Customer Vulnerability, Trust and Risk in Indian Digital Financial Services

by Graham Wright and Soumya Harsh Pandey

by Graham Wright and Soumya Harsh Pandey- Apr 26, 2016

- 4 min

by

by  Apr 26, 2016

Apr 26, 2016 4 min

4 minThere is strong evidence that poor customer service/protection is reducing not just uptake but also usage of DFS services. What are the challenges and how can DFS providers address them.

Qualitative research done as a part of MicroSave’s study for the Omidyar Network on customer production, risk and financial capability in India shows that customers’ perceptions of banking or financial transactions are still focused on brick and mortar based services. DFS providers have not done enough to change the customer’s perception and gain trust. The customer’s perception of risk of digital systems and technology can be further broken down into three broad issues.

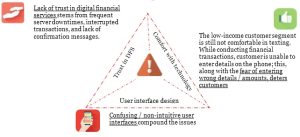

1. Lack of trust in digital financial services arises from three key drivers:

a. Frequent server downtime: Many issues are clubbed here – including: bank server downtime; provider’s network downtime; failure or overload of the middleware linking the bank system to the provider’s system; and internet or GSMA outage. In addition, on occasions, the agent’s unwillingness (or inability due to lack of liquidity) to service the customer is covered by the agent with an assertion that “the system is down”.

b. Interrupted transactions: Often, while transacting, agents/customers face the problem of interrupted transactions. This can happen due to various technology challenges and often results in incomplete transactions.

c. Lack of confirmation messages: Lack of a confirmation message, or receipt, or any form of physical evidence of the transaction, causes anxiety amongst many customers.

2. The low-income customer segment is still not comfortable in texting for two reasons:

a. Unable to enter details: In the case of mobile delivery channel, many old and middle-aged customers are unable to type details on the phone.

b. Fear of entering wrong details: Customers do not want to conduct transactions (themselves) because they are afraid that they might enter wrong details, and thus lose money.

Customers’ low level of comfort with technology is exacerbated by often clunky user interfaces (see below) and often leads to agent-assisted transactions. Assisted transactions significantly increase the level of risk for the customer as they have to share their account details with the agent. Further, it also harms the service provider in the following ways:

• Increased risk of fraud and hence reputational risk

• Agents start behaving like middlemen, limiting the providers’ communication with clients; exposing the provider to the risk of customer poaching (if the agent is not satisfied with the service/commission given by a provider, he shifts to a different provider and also shifts the customers along with him), and limiting opportunities to cross-sell.

3. Confusing/non-intuitive user interfaces compound the issues

a. User interfaces are often confusing to the customer. The USSD interface is often too deeply layered or embedded for the customers to get to the right option. This forces the customer into risky behaviours like:

• Sharing PIN with the agent

• Leaving cash with the agent (especially when the system is down or alleged to be down)

• Leaving phones with agents to complete a transaction

b. Transaction data security relates to the privacy of customers’ account/PIN details while conducting transactions at agent locations. Poor transaction data security increases customers’ vulnerability to external frauds. Confusing interfaces and low comfort level with technology add further to poor transaction data security, as the customer is forced to share personal account details.

Two other issues further erode customers’ trust in digital finance in India:

1. Lack of liquidity at the agent is a multi-fold issue. For the customer, it means that their funds are inaccessible and service is denied. A customer who has been refused service by an agent is less likely to transact again at that agent location. Furthermore, loss of business reduces profitability and demotivates the agent, so he starts maintaining minimum (or less) liquidity – thus setting in motion a downward spiral.

2. The perception that funds held digitally are not safe. This stems from rumours which spread in the market from time to time. For example, in 2014, in response to government policy, agents were given a target of 100% withdrawal of government payments to receive their commission from the agent network managers. So, (unsurprisingly) agents communicated that customers must withdraw all their direct benefits immediately or the government would take back the amount left in the account.

These issues are very similar to the ones we found in Bangladesh, Uganda and (to a lesser extent) the Philippines (see graph below).

There are, however, important consequences of these issues and risks for DFS uptake and usage. Fears and perceptions suppress uptake and tarnish the reputation of DFS and its providers. Non users are often very aware of these issues. In the words of one customer, “We keep hearing mobile money users complain about unstable network, delayed service, missing money and many other negative comments about mobile money. Why then should we register for these services?”

There is strong evidence that poor customer service/protection is reducing not just uptake but also usage of DFS services. Many registered customers lapse into inactivity when they find it impossible (due to system downtime or absent/illiquid agents) or too scary (due to the risks of sending money to the wrong number or losing/compromising their PIN) to make transactions. Others choose to self-protect by using OTC services in preference to registering or keeping money in their m-wallets. These all limit the use of digital financial services. This was a repeated theme across the studies and reflects the findings of InterMedia’s work in eight leading markets across the globe. MicroSave’s recent work for UNCDF’s MM4P on the customer journey highlighted that, “Moving people from knowledge to trial, and from trial to regular usage, will require providers to address issues that erode trust: system instability, poor customer service; and improve access which is limited by current KYC requirements”.

System downtime and sending money to the wrong number, in particular, seem to damage the reputation of DFS service providers. Ironically, these technological issues can be addressed by providers themselves. Similarly, agent liquidity and overcharging can and should be addressed through effective monitoring by providers and their agent network managers. The future of DFS in India is in the hands the very people that provide these services.

Written by

Graham Wright

Group Managing Director

Leave comments