Can digital approaches enable better access to formal financial services to MSMEs?

by Aparna Shukla, Anup Singh and Graham Wright

by Aparna Shukla, Anup Singh and Graham Wright Apr 22, 2021

Apr 22, 2021 7 min

7 min

Financial institutions have a clear opportunity to enhance access to formal financial services for MSMEs. Let us examine from this blog whether digital approaches can give the needed access to MSMEs.

Experts estimate that the digital credit industry worldwide will be worth more than USD 890 billion by 2024. Users of digital credit around the world appreciate its convenience and immediacy. While digital credit has catalyzed access to finance for the mass market, it has barely begun to meet the needs of MSMEs.

The demand for affordable, relevant, and quality financial services for MSMEs has grown over the past few decades. In 2010, McKinsey estimated that the total unmet need for credit by all formal and informal MSMEs in emerging markets was worth USD 2 trillion. However, a recent study by CGAP estimates that the unmet need for credit among micro and small enterprises (MSEs) in emerging markets is around USD 4.9 trillion. Several factors constrain access to credit for MSMEs. These include the high cost of accessing credit, limited awareness, lack of credit history, and short repayment periods.

The COVID-19 pandemic has further reduced the supply of formal financial services to MSMEs, which currently face a squeeze on credit, have limited access to capital, and face stifled growth. The process of their recovery from the debilitating effects of the pandemic will call for enhanced access to suitable financial services. As per our research, almost one-fifth of entrepreneurs gradually began using digital platforms to sell their products during the pandemic. As the entrepreneurs build their digital footprint and profile, financial service providers have an opportunity to use digital information to assess creditworthiness and offer digital credit facilities.

The chance to use digital approaches to enhance access to finance for the entrepreneurs

Financial institutions have a clear opportunity to enhance access to formal financial services to MSMEs by:

Supporting MSMEs to build digital footprint:

Financial service providers can increase access to finance for entrepreneurs by understanding their footprints better—whether they are digital or potentially digital. As the providers build the footprints of entrepreneurs, it is crucial to assess their readiness and receptivity to transition to a digital future and segment the entrepreneurs accordingly. For example, at MSC, we have learned that providers cannot promote merchant payments through standard “cookie-cutter” solutions. Therefore, we need to look at merchants as distinct personas to decipher their characteristics and explore ways to change their behavior. Our research identified that merchants embody one of four key personas: go-getters, receptive reticent, high-hanging fruits, and easy-catch merchants.

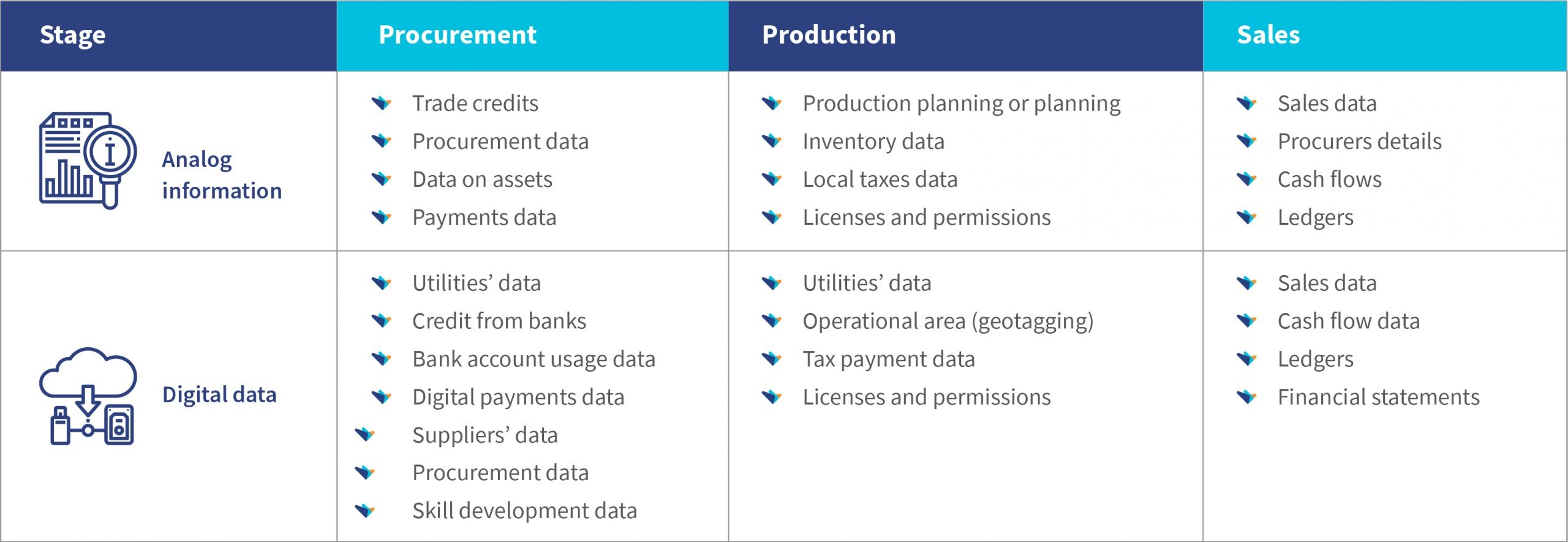

Notably, while MSMEs have some digital presence, most transactions remain in silos. The entrepreneurs themselves are not aware of the data trails they generate and remain in the dark about potential use-cases for data, now or in the future. Moreover, financial institutions cannot utilize the data trails fully to increase financial access. A snapshot of data trails generated by an entrepreneur below illustrates what data could financial institutions digitize to enable better credit assessment.

Lenders and financial institutions can build a nuanced understanding of the status of the digital data footprint of entrepreneurs across different segments and activities. Assessing the digital footprints may include answering questions, such as:

- What are the digital data streams? Who owns them?

- What is the availability of data? Is it aggregated or disaggregated? Is it analog or digital?

- What is the depth and quality of the existing digital data footprints?

- How can data be aggregated and ownership restored with the entrepreneur?

- Does the entrepreneur have control over the data to open it to financial institutions and inform credit decisions?

- How can the entrepreneur use data for better services and services at a better price point?

- In light of regulations on data privacy, how does a financial institution ensure security and ethical use around ownership, usage, handling, storage, and data transfer?

Once the financial institutions have helped MSMEs enhance their digital footprints, they may use the digital data to develop new business models, innovate risk management approaches, and formulate and implement new products anchored on alternate data.

Building skills and capacities of MSMEs on business management

As discussed in our previous blog, “Digitizing the operations of MSMEs: A big step to strengthen their resilience”, we argue that financial institutions may support enterprises to trust, navigate, and use technology to market their products and services, receive payments, and access digital financial services. Carefully designed and delivered digital skilling programs based on an understanding of their mental models can enable MSMEs to use digital technology to grow their businesses.

Digitizing enterprise finance operations

In our blog, “How can financial institutions use digital transformation to help MSMEs recover from the impact of the COVID-19 pandemic?” we argue that financial institutions may have to use a multi-pronged approach anchored on digitization to support MSMEs as the entrepreneurs revive businesses and build resilience through several avenues. These ways include:

- Developing a digital business model and digital solutions for MSMEs;

- Digitizing front-end and back-end processes;

- Using an omnichannel approach and embed digital channels to distribute financial services to enterprises;

- Providing superlative user experience using a digital engagement approach.

Developing and implementing adequate digital products for MSMEs

Financial service providers, including FinTechs, have the opportunity to design and implement customized and relevant digital products for MSMEs. Such products may include:

· Short-term loans with a tenure of a day to a week to help market traders who currently use loans repayable over weeks or a month to finance their business cycles, which run from early morning to afternoon. Mahindra Finance, a non-bank finance company from India has plans to launch digitally-driven small-ticket loans in 2021.

· Goal-based savings and loans offer a new approach to wealth management that helps an individual plan for a specific life-cycle goal. Such products have an appropriate financial planning tool embedded in the app or USSD interface. Many financial institutions offer goal-based products to their customers. ALAT, Nigeria is Africa’s first fully digital bank launched by Wema Bank. It provides simple, automated saving plans that are goal-based and earns an annual interest of 10%—triple the typical bank rate. Similarly, Equity Bank offers EazzySave to helps customers save toward a goal and often backs it up with a loan.

- Digital credit for enterprises: Digital credit provides instant, automated, and remote credit to users. Millions of users have benefited from digital credit to meet their consumption needs. While some enterprises use digital credit for their sundry needs, digital credit is seen as a last resort to meet larger working capital needs. Digital credit providers may develop MSME-specific products to on alternate data sources, customized credit-scoring approaches, and aggregating existing and potential digital footprints. We see this in action as in the case of U GRO Capital, a small-business lending platform from India. The platform plans to roll out an end-to-end digital lending platform for the sector and plans to reach out to 500,000 MSME clients.

- A merchant cash advance (MCA) is a point-of-sale (POS)-based loan product for entrepreneurs offered for a fixed tenure (usually less than 24 months) to meet their working capital needs. Such products enable automatic access to credit as lenders can tap into the entrepreneurs’ cash-flows to use them to help make credit assessments, disburse loans, and collect repayments linked to the sales automatically. The sales-linked repayment allows the entrepreneurs much more flexibility than a regular loan. Bidvest Bank in South Africa offers merchants a loan facility based on the business’s future turnover. It has designed MCA alongside Merchant Capital and catering South African MSMEs. Similarly, Neogrowth in India assesses creditworthiness based on the cash flows through the POS terminals of merchants. It electronically collects loans each day from the sales on the POS terminals, thus addressing issues around seasonality in merchants’ business.

- Receivables-based, invoice-based, and inventory finance help MSMEs easier access to credit. Like their larger counterparts, micro and small entrepreneurs also buy and sell on credit and maintain stocks and inventory—albeit in analog format. Lenders could help MSMEs digitize sales, cash flows, stock movement, invoices, receivables, and inventory details to assess credit risk and extend credit at a discounted value to the entrepreneurs. The receivables, invoices, and inventory could also act as a psychological guarantee. The increasing use of digital contracting and push from governments toward formal invoicing by enterprises irrespective of their size provides further impetus for this type of finance. Reserve Bank of India, which is India’s central banker, instituted an online bill-discounting platform, the Trade Receivable Discounting System (TReDS). This gave MSMEs the power to raise funds by selling trade receivables from corporates.

How can we help providers and entrepreneurs utilize digital approaches to enhance access to finance for MSMEs?

The market offers a clear opportunity to use digital tools to enhance access to finance, skills, and market linkages for enterprises through a multi-pronged approach at the level of policy and regulation, providers, and entrepreneurs. Such an approach will help resolve the legal, operational, and other barriers for enterprises to access finance, skills, and market linkages. Significantly improving digital financial services design and delivery will require an ecosystem-wide approach to enable entrepreneurs to choose, use, and prefer digital tools and approaches.

MSC plans to build a holistic Enterprise Finance Lab (enFinLab) to:

- Support providers develop customer-centric products;

- Support enterprises transform digitally;

- Build digital platforms to enhance better access to finance, skills, and market linkages; and

- Work with policymakers and regulators to build a conducive environment for the growth of enterprises.

We invite investors, donors, and financial institutions interested in partnering with us to get in touch to participate in the enFinLab and enhance access to credit to millions of un(der)served enterprises

Leave comments