Adopting a segmentation approach to serve enterprises in Kenya: Insights from the FinAccess Household Survey 2021

by Aakash Mehrotra, Lakshay Jain, Rahul Chatterjee and Chinmay Dabhade

by Aakash Mehrotra, Lakshay Jain, Rahul Chatterjee and Chinmay Dabhade- Dec 9, 2022

- 3 min

by

by  Dec 9, 2022

Dec 9, 2022 3 min

3 minWe used the FinAccess data to develop a composite score-based index. This index helped us segment these MSMEs based on their sophistication levels to identify their business needs and growth opportunities and maximize their business sophistication levels. In this blog, we discuss our findings from this segmentation exercise.

“I do not have a bank account or an M-PESA till number,” sighs Ronah, who runs an unregistered fresh produce shop in Busia on Kenya’s southwestern border. Far away in the southeast in Mombasa, William operates a registered grocery store with three workers and wants to know how to upgrade and digitize his business. Meanwhile, in Nairobi, electronics shop owner Doreen employs 20 employees and seeks to expand her business and access hassle-free credit. All of them aspire to grow their businesses.

Ronah, William, and Doreen are among the millions of spirited people who comprise Kenya’s micro, small, and medium enterprises (MSMEs) sector, which contributes to approximately 25% of the country’s GDP. They make up more than 90% of private enterprises and employ around 93% of the Kenyan labor force (FSDK,2021).

Most government policies treat MSMEs as a monolithic, homogenous group and do not recognize the complex range of sub-segments within—each with specific characteristics, behaviors, and needs. A one-size-fits-all approach will not create customized solutions to enable small businesses to grow. In response, MSC analyzed the different MSME segments to assess how businesses vary according to their sophistication.

Segmenting enterprises in Kenya

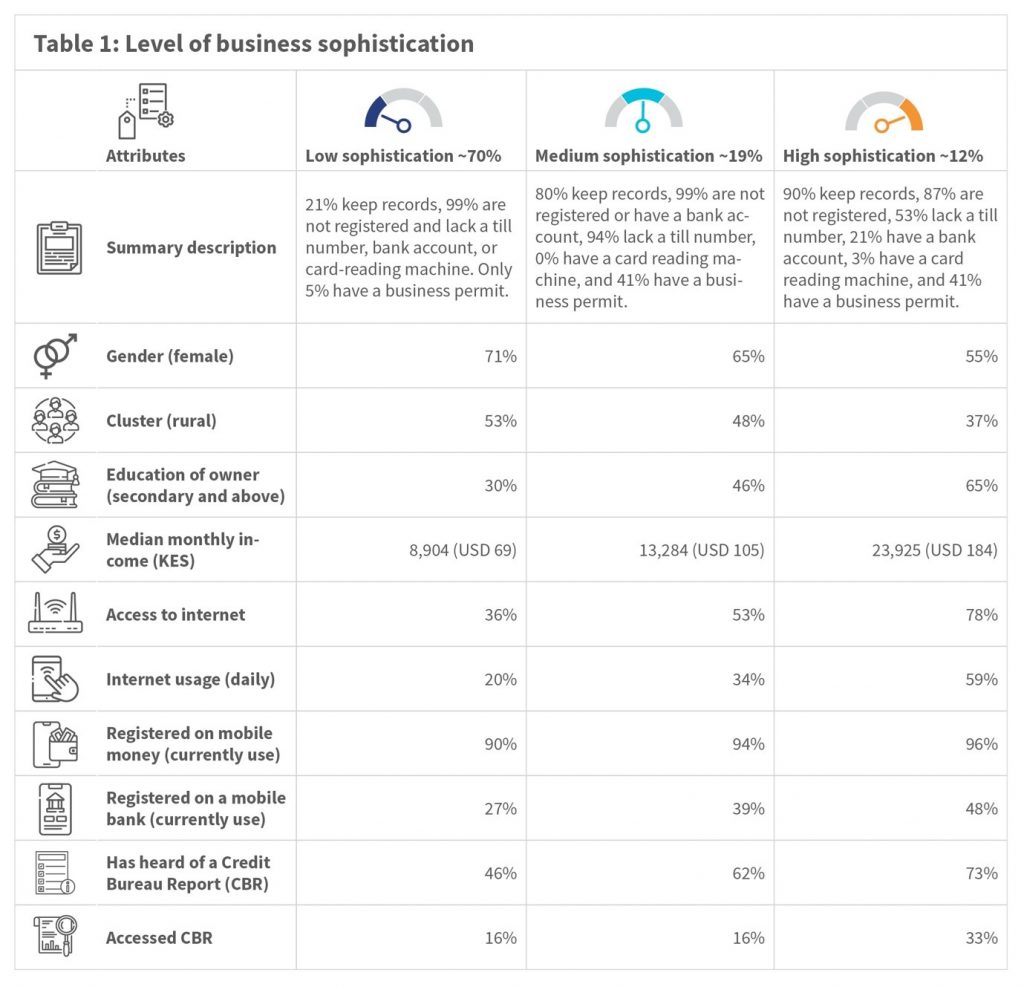

We used the FinAccess Household Survey 2021 to create a composite score-based index for the sophistication of enterprises. The variables used for the segmentation were: the number of paid workers, availability of written books of account, till number, bank account, registration number, and business permit.

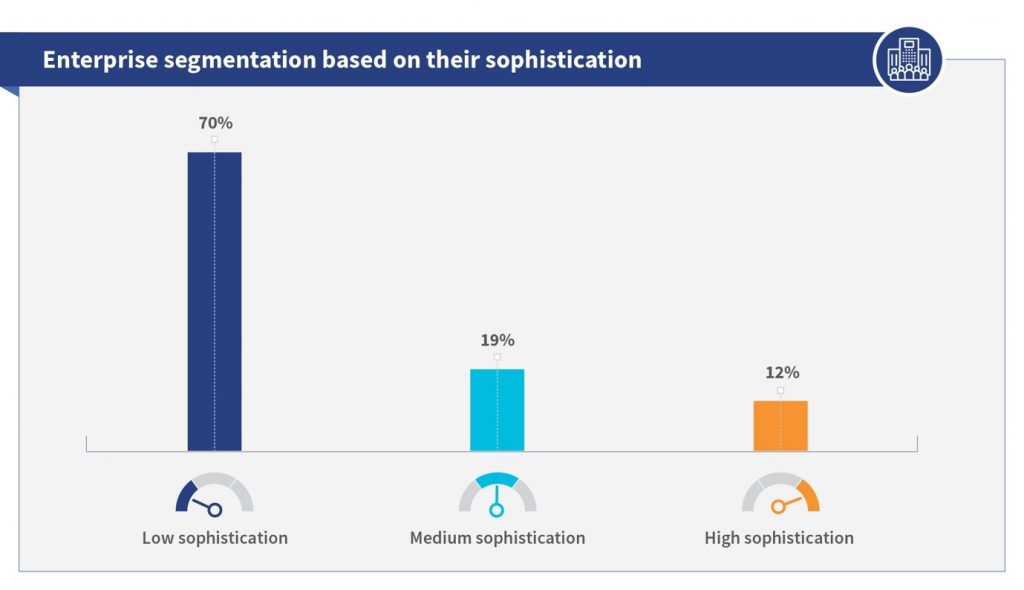

Using this methodology, we found that 70% of the enterprises in Kenya fell in the category of “low-sophistication.”

The categorization is based on how enterprises function. Yet it also highlights how well these enterprises perform business operations and access financial services. Enterprises with low sophistication are run predominantly by women with low levels of education and are concentrated in rural areas. On average, these enterprises pay lower wages to their employees than their more sophisticated counterparts. Entrepreneurs managing high-sophistication enterprises have better internet access and use mobile money more frequently.

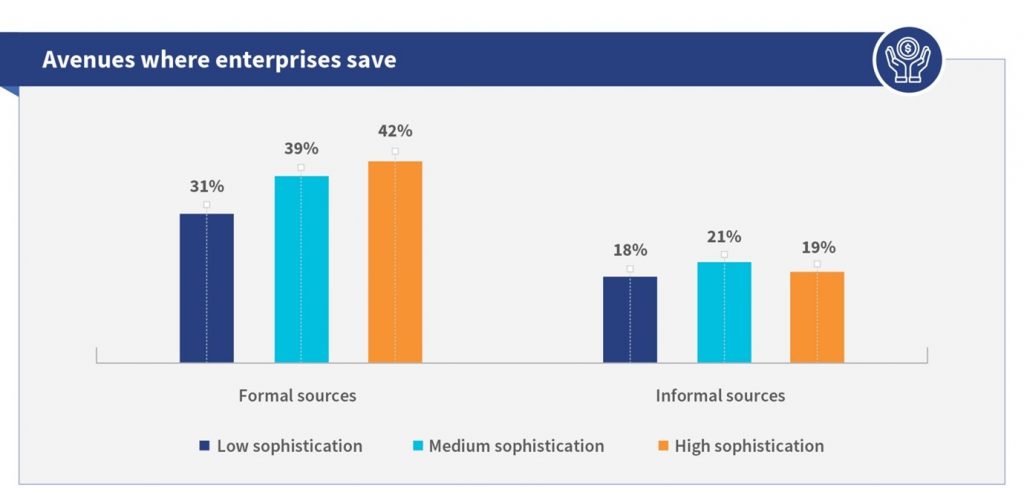

Source of savings and credit

Business sophistication also directs how these enterprises manage and access their finances. A more sophisticated enterprise is more likely to access its Credit Bureau Report (Table 1) and save with formal channels or avenues, such as banks, and mobile money.

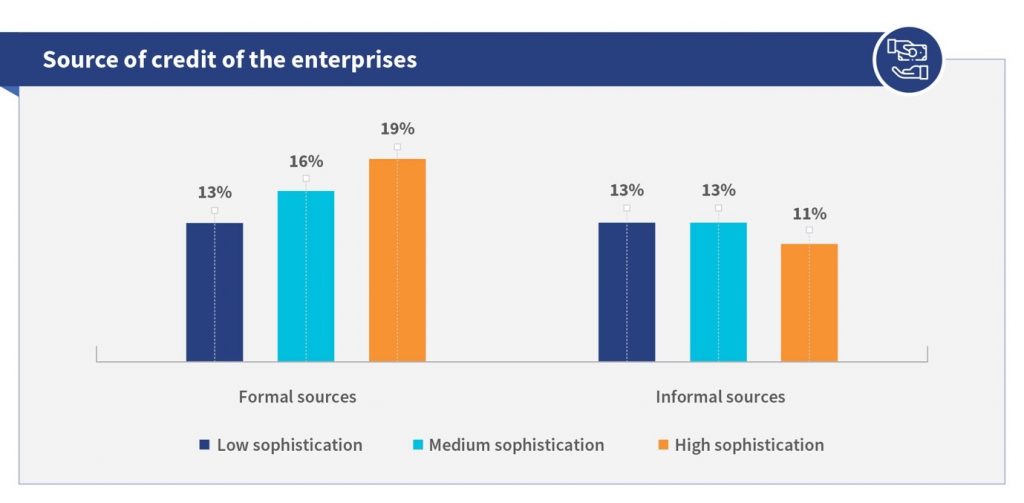

Enterprises with higher sophistication were more likely to use formal sources of credit than less sophisticated enterprises. Lack of collateral and financial records are among the reasons for the exclusion of these enterprises. The lack of credit from formal sources stifles the growth of all categories

Financial resilience of enterprises

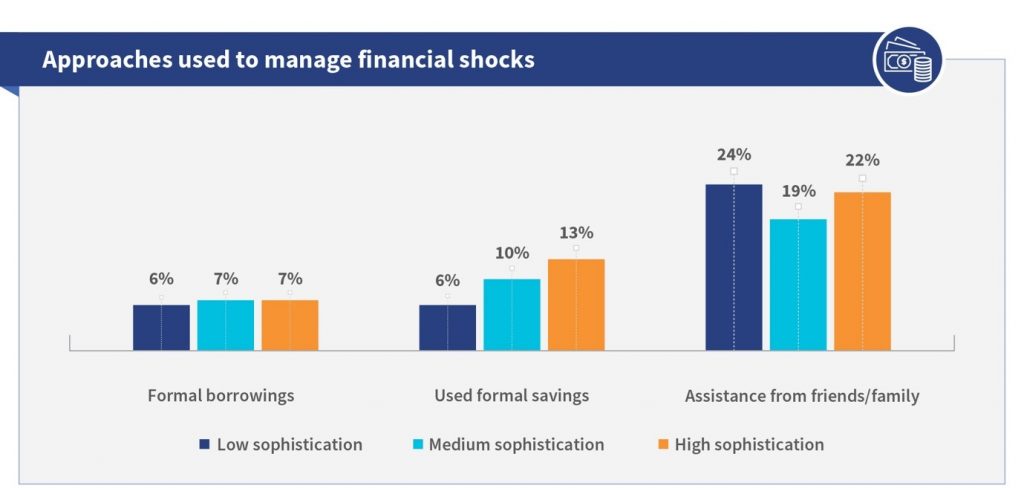

Findings from the FinAccess Household Survey also suggested low financial resilience of the enterprises, irrespective of their sophistication. Major unforeseen events, such as the pandemic itself, highlight the need for enterprises to have access to financial services to help manage risks and short-term adversity. Our June 2020 report on the “Impact of the COVID-19 pandemic on MSMEs” discusses how the pandemic significantly hurt the income of these businesses and disrupted supply chains and cash flows. About 6% of enterprises used formal borrowing and saving channels to cope with the shocks, while 22% relied on assistance from friends and families. However, the various segments displayed minor differences. More sophisticated businesses were better placed than the others to use formal savings and credit to manage shocks.

Access to banking products

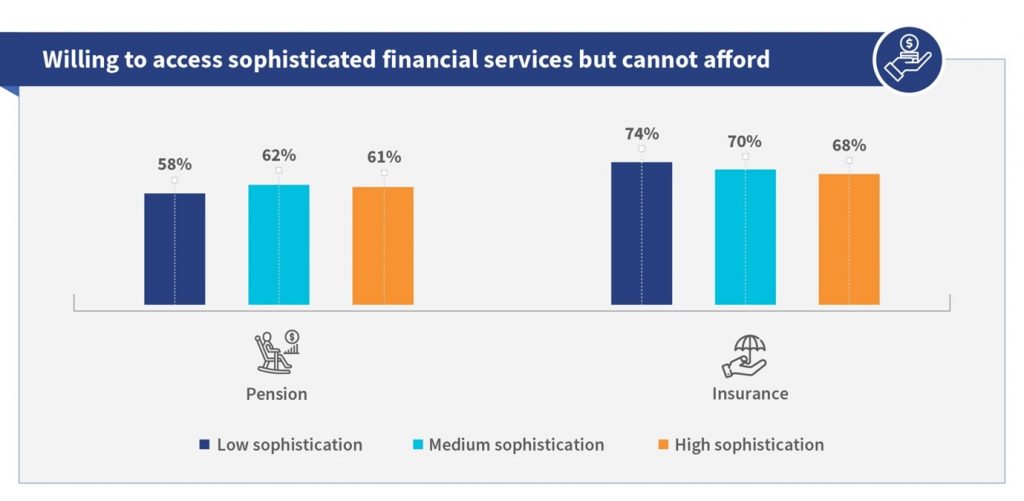

Most entrepreneurs were keen on insurance and pension facilities but cited affordability as a significant hurdle. Less sophisticated businesses were least likely to afford the insurance coverage they wanted. A report by UNCTAD discusses how insurance coverage for enterprises still largely remains a distant aspiration. The affordability of pension schemes is similarly challenging for all business owners. Barriers associated with product design, distribution channels, and a lack of insurance culture require collective participation from the public and private sectors to overcome.

The segmentation analysis makes the challenges faced by enterprises more distinct. More details about the operations of the different categories of enterprises will provide an even clearer picture on the challenges faced, and needs and aspirations of the enterprises. For example, many challenges are seasonal, while others have more predictable and consistent course. Nevertheless, the segmentation analysis helps us understand the enterprises better and makes strategizing for immediate response to ensure short-term survival and build their resilience for the long term easier.

Leave comments