FinTech start-ups in Côte d’Ivoire amid COVID-19: Expectations from the government and the regulator

by Ariane Kouassi and Achille Tefong

by Ariane Kouassi and Achille Tefong- Jul 9, 2020

- 5 min

by

by  Jul 9, 2020

Jul 9, 2020 5 min

5 minThe blog gives a unique glimpse of the FinTech ecosystem of Côte d’Ivoire, how it has been impacted by the COVID-19 pandemic and what measures and guidelines are being proposed and implemented by the government and regulators of the country.

“We are currently seeing a net increase of approximately 30% in the number of subscribers, with a mass reactivation of dormant accounts on our platform. If this trend continues, it could lead us to strengthen the customer support team, even if this does not guarantee that we will have a better turnover. We will wait [and] see,” – Founder of an Ivorian chatbot-powered payment platform.

This blog examines the impact of the COVID-19 pandemic on FinTechs, their expectations from policymakers and regulators, and the measures proposed by these critical players in the FinTech ecosystem.

FinTech start-ups in Côte d’Ivoire before the pandemic

The FinTech industry in Côte d’Ivoire faced stiff challenges even before the pandemic arrived in March, 2020. These challenges included:

- An unclear regulatory framework that discouraged FinTechs to move beyond providing credit services into other activities that could accelerate financial inclusion;

- High cost of licenses to practice as a FinTech company;

- Heavy taxes that pushed the operational expenditures of start-ups below sustainable levels.

Impact of COVID-19 on FinTechs

With the arrival of the COVID-19 pandemic FinTechs now face the following challenges:

- Organizational challenges: While the larger FinTechs are optimistic and continue to retain their pre-pandemic workforce in numbers, the smaller FinTechs, especially start-ups, have been forced to lay-off part of their staff and freeze recruitments. Some have even had to enforce pay-cuts for existing employees, including upper management.

- Internal process challenges: To safeguard their teams and abide by the government’s measures for social distancing, the FinTechs are adapting their processes and tools to enable employees to work from home.

- Customer engagement: This reorganization of processes has also led to greater use of digital means, especially social media, for activities such as generating leads and onboarding new customers.

“We think this prospecting method suits us best, given that we have limited means. In the future, travel for our team will be restricted to essential travel alone.” – A FinTech CEO

- Product changes: Most FinTechs are transforming the physical features of their products into intuitive digital features for a seamless transition to customer engagement in a more digital world.

The lesser-known and comparatively younger FinTechs do not enjoy the high levels of popularity of the established FinTech giants of mobile telephony, such as Orange Money, MTN Mobile Finance Services, and Moov Money. Yet these smaller companies are depending on their speed, agility, and flexibility to devise and implement innovative solutions to overcome the challenges posed by the COVID-19 pandemic.

The Government of Côte d’Ivoire had set up a support fund of XOF 100 billion (approximately USD 1,700,000) for small and medium enterprises (SMEs). While the small FinTechs hope to benefit from this fund, they also seek investment from professional investors to survive and sustain their businesses. This is also driven by the fact that certain measures taken by the regulator – the central bank, BCEAO have a direct impact on the turnover of these FinTechs and that many of these companies do not often maintain cash reserves of more than 3-4 months. In 2019, the World Bank and BCEAO laid the groundwork for a review of the FinTech start-up sector by organizing a conference. While the regulator announced the emergency measures to tackle the pandemic, the results of this laudable World Bank-BCEAO initiative are yet to bear fruit.

FinTech start-ups in Côte d’Ivoire: All eyes on the government

FinTech start-ups in Côte d’Ivoire expect two types of support and guidelines from the government: those linked directly to the COVID-19 crisis and those linked more broadly to the “business-as-usual” industry activity.

The Ivoirian State announced measures related to the COVID-19 crisis at the Council of Ministers held on 15th April 2020. In the following section, we look at issues related to these measures in the context of the pandemic:

- Clear, precise procedure on how to avail the support fund worth 100 billion XOF (USD 1.7M) for SMEs: The FinTech start-ups we interviewed stated that they were unclear about the criteria, stages, and timelines for obtaining SME support funds for SMEs that were announced in April.

“You know me. I am not into political affairs, so we do not believe [in this announcement]. We have registered through the online system but have no visibility on what the process is or when and how the funds will be made available.” – An Ivorian FinTech founder.

- Inclusion of Ivorian FinTech start-ups in social assistance programs: Social cash transfer programs for poor households ignore the services that FinTech start-ups could provide with lower turnaround times and lower costs than larger FinTechs would. If the government includes such start-ups to implement these programs, then it will increase the visibility of the start-ups involved. It will also help the financial institution partners to improve their business efficiency along with their payments and collection methods.

“We do not necessarily expect money from the government but at least [it could] include us as local FinTech in programs like these.” – A FinTech founder

- Tax relief: Several of our interviewees raised the issue of going further than the postponement of tax payments. According to them, the outright cancellation of taxes and fiscal charges for the period of confinement would be of greater benefit to them.

“Yes, there was a deferral but this remains a debt—and short-term debt at that.” – A FinTech founder.

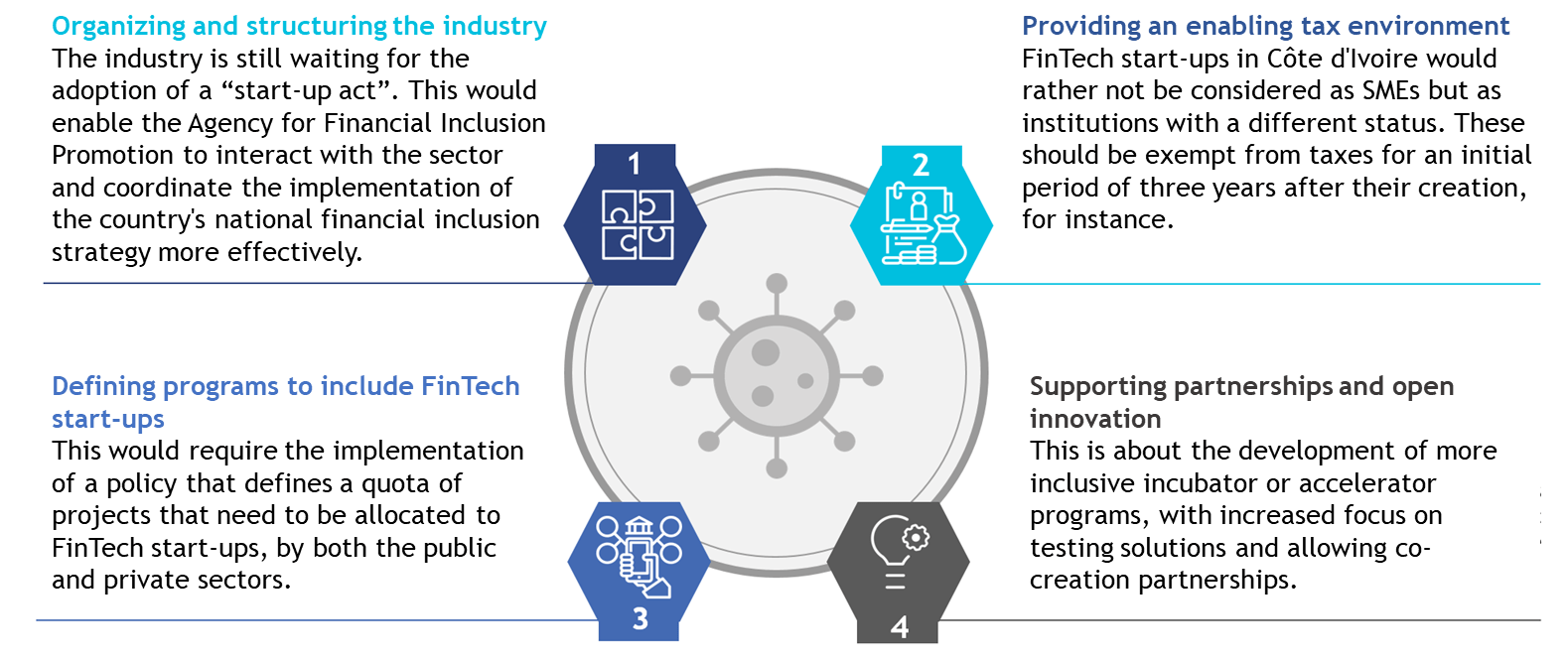

More broadly, based on discussions with sector players, expectations linked to the normal activity of the Ivorian FinTech start-up refer to:

Figure 1: What FinTech start-ups expect from the Côte d’Ivoire government

Figure 1: What FinTech start-ups expect from the Côte d’Ivoire government

FinTech start-ups in Côte d’Ivoire: All eyes on the regulator

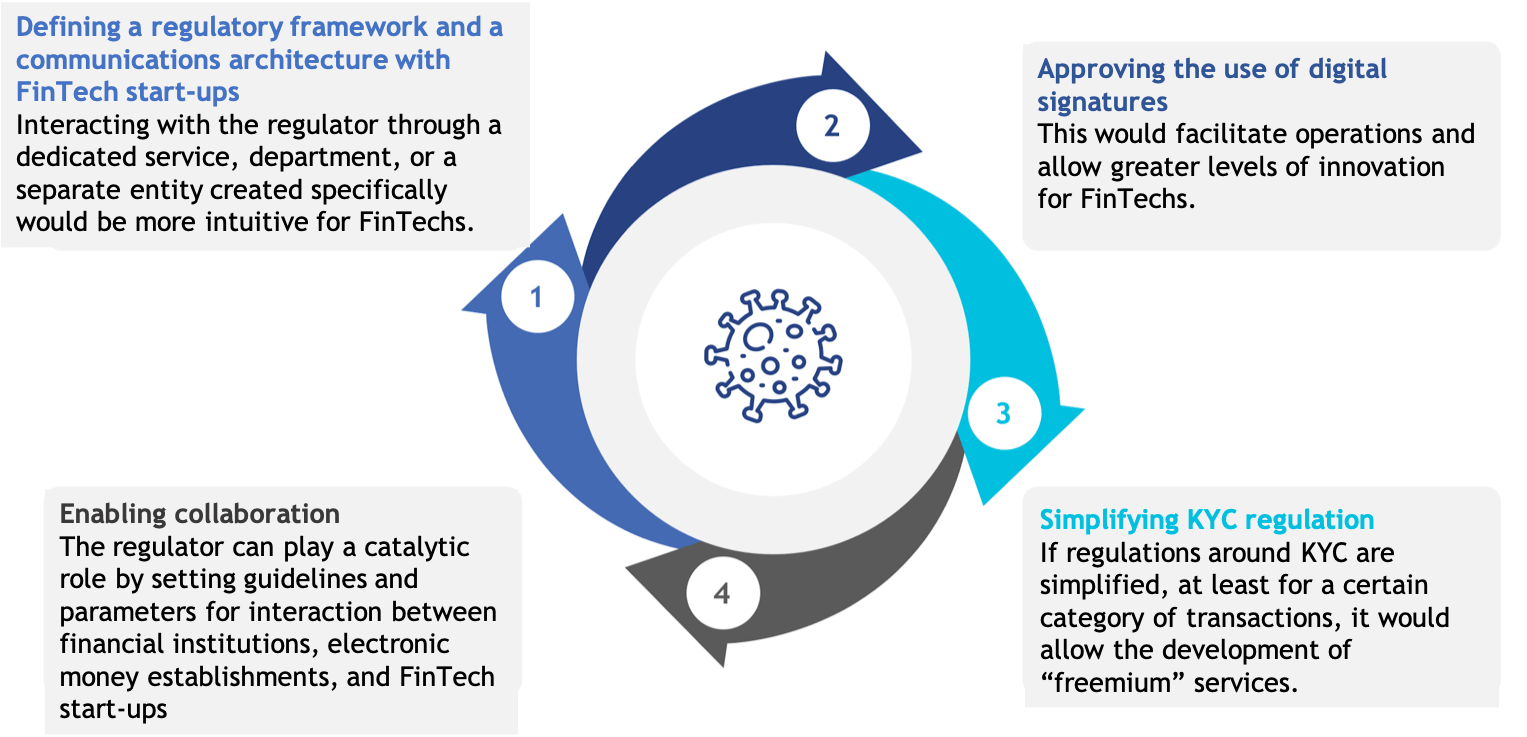

Apart from the government, the regional regulator also has a key role to play. The BCEAO has taken several measures during the crisis, including the waiver of commercial commissions on digital payments and the relaxation of conditions to open mobile wallet accounts. However, a set of other expectations of the regulator, which MSC has highlighted in its forthcoming study on the mapping of FinTechs in Francophone Africa, are essential to the expansion of the Ivorian FinTech start-up sector. These expectations include:

Figure 2: What FinTech start-ups expect from the regulator

Figure 2: What FinTech start-ups expect from the regulator

Organizing the FinTech start-up industry: An imperative

Supporting the FinTech startup industry will help the Government of Côte d’Ivoire achieve at least two of its set objectives:

- to include 60% of the country’s population in the realm of financial inclusion by 2024, from the current levels of 40%;

- to promote social inclusion by reducing the unemployment rate, which is currently estimated at 26% of the population.

There is a need to re-organize and strengthen the FinTech start-up industry. Digital platforms such as the Hub of Digital Finance will play a pivotal role in achieving this. Such platforms will bring together various actors of the entrepreneurial ecosystem not only from Côte d’Ivoire, but also from the entire Francophone Africa region, to facilitate the development and expansion of the industry beyond the borders of the continent.

The French version of this blog is available here.

Leave comments