Kenya moved towards electronic payments of social benefits in 2013. In 2018 the payments system for its premier social protection program, Inua Jamii, was restructured to offer most, but not all, beneficiaries a choice between several payment service providers (PSPs), all commercial banks. The Center for Global Development’s (CGD) study surveys the payment system from the perspective of recipients, including their views on convenience and the benefits from competition. It also considers whether these digital G2P payments programs have increased financial inclusion more generally – recognizing that this was already high in Kenya due to the market penetration of M-Pesa digital wallets.

It finds strong support for making payments through financial accounts. The overwhelming majority of respondents consider this to be a good system, with some favoring the commercial bank channel and others expressing a preference for direct payments through wallets. There is strong support for offering choice where this is feasible, but we find that the single payer G2P model can also be effective depending on local conditions. While social transfers may have enabled poor people to afford cell phones and mobile money accounts, the system can be developed further to enhance financial services access.

CGD partnered with MSC to conduct a survey of Inua Jamii recipients. For a detailed look into the findings, access the complete study here.

World Bank’s recent evidence and practice note on what works to support women-led businesses emphasizes the need to better target support to growth-oriented women entrepreneurs, consider women’s differentiated needs, and provide a package of support to overcome multiple constraints. MSC’s previous study with the Women Entrepreneurship Platform (WEP) found that women entrepreneurs require support in six critical ecosystem areas to develop successful businesses. One of these critical areas is entrepreneurial mentorship. The explosive growth of the Indian startup ecosystem has increased recognition of mentorship as an effective entrepreneurship development tool.

However, empirical research that examines its impact is yet to be undertaken. This study—Mentorship for Women Entrepreneurs—A Highway to Growth,” attempts to understand women entrepreneurs’ awareness, access, experience, and perceptions of the value derived from mentorship. In the study, we interviewed mentors across industries in India to understand their motivations and mentorship experience. This was complemented by a review of global evidence on the subject and an analysis of the country’s mentorship landscape.

Nitesh is a 31-year-old autorickshaw driver who migrated from Katihar in Bihar state of eastern India, to Delhi for a better job. He earns ~INR 700 (~USD 8.55) per day. After covering his basic living expenses, Nitesh saves approximately INR 11,000 (~USD 133) monthly. He remits this money to support his family back home in Katihar. For a long time, Nitesh used informal channels for remittance, such as hawala and over-the-counter (OTC) agents.

Although Nitesh found it convenient to send his savings monthly through these channels, the commissions charged by the agents bothered him. He tried to use alternate modes, such as the USSD-based mobile banking service *99#. Yet he found the process cumbersome and time-consuming. Nitesh is comfortable using a feature phone and does not want to upgrade to a smartphone anytime soon. He is keen to try UPI 123Pay to transfer money to his family. However, he wonders if it is safe and if he can use it independently.

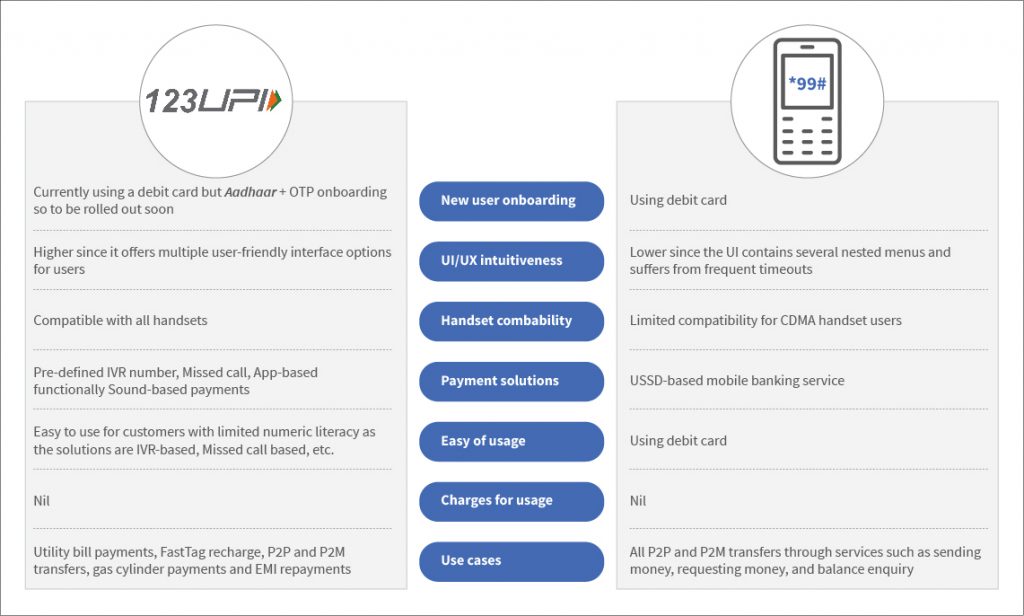

More than 400 million feature phone users in India like Nitesh have limited alternatives for digital payments on their feature phones. They continue to depend on physical access points for financial transactions. To cater to this segment of feature phone users, the National Payments Corporation of India (NPCI) integrated its USSD channel *99# into the Unified Payments Interface (UPI) ecosystem in 2016. *99# allows users to conduct financial and non-financial services using their mobile phones without using the internet. It aimed to make payments easier for users, especially those with feature phones. However, there has been limited uptake of the solution among the LMI segment for multiple reasons. One of the primary reasons for the limited uptake is the complicated payment process involved in *99# with a non-intuitive user interface. Subsequently, the transaction volume for *99# decreased significantly from 2.44 million in 2017 to 1.47 million in 2022, indicating a need to develop new and innovative solutions to facilitate payment for the feature phone user segment.

The launch of UPI 123Pay

With 10.586 billion transactions amounting to INR 15 trillion(~USD 189.64 billion) in August 2023, UPI has broken all records and has become the preferred choice of payment for digitally savvy Indians. Transactions conducted through UPI also create digital data trails for users. However, UPI’s penetration is limited mainly to the urban segments with high smartphone and mobile internet usage.

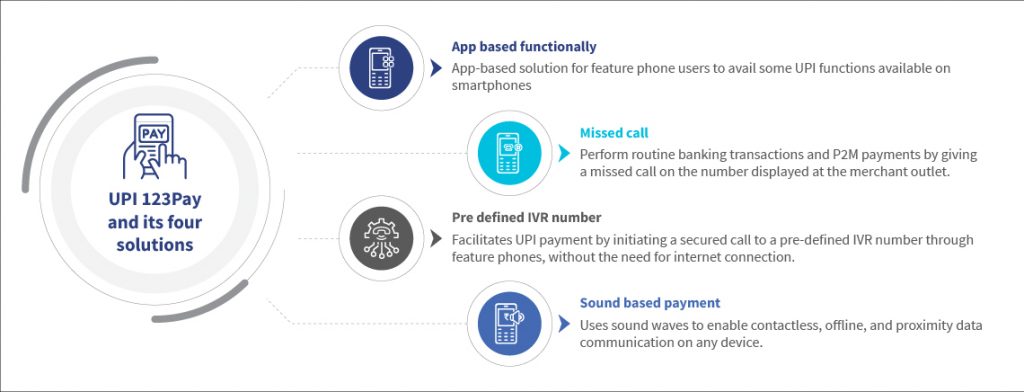

In March 2022, the Reserve Bank of India (RBI) and NPCI launched UPI 123Pay to offer digital payments to underserved segments of feature phone users. UPI 123Pay facilitates payments for feature phone users without needing internet connectivity. Through this, users can initiate payments to peers and merchants using UPI. The UPI-powered solution also supports smartphone users who prefer operating offline or with minimal internet connectivity. The current use cases of UPI 123Pay include utility bill payments, FASTag activation and recharge, mobile recharges, and fund transfers, among others. Users can undertake these transactions based on the following four technology alternatives that are currently live:

While smartphone users can also use UPI 123Pay, its primary target market comprises the underserved segment of feature phone users who are still dependent on the last mile access points or their friends/family for their financial transactions. Customers in remote locations often incur high costs, including travel costs, waiting at the business correspondent (BC) outlet, and the wages foregone when making periodic visits for their cash requirements. Wide-scale adoption of UPI 123Pay would significantly reduce these costs while improving ease of access for P2P and P2M payments for feature phone users.

Another challenge for people using digital payments, especially the feature phone segment and those in rural areas, is the lack of an active debit card. Most users of this segment struggle to keep their debit cards active due to low account balances, limited infrastructure for card acceptance, and limited knowledge of how to use the cards. Further, according to the latest data published by Global Findex, the debit card penetration in India is just 27%, and the majority of these users are based out of urban areas. The lack of active debit card limits a large chunk of the rural population to try and experience the digital payment convenience offered by UPI.

To solve for these issues, in September 2023, NPCI introduced the alternate onboarding process for UPI usingAadhaar + OTP. This is expected to simplify the process for feature phone users and help increase the uptake and usage of UPI further. The Aadhaar-based onboarding process is available to users in addition to the existing onboarding process using debit cards. UPI 123Pay is available in six vernacular languages: Hindi, Tamil, Telugu, Malayalam, Kannada, and Bengali. NPCI plans to introduce other languages as well. This would help resolve another significant barrier for feature phone users.

Furthermore, UPI 123Pay has also factored in the network and internet connectivity issues in remote and rural areas. All four solutions are built on technologies that work offline and do not require an internet connection. A look at the critical differences between *99# and UPI 123Pay highlights the different pain points that UPI 123Pay addresses for the feature phone users:

Barriers to the usage and scalability of UPI 123Pay

While these offline payment solutions offer massive growth opportunities in the feature phone users market, the uptake for UPI 123Pay has been slow since its launch in 2021. Major traction for the product is for use cases such as LPG gas cylinder payments, P2P payments, and mobile recharges. The solutions look promising and manage to overcome several barriers associated with *99#; however, a few concerns limit the uptake of UPI 123Pay among users. MSC’s analysis of the use of the IVR solution highlighted some critical insights into the process experience of UPI 123Pay for customers.

1) Limited comprehensibility of the users’ voice input

Users often have to pronounce their bank name multiple times while generating the UPI PIN, as the input gets disrupted due to differences in pronunciation or background noise. While users can also type the bank name as an alternative, the voice input provides more ease and convenience than the text input and is preferred.

2) Lack of a ‘favorites’ option

The solution currently does not have the provision to remember customer preferences such as frequent payee names’, frequently conducted transactions, or even the transaction history. This results in users undertaking these processes repeatedly, leading to a longer TAT that impedes the process experience.

3) Limitations in the current interface

First-time users, especially those with limited numeric literacy, require some assistance in onboarding while entering their debit card details and generating the UPI PIN. Hence it is not a completely independent process for the feature phone users in its current form. Users with limited digital readiness usually depend on others for transaction completion. MSC’s recent report “Decoding the extent and exposure of financial fraud among DFS customers” suggests that users’ dependency on others coupled with low digital readiness exposes them to financial fraud and risks. The risk increases even more for women users which is a major deterrent to the uptake of digital financial services among women.

Limited use cases in the IVR solution

Currently, the solution offers users limited use cases to transact. Recent MSC research for NPCI highlights the need to introduce use cases such as fee payments, postpaid bill payments, and rent payments, among others, to improve the uptake of the solution. While NPCI is working on adding new use cases, it will be critical to include use cases that cover the entire journey of a user’s financial needs lifecycle.

To further extend the usability and adoption of UPI across different segments, NPCI conceptualized Hello!UPI to make digital payments easy, accessible, and safe for users. The voice-activated payments solution is an extension to UPI 123Pay and allows users to use their voice for conducting transactions. Hello!UPI is available through two modes currently: on-call (through a voice call), and in-app (through any UPI app). MSC’s recent whitepaper on conversational payments (developed jointly with NPCI) suggests that the solution has immense potential to disrupt the payments space and bring millions of underserved users who are constrained by the lack of smartphones, Internet connectivity, and limited digital literacy into the folds of digital payments. All these are strong and positive steps to build pathways to a safe and inclusive payment ecosystem. Concerted efforts from NPCI and other stakeholders to develop inclusive payment solutions will benefit millions of underserved users like Nitesh and support them to kickstart their digital payments journey.

Sana is a clothes wholesaler from Uttar Pradesh in northern India. During the COVID-19 pandemic and the subsequent lockdowns, she took the leap to digital and registered her business on a B2B platform. Savitri, another clothes retailer from Maharashtra in western India, seeks an alternate supplier as she is unhappy with the cloth quality and designs offered by local wholesalers. In the current scenario, Savitri and Sana can only discover each other online if they register on the same application or platform. However, with the Open Network for Digital Commerce (ONDC), they could connect, even if they do not register on the same app or platform.

India has more than 63.39 million micro, small, and medium enterprises (MSMEs), which contribute 30.27% to the GDP and employ 111 million people. Yet these MSMEs face two related but significant challenges—access to capital and market. The overall credit gap in the MSME sector is estimated at INR 25 trillion (~USD 304 billion). In contrast, MSMEs’ overall debt demand in India is INR 69.3 trillion (~USD 843.19 billion), which continues to grow at 11.5% CAGR.

Women-led businesses (WLBs) comprise 20.37% of MSMEs in India. They are more vulnerable to these challenges. Many WLBs, such as those led by Sana and Savitri, have low awareness of business registration. They have limited digital literacy, which affects how well they can manage multiple selling apps and social biases. Around 90% of MSMEs in the country still operate offline, and 99% are microenterprises. Digital platforms or networks, such as ONDC, are emerging as a critical avenue to empower MSMEs, especially WLBs. These platforms have immense potential to foster innovation, increase sales through better reach, and reduce market risks.

What is ONDC?

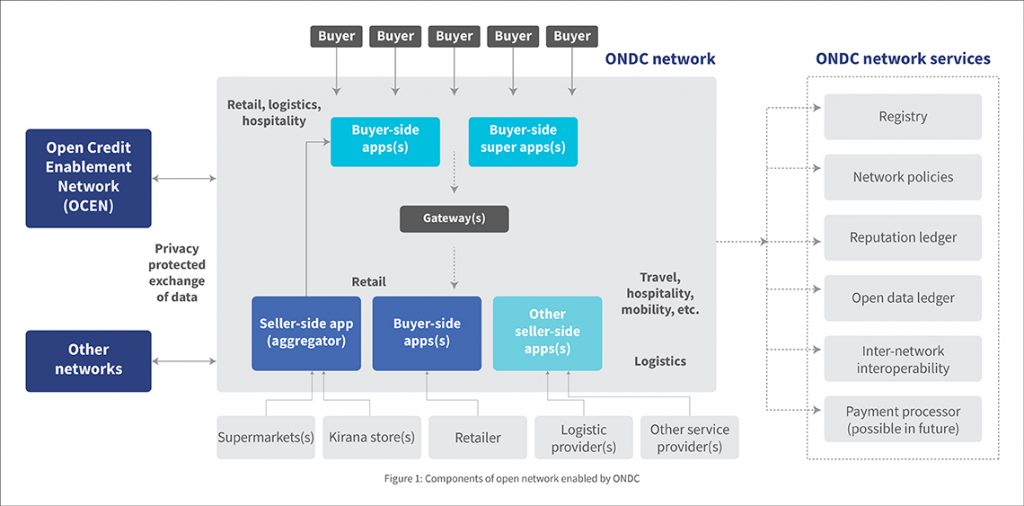

ONDC is an initiative to promote open networks for the exchange of goods and services over digital or electronic networks at a national scale. It enables sellers and buyers to be digitally visible and transact through an open network, regardless of the platform or application they use. It serves as a neutral platform to set protocols for cataloging, vendor matching, and price discovery on an open-source basis. Figure 1 showcases how the components of the open network enabled by ONDC interact with other networks:

Figure 1: Components of open network enabled by ONDC

In Figure 1, the ONDC network (at the center) comprises network participants, which join ONDC as a buyer-side app, seller-side app, or gateway to form the open network. ONDC network services (on the right) show the common services that enable network participants to transact on the network and create the digital infrastructure ONDC offers. Other networks (on the left) show open networks in other domains with which it can seamlessly interface, for example, the Open Credit Enablement Network (OCEN).

ONDC intends to replace the present platform-centric e-commerce model with an open-network approach. It is neither a super aggregator app nor a hosting platform. It only enables the discovery of location-aware, local digital commerce stores across industries and engagement with them by any network-enabled applications. It eliminates the need for buyers and sellers to register on common apps or platforms. This is possible through open communication protocols.

All digital commerce apps and platforms can voluntarily adopt and join the ONDC network. The network-enabled applications will continue to onboard sellers and buyers and manage end-to-end orders. As a result, e-commerce will be more accessible to all shoppers and vendors, which brings us to the next question.

How will ONDC help WLBs?

It enhances their discovery: When Sana decided to go digital, she had two choices—she could build her own digital space through an app or a website or list her products on marketplaces or aggregators. Yet an app or a website would cost a lot of time and effort. It would also impose limitations, such as policies, commissions, and brand preferences.

Figure 2: Potential of ONDC

MSC’s experience with WLBs in India suggests that most businesses struggle to scale through e-commerce, even though they have a smartphone and access to the internet. WLBs do not register their businesses online. This restricts their chances to sell on online marketplaces. Only 18% of WLBs have registered on the Udyam portal. They also hesitate to explore digital platforms as they believe their business is too small to enter the digital space. The considerable listing fee on e-commerce platforms and heavy documentation processes further dissuade them from going online.

ONDC has already onboarded prominent apps on the seller side, such as Meesho, Paytm Mall, and CoutLoot. Paytm alone acts as a digital storefront for more than 8 million small merchants. The merchants registered on these seller apps automatically get signed up on ONDC. However, offline merchants are also being encouraged to sign up.

The details around onboarding support and grievance resolution mechanism (GRM) are yet to be clarified by the ONDC officials. Yet ONDC has immense potential to onboard small merchants, such as Savitri and Sana, particularly if we consider the multiplier effects. It offers wide discoverability for small businesses and vast opportunities to expand into neighboring areas. Currently, ONDC does not charge any platform fee, but it might set a transaction fee of 1.5% later—a much lower sum than which e-commerce giants and aggregator platforms charge.

It improves access to finance: Despite a 75% increase in their numbers, WLBs’ share of the MSMEs’ annual turnover is a mere 20%. MSC’s reports and our work with WLBs, such as the SEWA Cooperative Federation, indicate that women-led businesses struggle with access to capital more than their male counterparts as they lack ownership of collaterals and legal documents to secure formal credit. Social norms exacerbate the situation and increase their reliance on informal credit sources.

Alternative financing, which otherwise has immense potential to bridge the credit gap, does not work for most small businesses, especially WLBs, as they lack digital footprints. The ONDC platform provides an immense opportunity to bridge the credit gap of WLBs, currently worth USD 158 billion. The platform can help generate digital footprints for small businesses through point-of-sale (PoS) data. Players in the alternative financing space can then assess creditworthiness through PoS data and offer WLBs small-ticket, customized credit.

It opens landscapes of opportunity: MSMEs, especially WLBs, struggle to meet changes in customer preferences and market trends due to a lack of customized training and skill development programs. ONDC can connect millions of WLBs to promote peer learning. The backend data and interaction with WLBs can serve as a powerful source to design and customize capacity-building programs. These programs can help bridge the skill gap and help millions of WLBs expand their business and sales.

ONDC’s story so far

Currently, e-commerce channels serve only 8-10% of the value market. ONDC can potentially increase this share to 22% by 2026. In April 2022, ONDC started its alpha testing phase with a closed user group of buyers in Bengaluru. By September 2022, it had expanded to more than 80 cities. The platform validated the apps in this phase and confirmed business and operational flows. Now in its beta testing phase, the general public can experience shopping on the interoperable platform and provide feedback.

But first, the ONDC model must overcome issues related to platform iterations and general awareness among the users to achieve this. It should also consider the possibility of commercial mismatch, especially for kiranas. These small stores operate on thin margins (5%-20%) and cannot afford to pay a 3% cut to the apps that onboarded them and another 2-3% to those who facilitate payments andbear logistics costs. Lastly, the model must account for open competition based on price discounts between large and small sellers, as larger sellers can afford to offer heavy discounts to customers due to economies of scale.

Yet despite challenges, the open network holds vast potential. It can curb digital monopolies and transform India’s e-commerce sector to a more platform-agnostic model. In the days to come, ONDC could generate inclusive growth and bring millions of micro-merchants, much like Sana and Savitri, into the folds of the digital commerce revolution and fuel their growth, dreams, and aspirations.

World Bank’s recent evidence and practice note on what works to support women-led businesses emphasizes the need to better target support to growth-oriented women entrepreneurs, consider women’s differentiated needs, and provide a package of support to overcome multiple constraints. MSC’s previous study with the Women Entrepreneurship Platform (WEP) found that women entrepreneurs require support in six critical ecosystem areas to develop successful businesses. One of these critical areas is entrepreneurial mentorship. The explosive growth of the Indian startup ecosystem has increased recognition of mentorship as an effective entrepreneurship development tool.

However, empirical research that examines its impact is yet to be undertaken. This study—Mentorship for Women Entrepreneurs—A Highway to Growth,” attempts to understand women entrepreneurs’ awareness, access, experience, and perceptions of the value derived from mentorship. In the study, we interviewed mentors across industries in India to understand their motivations and mentorship experience. This was complemented by a review of global evidence on the subject and an analysis of the country’s mentorship landscape.

Watch this video to get the key insights from the report.

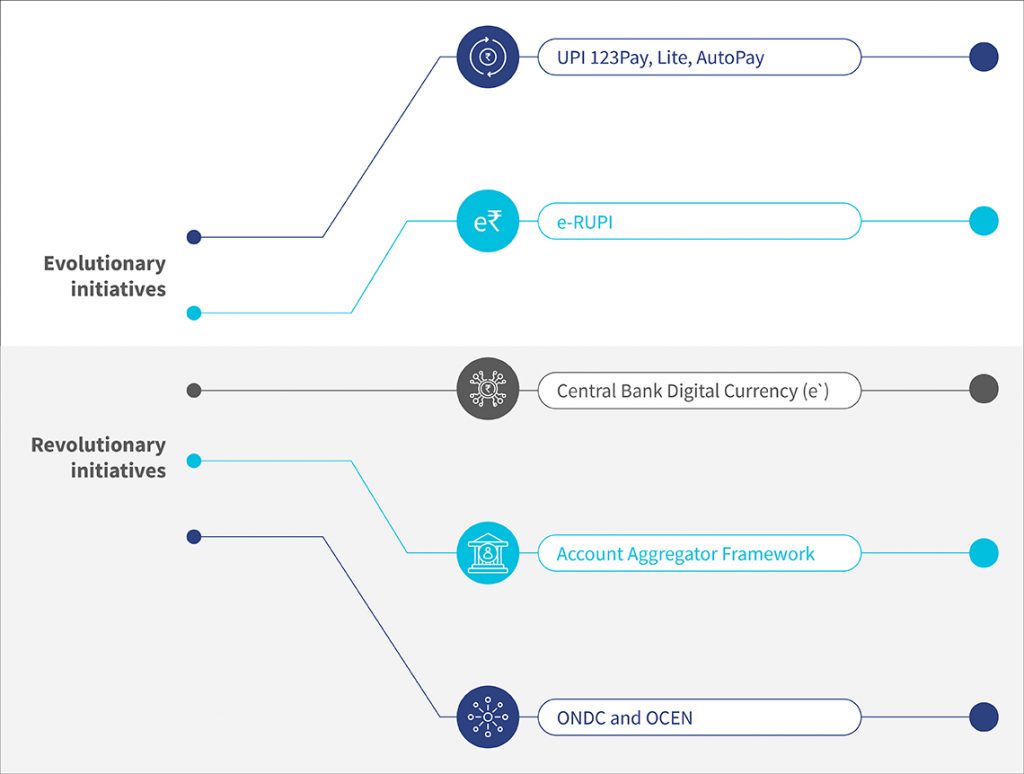

In our previous blog, we discussed the various factors that led to the rise of digital payments in the country, and also highlighted the evolutionary measures that will help us unlock the USD 10 trillion opportunity. In this blog, we highlight a few revolutionary initiatives that have bridged the gap further for the historic transformation of India’s digital financial services space.

Revolutionary initiatives

Central Bank Digital Currency (e₹)

The RBI’s Central Bank Digital Currency (CBDC) is a significant step in the evolution of currency that can change the way money works. The RBI defines CBDC as the legal tender issued by a central bank in a digital form akin to sovereign paper currency. CBDCs are exchangeable at par with the existing currency and shall be accepted as a medium of payment, legal tender, and a safe store of value.

The RBI launched CBDC’s first pilot in the retail segment in December 2022, known as digital Rupee-Retail (e₹-R), within a closed user group comprising participating customers and merchants. Mumbai, New Delhi, Bengaluru, and Bhubaneswar. State Bank of India, ICICI Bank, Yes Bank, and IDFC First Bank issue e₹-R in the form of a digital token representing legal tender in the same denominations that paper currency and coins are currently issued.

Users can make P2P and P2M transactions with e₹-R through a digital wallet the participating banks offer and stored on mobile phones or devices. As in the case of cash, e₹-R will not earn any interest and will be converted to other forms of money, such as bank deposits. Through this product, CBDC expects to reduce operational costs involved in physical cash management, foster financial inclusion, and bring resilience, efficiency, and innovation to the payments system. The use of e₹-R will also add efficiency to the settlement system, boost innovation in the cross-border payments space, and provide the public with use cases private virtual currencies provide without the associated risks. CBDC’s offline functionality would also benefit users in remote locations with limited electricity or mobile networks.

Account aggregator framework

India’s account aggregator (AA) framework is a consent-based system under IndiaStack that enables data sharing across financial institutions. In this case, account aggregators will serve as consent managers who permit an easy flow of financial data by serving as a conduit between customers’ financial information providers and users. The AA framework enables users to link all financial accounts securely to one data handle and provide consent to share the data with other financial institutions. Currently, 56 banks, FinTechs, NBFCs, and ~1.1 billion customer accounts are live on the AA system.

The AA framework will democratize financial services through easy, secure, and consent-based data transfer, give customers more control over their data, and reduce processing costs for banks and NBFCs through better access to data. More recently, the RBI included the Goods and Services Tax Network (GSTN) in the AA network as a financial information provider to facilitate cash flow-based lending to the micro, small, and medium enterprises that lack credit history based on their GSTIN records.

However, we are yet to learn how it will impact low and middle-income segments in rural markets that have limited or no digital footprint with low financial literacy. Our blog on the DEPA framework discusses one of AA’s most highlighted use cases—lending.

Open Network for Digital Commerce (ONDC)

India has the third-largest online shopper base globally, with 140 million e-retail shoppers. However, this number comprises only 18% of the country’s 761 million mobile internet users. On the supply side, around 12 million kiranas, which are hyperlocal neighborhood provision stores ubiquitous across the country, account for 80% of the retail sector in India. Among them, 90% are unorganized or self-organized, and most remain digitally excluded. Moreover, ~63 million MSMEs in the country can potentially unlock innovation and scale their operations through digital commerce. ONDC with OCEN can potentially support the growth of these kiranas and MSMEs and many customers by building a data trail, increasing outreach, and providing access to credit.

ONDC is an initiative to promote open networks for exchanging goods and services over digital or electronic networks at a population scale. The neutral platform is designed to set protocols for cataloging, vendor matching, and price discovery on an open-source basis. It enables sellers and buyers to be digitally visible and transact through an open network, regardless of the platform or application they use. Adding on the OCEN layer, ONDC will enable customers and businesses to borrow through any of these e-commerce or other apps. This will involve a standardized process with APIs for every stage of the customer lending lifecycle to support the integration of lenders with other digital platforms, including e-commerce.

Conclusion

These initiatives can potentially drive India’s digital payments growth and unlock the USD-10 trillion opportunity by 2026. Embedded payments via 5G and the Internet of Things (IoT) will provide further impetus. Building customer trust through better fraud management and easy digital onboarding remains imperative. So does improving economics for payment players.

Entities such as the RBI, NPCI, and FinTechs will prove crucial to facilitating this growth. How these initiatives will affect the digital divide and the low and middle-income segments, especially vulnerable communities, remain to be seen. Regulators and service providers can address some of these concerns by enabling customer-centric interfaces, agent-assisted support, last-mile distribution networks, and robust grievance resolution mechanisms.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.Ok

Barriers to the usage and scalability of UPI 123Pay

Barriers to the usage and scalability of UPI 123Pay