its commitment to delivering reliable service to customers and build their trust and usage of DFS services.

Despite these achievements in a relatively nascent market, our research demonstrates that there are some gaps in Beninese providers’ strategies that may hurt them in the near future if action isn’t taken now. We recommend the following for current providers in the market as well as for those who are considering (or planning) to launch their deployment:

1. Position Mobile Money as a Priority

For new players, one of the major challenges is to define clear objectives regarding DFS and build consensus around them. Various departments within a company may want to pursue conflicting objectives – from envisioning DFS as an additional source of revenue to support the existing business to positioning DFS as a core business for the company’s future.

Across multiple markets, MNOs often experience a disconnect between their traditional voice business and mobile money business, which can result in barriers to building the latter. As for financial institutions, the digitization of their operations often means changing their traditional paradigm and laying off the middlemen – cashiers, back-office staff – which can lead to resistance towards adopting the DFS business case.

Providers must ensure that they obtain the commitment to pursue the target DFS objectives from all of their stakeholders across various streams of the organisation, from executive management to operations’ staff, right from the beginning. Rushing to launch a DFS offering without strategic clarity and an organisation-wide commitment can result in slow progress and may eventually set up a deployment for failure. Therefore, Beninese providers will want to ensure that all departments are on board and embrace their objectives for DFS.

2. Understand Your Target Customer’s Preferences

Although Beninese providers’ offerings are designed to be self-initiated transactions over a handset, research indicates that agents play a critical role in assisting customers to conduct transactions. Agents do this by either helping customers perform the given transaction on customers’ phones or using agents’ own devices.

This is not surprising in a market characterized by low readiness for DFS – only a third of Beninese are literate and 44% have had SMS exposure (Intermedia, 2016). Interviews with Beninese agents indicate that they understand the need for human interaction in a nascent DFS market, and many have created trust relationships with their customers by walking them through what is, for many customers, their first digital experience.

In light of this, providers may need to evaluate the transaction methodology in which they are offering their value proposition, as well as their marketing strategies to adjust to those customers not yet comfortable with using mobile wallets. A first step is to conduct market research to understand what product and accompanying user interface will drive the uptake of services, and augment its reach by providing consumer education. Agents are often the first touch points for most end-users, so providers may want to focus on promoting agents as their brand ambassadors, simultaneously equipping and incentivizing them to play this role.

3. Focus on Agent Network Quality Rather than Quantity

While quickly onboarding agents across Benin has ensured ubiquity of the service, providers may not have necessarily ensured whether their agents have the right profile to sell the service, and are sufficiently trained or monitored to deliver top-notch customer experience. Our research shows that some agents start the business with just a table and a parasol, with as little as 20,000 FCFA (34 USD) – resulting in high volumes of denied transactions – and with limited knowledge of operational aspects of their own DFS business.

Quite interestingly, Beninese providers report that their branded shops (MTN and Moov shops) account for a majority of the conducted transactions as opposed to their retail agents, whom providers still invest in. This actually indicates that end-users choose to transact where they are assured of finding liquid and secure outlets – leaving the vast majority of retail outlets with low traffic, and thus low profitability. This may hurt providers in the long-run, as customers who have a negative experience at an outlet are unlikely to try and use the service again. Therefore, they should focus on designing and implementing a structured approach to agent selection, striving for quality over quantity, and ensure that the agent profile is best-fit with the provider’s value proposition.

Recommendations for New Players

The Beninese digital space is growing and different players are on the horizon: ASMAB is the first microfinance institution in the entire WAEMU to have received its Electronic Money Establishment license in 2013. The Helix Institute will be keenly observing Benin’s developments, and we hope that the challenges we have highlighted will encourage new and old players to think about their strategic considerations in the market. Though the challenges may not be similar for financial institutions, which have different competitive advantages than MNOs, the rule of thumb is to devote sufficient time and effort to build a solid strategic foundation right in the beginning during the ‘Launchpad Stage’ before propelling into the ‘Lift-Off’ stage.

Leave comments