Face-to-face network specialists: Helping institutions better bring digital finance to the unreached Part 1

by Chris Wolff, Prabir Barooah and Graham Wright

by Chris Wolff, Prabir Barooah and Graham Wright Feb 5, 2019

Feb 5, 2019 6 min

6 min

This blog series outlines potential next steps towards an augmented future, which visionaries in the industry could explore through the support of Agent Network Management Companies (ANMC).

Last year was filled with a refreshed interest in agents, and starting 2019 with a look ahead to their future can inspire a vision for how to build them into an industry that advances financial inclusion while boosting businesses targeting the base of the pyramid (BoP). At the World Bank Spring 2018 meetings, H.M. Queen Maxima of Netherlands and the then President of the World Bank, Jim Yong Kim emphasized the importance of mobile money agents. Queen Maxima noted how a business case needs to work for every player in the value chain to deliver services, including agents. Dr. Kim observed that only trusted agents can provide augmented services to include oral-only, illiterate, or innumerate customers.

For those eager for a faster path toward diversified digital financial services that meet the practical needs of the unbanked, it is time we start looking at networks of agents as the center of solutions that can “unstick” the status quo, as highlighted in The Clear Blue Water on the Other Side of the Digital Divide.

The initial steps towards agent-driven approaches are documented in a number of works. They include the FIBR/MasterCard paper Digital Solutions for Analog Agents: New Technologies to Manage Agent Networks, CGAP’s Employee and Agent Empowerment Toolkit and Ideabook, which detail how to “strengthen the engagement and the ability to deliver valuable customer experience,” and GSMA/MSC’s Distribution 2.0: The future of mobile money agent distribution networks, which highlights exemplary practices for any provider.

This blog series outlines potential next steps towards an augmented future, which visionaries in the industry could explore through the support of Agent Network Management Companies (ANMC).

The posts will focus the case on:

- The need to disrupt the conventional approaches or actors to speed up the progress;

- The unique positioning and potential advantages that make ANMCs deserving of support;

- Six ideas worthy of experimentation;

- How different institutions could use ANMCs to complement their current operations.

In the short run, mobile money service providers should differentiate between sales and transactional agents. The differentiation between sales and transactional agents involves:

- Relatively sophisticated sales agents who are usually dedicated and are exclusive to one brand. These agents are responsible for selling products, onboarding customers, and conducting transactions of larger value;

- Basic transactional agents, who are usually non-dedicated and non-exclusive. These agents are responsible for conducting typically smaller cash-in and cash-out (CICO) transactions.

Improving on the status quo

The 2017 Global Findex report revealed much to celebrate for financial inclusion, and undeniable strides towards the provision of DFS, indicating a promising future. Those of us with a passion for the power of DFS to deliver real value to the poor want to see the future sooner—and without the growing digital divide that we currently see emerging. We can surely improve on the current 24% (30-day active) usage rates, offer a broader array of products, and find creative ways to overcome gender disparities.

While each country’s digital journey is different, there are some common denominators that can stifle the primary drivers of the efforts of both telcos and banks to serve the mass market through digital platforms.

If we are ever going to offer more sophisticated digital financial products, we will need to respect the need for trust and the role of face-to-face interaction to build that trust, particularly in oral and rural communities. In order to achieve this, we will need to develop and deploy models that can increase the value-add by agents rather than minimize them and continue to see agents as a regrettable cost.

Dr. Kim highlights that agents are required to provide a range of services upon which all of mobile money depends. Yet liquidity management, marketing, customer service, complaint management, and agent assistance with transactions are rarely, if ever, factored into their formal compensation. Agent commissions should be seen as part of mobile money’s “cost of goods sold”, plus sales incentives. Agents are fundamental to any mobile money service rather than merely a channel cost to be squeezed out of existence. Despite smartphone sales growth (accompanied by data or not), in most countries, low-income customers will want and often need a trusted person to explain the nuances of aspired-to, sophisticated products, to promote the benefits, and to provide the after-sales service.

Dr. Kim highlights that agents are required to provide a range of services upon which all of mobile money depends. Yet liquidity management, marketing, customer service, complaint management, and agent assistance with transactions are rarely, if ever, factored into their formal compensation. Agent commissions should be seen as part of mobile money’s “cost of goods sold”, plus sales incentives. Agents are fundamental to any mobile money service rather than merely a channel cost to be squeezed out of existence. Despite smartphone sales growth (accompanied by data or not), in most countries, low-income customers will want and often need a trusted person to explain the nuances of aspired-to, sophisticated products, to promote the benefits, and to provide the after-sales service.

To reach the mass market, telcos and banks, with their greater power, customer base, and balance sheets were the obvious first choices to back. However, the same scale can also create hurdles for reaching the low-income market with products that are tailored to meet their needs. These challenges include legacy systems, competing priorities, product-focus over customer segmentation, and more alluring, affluent markets.

ANMCs are specialists in developing face-to-face, commission-based networks on behalf of brands through a focus on recruiting, training, equipping, and quality control or performance management. In contrast to telcos or banks, tackling change through ANMCs offers the following advantages:

A. A sole focus on agents and no need to compete with numerous internal alternatives that face larger corporations puts them in a better position to optimize agent performance. Boosting the value-add of frontline sales and basic transaction agents is a different business from the retail work of banks or MNOs. So it would help to have specialists build out this human resource-based business. To date, ANMCs have been sidelined in relation to other financial inclusion influencers, but it could, and indeed should play a bigger role.

B. The smaller size of ANMCs means that they have less entrenched business practices, which could make it easier to gain and hold their attention on creative approaches to optimizing their agent networks for both profitability and social impact (or value addition).

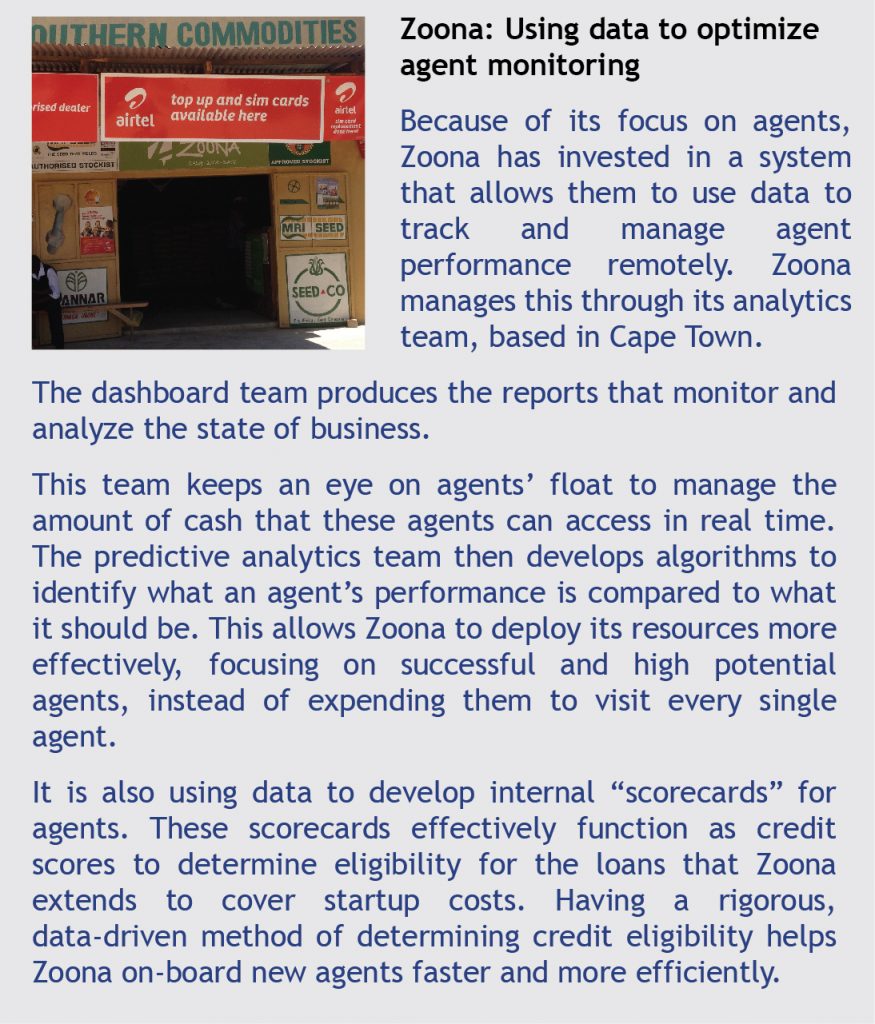

C. ANMCs are not weighed down by legacy systems. These make it harder for established industries to find new ways to track and boost agent performance or even report internally on agents’ sales volumes or customer satisfaction for more refined segmentation. So ANMCs could pioneer data-driven decision making, as shown in the example of Zoona.

It is our belief that proponents of financial inclusion need to also foster ANMCs with the same philanthropic or social-technical support that banks or telcos have received. Some options are highlighted in the next post.

It is our belief that proponents of financial inclusion need to also foster ANMCs with the same philanthropic or social-technical support that banks or telcos have received. Some options are highlighted in the next post.

Although some have been initially instrumental in the rapid build-up of networks (as Top Image did for M-PESA), ANMCs have not proliferated or realized their full potential, since telcos and banks typically persist with in-house agent management. Telcos and banks have so far seen opportunities to secure competitive advantage through owning and managing their agent networks. This will be eroded as markets move towards shared agents and agent-level interoperability. Thereafter telcos, if not banks, will likely begin to think more carefully about the potential economies of shared and third-party managed agent networks governed by key performance indicators. While telco agents have so far been raised up to offer predominantly a transactional, basic CICO service, bank agents have shown that you can start operations with sales agents, who offer a range of relatively complex financial services.

As markets shift and some telcos find themselves selling off assets, starving their mobile money investments, consolidating, or facing non-exclusivity of agents, they may seek stronger ANMCs. These third-party service providers could alleviate distractions from the core business and reduce the costs of running agent networks by offering shared services. Here we propose six paths that warrant experimentation in order to build an industry of ANMCs that are positioned to advance financial inclusion and profits for all.

![]()

To foster new, stronger, diversified, or shared agent networks, proponents of financial inclusion could support an “incubator” for:

- ANMCs by catalyzing startups or bolstering smaller players;

- Last-mile sales networks to augment their offerings as providers of a range of digital services;

- DFS products by incorporating R&D specialists within the daily operations of an owned network;

- Joint ventures through brokers that form and run shared agent networks;

- ANMC associations to tackle shared problems and proliferate the increased value-add brought by their industry;

- Franchise services company that spreads expertise and investments for ANMC owners to not have to learn the best practices on their own.

We will discuss these six approaches in our next blog.

Written by

Chris Wolff

Warning: Undefined array key "title" in /var/www/html/wp-content/themes/microsave/single.php on line 486

Warning: Trying to access array offset on value of type null in /var/www/html/wp-content/themes/microsave/single.php on line 486

Prabir Barooah

Specialist/Consultant

Leave comments