Can Farmer Producer Companies (FPCs) benefit from participating in agriculture derivatives trading?

by Mukesh Kumar, Rajnish Kumar and TVS Ravi Kumar

by Mukesh Kumar, Rajnish Kumar and TVS Ravi Kumar- Apr 14, 2023

- 6 min

by

by  Apr 14, 2023

Apr 14, 2023 6 min

6 minIndia’s policymakers view the trading of commodity derivatives skeptically. As a result, they have enacted occasional bans and suspensions. Unfortunately, this apprehension is often misplaced and appears to be driven by concerns of speculative trading and market price manipulation. However, farmer producer companies have increasingly traded commodity derivatives to establish market linkage, achieve better price realization, and hedge commodity price fluctuations.

In May 2022, as market trends indicated rising prices for maize, Aranyak Agri-Women Farmer’s Producer Company Limited (AAPCL) used the National Commodities and Derivatives Exchange (NCDEX) futures market to make an additional $1,875 (INR 150,000) profit on their sale of maize.

Policymakers in India view the trading of commodity derivatives sceptically, and as a result, have enacted occasional bans and suspensions. Unfortunately, this apprehension is often misplaced and appears to be driven by concerns around speculative trading and market price manipulation. However, there is a growing trend among farmer-producer companies to utilize commodity derivatives trading to establish market linkage, achieve better price realization, and/or hedge commodity price fluctuations. In fact, over the last five financial years (FY 2016 to present), NCDEX has successfully onboarded 470 FPCs, with 160 of them trading a total of 115,175 metric tons (MT) in 18 different commodities.

The NCDEX and Multi-commodity Exchange (MCX) are the two major derivative exchanges in India, including futures and options contracts. Futures contracts allow buyers to purchase a commodity at a pre-determined price at a specific point in the future, while options contracts give the owner the right to sell (put option) or buy (call option) the underlying commodity/asset at a pre-decided price. One major difference between futures and options contracts is that the buyer or seller is obligated to buy or sell the good at the predetermined price upon contract expiration, whereas options holders have the right, but not the obligation, to buy or sell. In India, FPCs are allowed to deal in both futures and options. MSC through our work with FPCs, has facilitated 2,100 MT of maize futures trades and 1,200 MT of options trades in maize, chickpea, and mustard seeds. In this blog, we highlight our experience in supporting FPCs, trade in the derivatives markets, as well as the opportunities and challenges they have encountered as a result. For the purpose of this blog, we are only concerned with delivery-based trades, which is derivatives trading accompanied by the physical transfer of commodities upon contract expiration, and not speculative trades.

How FPCs can benefit from derivatives trading?

Derivatives markets as a way of institutional market linkages for FPCs

FPCs can benefit from futures contracts in several ways, one of which is by leveraging arbitrage opportunities between the spot market price which is the current market prices, and future prices reflected on commodity exchanges. Commodity exchanges have the potential to attract a larger set of buyers than traditional spot markets, due to the sheer size and volume of what is being traded, providing opportunities for FPCs to obtain some arbitrage opportunities than they would get in the open markets.

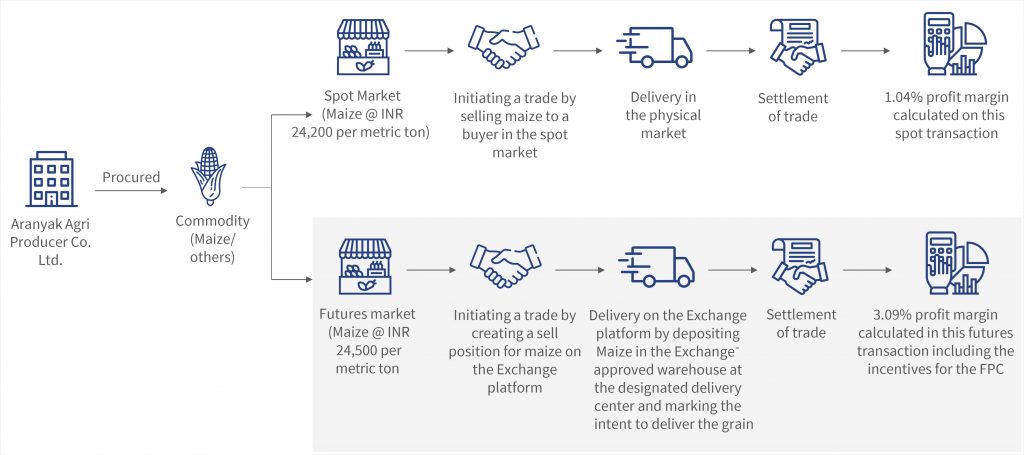

For an example, let us return to the case of Aranyak Agri-Women Farmer’s Producer Company Limited (AAPCL), which operates in Purnea, Bihar, and works with maize farmers. During the maize season from May to June, the FPC had the opportunity to trade maize August futures on the NCDEX exchange at USD 306.25 /MT (INR 24,500/MT), while the prevailing spot market rate was only USD 302.5 /MT (INR 24,200/MT). In essence, market forces indicated that the price for maize was going to rise, resulting in a price in the futures that was higher than the current metric ton price. By trading on NCDEX, the FPC was able to obtain a gross margin of 3.09% on the transaction, compared to the 1.04% margin it would have received if it sold in the spot market. There are additional expenses incurred by the FPC to deliver on the platform such as transportation costs till the NCDEX delivery centre and assaying costs at the NCDEX accredited warehouse. However, AAPCL benefitted from the subsidies offered by the regulator Securities and Exchange Board of India (SEBI) and NCDEX to FPCs to encourage their participation in derivatives trading.

Figure 1: Delivery based trade of AAPCL using futures contract

Price risk management using futures contracts

FPCs can effectively manage the price risk of stored commodities by using futures contracts without participating in deliveries on the commodities exchange platform. This approach can be particularly useful as explained in the following scenarios:

- When the exchange’s delivery center for a particular commodity is unavailable in the FPC’s intervention area. For example, NCDEX has a delivery centre for only maize in the entire state of Bihar. So, for other commodities FPCs may have to send the produce to other states.

- When the cost of delivery-based trades on the exchange is higher than selling in the nearest physical market.

- When storing commodities at the exchange’s warehouse is not logistically feasible or too expensive.

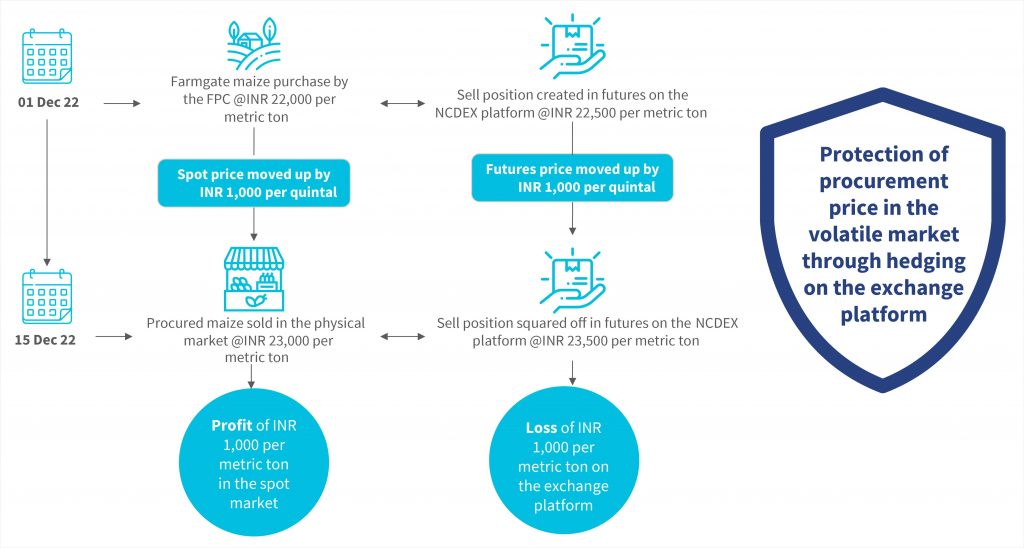

To illustrate the hedging mechanism, using a hypothetical company, ABC, consider the following example. On December 1, 2022, FPC ABC purchases maize from its shareholders at USD 275/MT (INR 22,000/MT). To hedge against potential losses, the FPC enters into a futures contract to sell maize on the NCDEX at USD 281.75/MT (INR 22,500/MT). On 15-Dec-22, the spot market price for maize became USD 287.75 /MT (23,000 /MT) and the “buy” rates in the futures market also moved up to USD 293.75 /MT (INR 23,500 /MT). The FPC sells the procured maize at USD 281.75/MT (INR 23,000/MT) in the nearest physical market, resulting in a profit of USD 12.5/MT (INR 1,000/MT). Simultaneously, the FPC closes out its sell position by buying a futures contract at USD 293.75/MT (INR 23,500), incurring a loss of USD 12.5/MT (INR 1,000/MT). In this example, the FPC does not realize a net gain or loss on these transactions but effectively protects the initial purchase price of USD 275/MT (INR 22,000/MT) from potential market price losses.

Figure 2: Price risk management using futures contracts

Price hedging through Put Options contracts

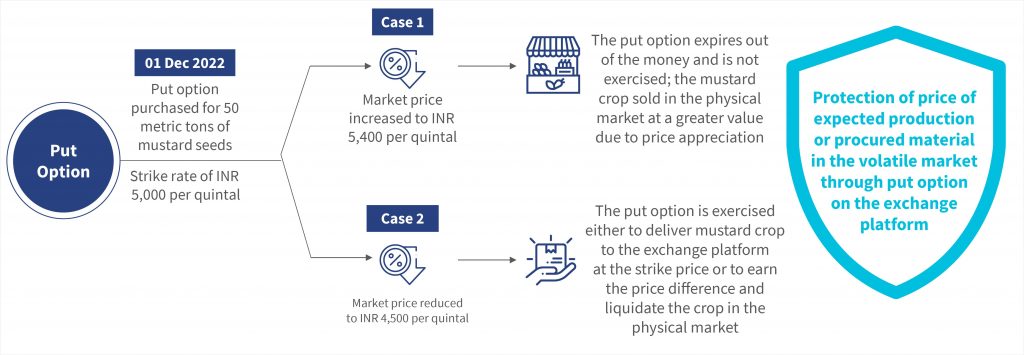

As previously mentioned, a put option, giving the holder the right to sell a good at a specified price by/on a specified date also serves as a valuable tool for hedging against price risks. For example, FPC ABC dealt in mustard seeds during the production season and purchased Put options on the 1st of December for 50 MT at a strike price of USD 62.5 /MT (INR 5,000/MT) via the NCDEX platform. This strike price represents the price at which FPC ABC can sell its mustard seeds if it chooses to exercise its put option. This put option was set to expire on January 25th. At the end of the season, the price of mustard seeds had risen to USD 67.5 /MT (INR 5,400/MT), allowing the FPC to sell the commodity in the spot market and earn a profit, while also squaring off the outstanding Put option at no additional cost. Alternatively, if the price of mustard seeds had fallen below USD 62.5/ MT (INR 5,000/MT), the FPC could have executed the trade on the NCDEX platform and made a profit. By following this process, the FPC was able to lock in a price for the commodity prior to the harvest season. The cost to purchase the Put option, also known as the premium, was around 6% of the total trade value, the FPC was able to take advantage of a 100% subsidy on the premium amount provided by SEBI to encourage Options trading by FPCs.

Figure 3: Price risk management using Options contracts

Other benefits of trading through exchanges

Exchanges are organised and supervised market places and trading through them offer a number of benefits to FPCs such as:

Reduced counterparty risk: Derivatives trading is supervised by the commodities exchange, which ensures that all parties involved in the trade meet their obligations. FPCs do not have to worry about receiving payment and buyers do not have to worry about the quality of materials supplied. These issues are common in spot market trades.

Price discovery and transparency: Derivatives markets are a good source of price discovery of agricultural commodities. FPCs can get a trend of the prices that the market is headed towards and can plan accordingly. Prices in the derivatives markets are clearly laid out, and FPCs do not face the ambiguity that they often encounter when dealing with traders and some institutional buyers.

Our next blog in the series considers the five key challenges that prevent greater adoption of derivatives trading by FPCs.

Leave comments