Financial Capability and Indian Digital Financial Services

by Graham Wright and Soumya Harsh Pandey

by Graham Wright and Soumya Harsh Pandey- Apr 28, 2016

- 4 min

by

by  Apr 28, 2016

Apr 28, 2016 4 min

4 minThe author predicts the future of mobile money based on his experiences, market insights and observations from working many years within the mass financial sectors and in Digital Financial Services.

The World Bank Institute highlights that behavioural change with regard to financial capability is a non-linear process and requires more than receiving compelling information. For an evolving channel like DFS, which has several models of service delivery, this brings its own set of challenges. For DFS to be used to its full potential, it is important that both customers and agents have functional knowledge of the channel.

Therefore, under MicroSave’s study for the Omidyar Network on customer protection, risk and financial capability in India, financial capability of the customers was assessed on the basis of:

- Functional knowledge to transact on their own

- Awareness about terms and conditions and product features

- Ability to protect personal account information

- Awareness and ability to access recourse

Financial capability of the agents was assessed on the basis of:

- Functional knowledge about terms and conditions and product features for proper facilitation

- Functional knowledge about recourse mechanisms to help the customers as well as to resolve problems they face

- Monitoring and training support so that agent is able to serve the clients well

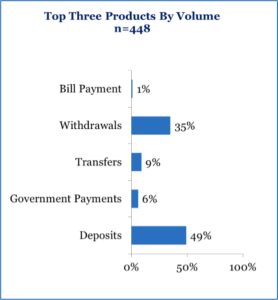

As indicated in a previous blog “Customer Protection in Indian Digital Financial Services (Part 2: Transparency and Privacy)”, almost 2/3rd of customers do not fully understand the product terms and conditions and pricing. Furthermore, knowledge about other products among agents is also low, and so they offer only a few products. The graph indicates the top three products offered by agents by volume.

Furthermore, field observations show that there is a growing trend amongst customers to carry out over the counter (OTC) transactions. These people are not covered in the study, but form a significant proportion of transaction volume. Since they conduct OTC transactions, it is fair to assume that they too have very limited knowledge of the terms and conditions of service.

Functional awareness among agents to facilitate transactions appears high. However, this does not represent the complete picture as they only have knowledge about a few products. MicroSave’s ANA India Survey highlights that only 59% of agents received training. Of those trained, 61% agents have undergone a refresher training. 36% of these have received refresher training only once.

In the MicroSave study for the Omidyar Network 96% of agents said that they knew about the product features of top three products on offer through their agency; 77% of agents said that they do not have any difficulty in handling the devices/technology; and only 68% of all active agents reported having received documents describing terms and conditions of service.

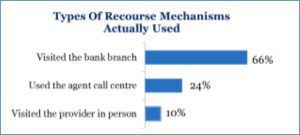

79% of the agents know about recourse options. However, of the agents who faced issues, only 24% actually used any kind of recourse option. Though agents were aware of multiple recourse options, the method actually used to resolve issues was much more traditional in nature ― agents preferred to sort out issues face to face at the branch.

This indicates that even though there is awareness about recourse options among agents, they are not used much. Moreover, the dependence on agents on going to the bank branch or provider for recourse suggests that call centres are either absent or not functioning adequately. This also raises a question on the ability of agents to resolve customer level issues if they do not have functional knowledge of recourse.

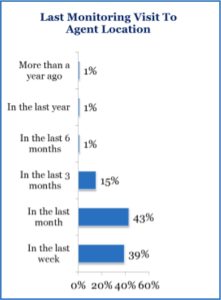

However, when asked what is discussed during monitoring visits, the answer was ambiguous both in terms of agenda and problem resolution.

A separate baseline assessment study conducted by MicroSave, for Bank Mitrs (agents) under the PMJDY scheme also highlights the fact that monitoring visits lack an agenda in terms of what needs to be checked, and often does not resolve any problems/issues that the agent/customer may be facing. At best, during monitoring visits, the bank staff checks the notebook of agents in which transaction records are maintained. There are almost no checks/interactions with customers during monitoring visits. This is primarily to avoid questions on unresolved issues like – When will they get their passbook? When will the ATM card be issued? Will they be able to access credit? etc.

Financial capability in terms of product knowledge and recourse is limited amongst agents and very limited amongst DFS customers in India. Furthermore, there is little sign that the sporadic agent monitoring visits are being used to address this problem. Providers and banks should view this as a big opportunity to both improve levels of trust in DFS and the range/uptake of products and services by the mass market. But, to achieve this, concerted efforts will be required to enhance the financial capability of both the agents and the customers they serve.

Written by

Graham Wright

Group Managing Director

Leave comments