Winter is coming: Digital disruption and its impact on the financial services industry

by Anup Singh

by Anup Singh- Sep 15, 2018

- 4 min

by

by  Sep 15, 2018

Sep 15, 2018 4 min

4 minA convergence of technology with finance, which, in turn, resulted in the emergence of FinTechs, has been changing the very fundamental nature of the financial industry.

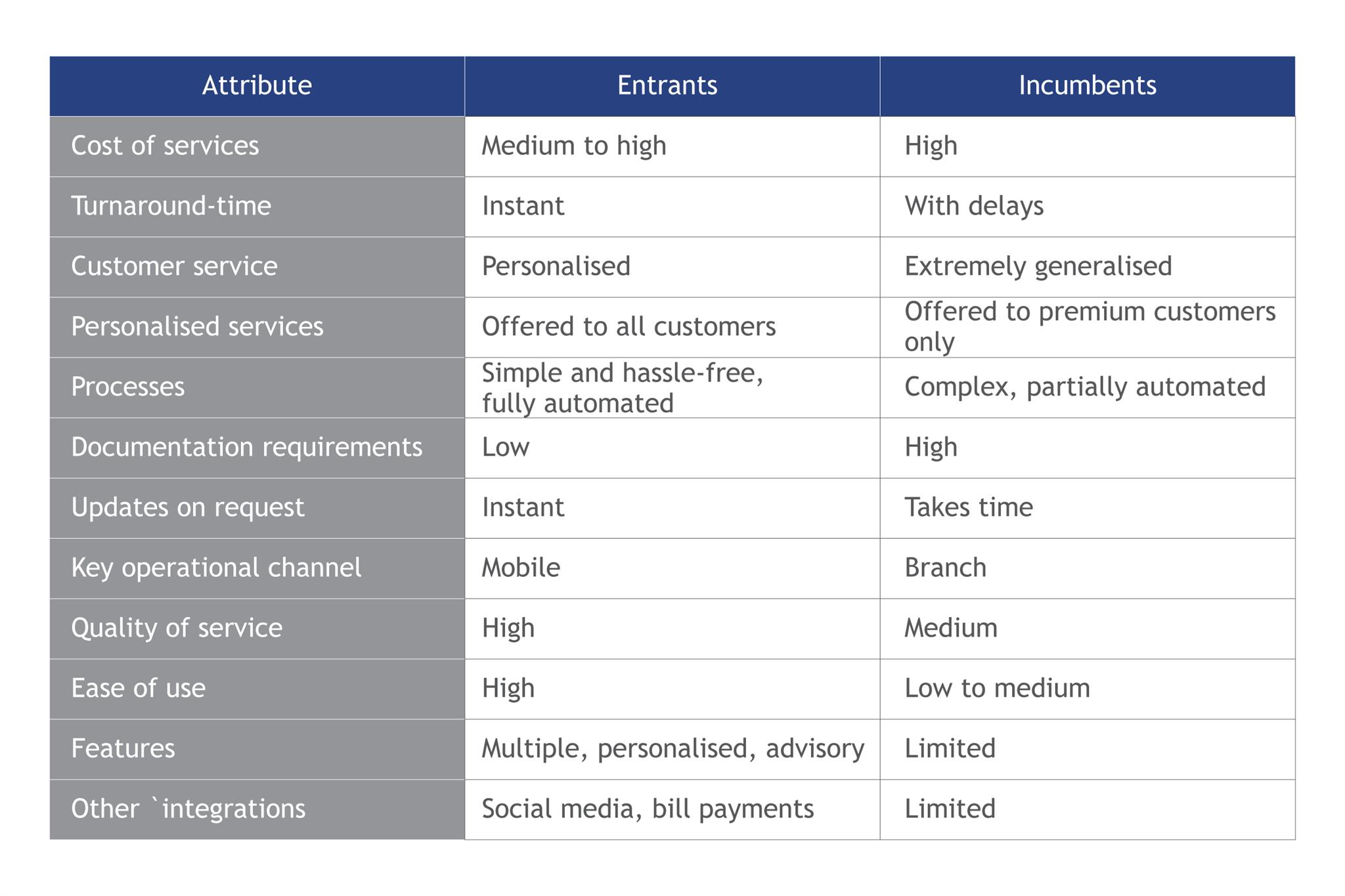

The financial services industry is changing rapidly. A convergence of technology with finance, which, in turn, resulted in the emergence of FinTechs, has been changing the very fundamental nature of the financial industry. Apart from technology, demographic and cultural shifts continue to alter the financial services value chains. Traditional financial institutions are losing their market share to technology-enabled entrants due to specific factors. The table below showcases these in detail.

Banking and financial services used to be the stronghold of traditional financial institutions or the “incumbents”. These providers had a number of advantages related to their size and scale and were able to serve a substantial part of the market. However, many have also had high-cost branch networks and legacy IT systems. This rendered them sluggish to adapt to the new digital world and also led to some consumers being considered unprofitable, with negative consequences for mass market growth.

In the past, the financial services industry used to have high barriers to entry with respect to capital and regulatory requirements. However, these entry barriers have been gradually reducing, thereby spawning innovative, technology-enabled entrants who disaggregate the financial services value chains and challenge the incumbents.

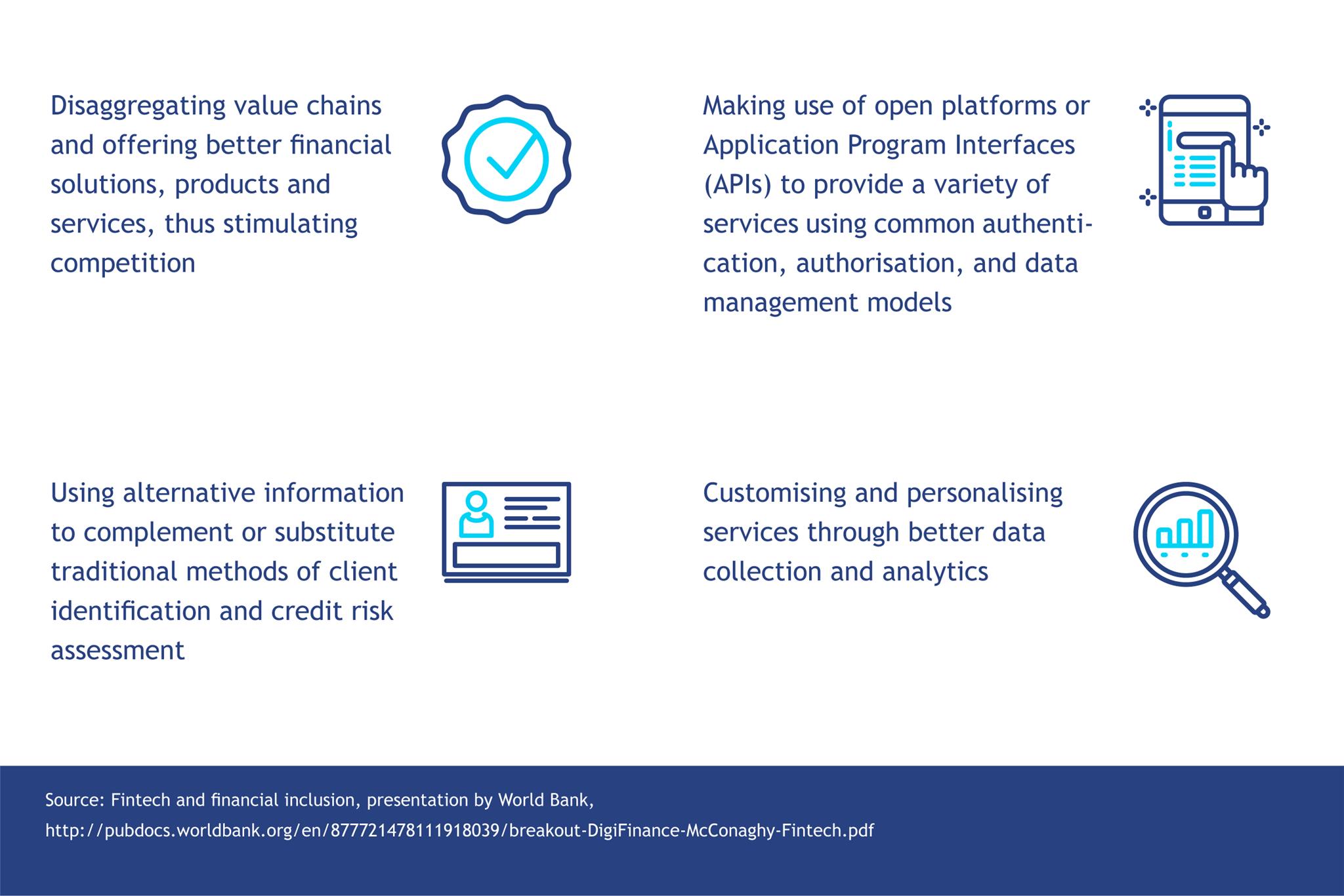

The landscape and context are changing. Market share, revenue, and profit have ultimately defined institutions in the financial service industry.As the prominence of these financial institutions dwindles, technology-enabled entrants have emerged to fill up the void. Since FSPs had not been able to meet the evolving needs of customers, the emergence of technology-enabled entrants has largely been a demand-side phenomenon. Such entrants target strategic niches, develop customer-centric solutions aimed at achieving a specific objective, improve customer experience, and interface and deliver these solutions using technology. They disrupt the financial services and financial information in a number of ways. The table below illustrates these.

The question is, “How is the rapid digital disruption of the financial services industry affect the incumbents?” Financial institutions struggle to balance three potentially-competing objectives:

- To provide financial intermediation services at a cost that makes business sense for the financial institution;

- To reach a large number of customers efficiently; and

- To accomplish the first and second objectives while managing the risks.

Financial institutions often find that these three desired objectives are not independent of each other and may require trade-offs. However, with the use of the digital disruption tools, agile and nimble entrants have found a way to manage the right balance between these objectives by:

- Using technology-enabled channels, such as mobile phone and agents to provide financial intermediation services at a significantly lower cost compared to the incumbents;

- Making use of digital means to reach a large number of customers at one-tenth of the cost compared to the incumbents;

- Identifying, monitoring and managing a variety of risks associated with financial service provision using technological approaches (artificial intelligence (AI), machine learning (ML) and auto triggers).

With the use of technology, the entrants have managed to:

- Improve customer experience by making it easier and more intuitive to perform financial transactions and by providing more transparency in the process;

- Provide better access to financial solutions using advancements in technology to allow customers and businesses to transact anytime, almost anywhere in the world. and across a range of devices;

- Lower operating costs and increase process efficiency using the new tools developed through technological innovations – the tools transform the way financial services firms operate by making the processes faster and more efficient.

The entrants have a significant edge over the incumbents in the following areas:

The end-users of financial services prefer the entrants over the incumbents. This is because of ease of use, faster services, good experience, lower cost of access to financial solutions, availability of a higher number of services and features, value-added services, instant gratification, and highly personalised services.

The end-users of financial services prefer the entrants over the incumbents. This is because of ease of use, faster services, good experience, lower cost of access to financial solutions, availability of a higher number of services and features, value-added services, instant gratification, and highly personalised services.

It is worth noting that the incumbents have an edge over the entrants when it comes to existing customer bases, innate customer awareness, human touch, and regulatory clearances or compliance. If they are able to utilise these and transform digitally, they have high chances to retain or even enhance their market share.

Digital disruption has the potential to shrink the role and relevance of the incumbents. But it simultaneously helps them create better, faster, and cheaper services that can render them well-equipped to better serve their customers. In order to avail of these opportunities, traditional FSPs need to acknowledge the digital disruption, overcome institutional complacency, and embrace digital transformation.

In the next series of this blog, we discuss how traditional financial institutions can go about the digital transformation to utilise the disruptive power of technology, innovation, and digital disruption.

Written by

Leave comments